Approved by USDA’s World Agricultural Outlook Board

Livestock, Dairy, and Poultry Outlook

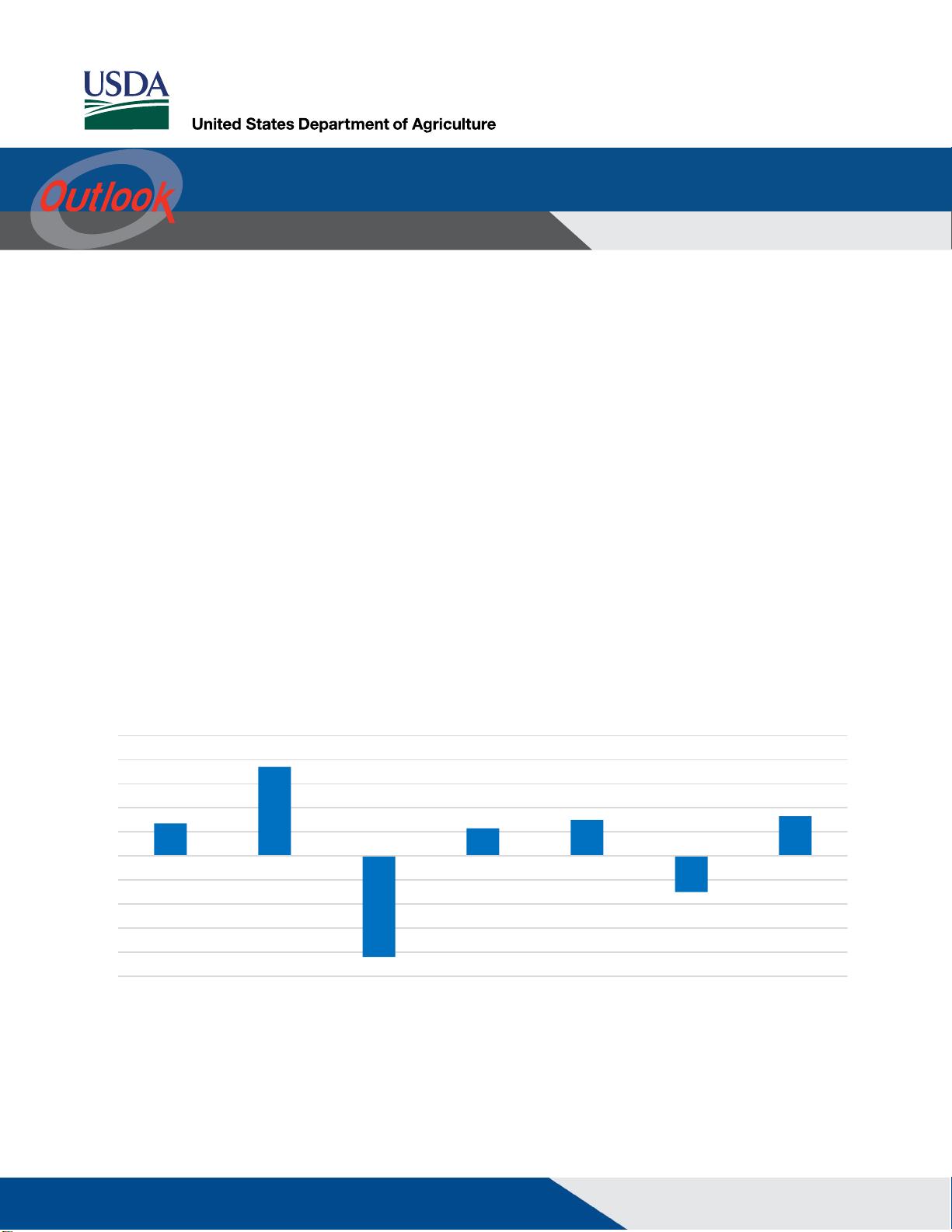

2020 Exports for Most Red Meats and Poultry Forecast Higher

U.S. exports of red meat and poultry are expected to increase by more than 4 percent in 2020. Beef

exports are forecast to increase 2.7 percent, largely due to lower anticipated competition in Asian

markets, as beef supplies in Oceania will reflect weather-related herd reduction this year. Pork exports

are expected to increase more than 7 percent next year as Mexican demand for U.S. pork is re-

established following the removal of tariffs in mid-May, 2019. Broiler export growth is forecast at 2.3

percent based on expectations of increased demand in low- and middle-income countries, particularly

as the global meat and poultry market is pressured by shifting Chinese demand. Growth of 3 percent is

anticipated for turkey exports next year, supported by strength in shipments to Mexico—the largest

buyer of U.S. turkey meat—with continued low turkey prices expected to draw additional international

buying interest. Lamb and mutton exports are likely to fall as U.S. production trends lower. Export

volumes for eggs and egg products are forecast to decrease by 3 percent, based on expectations of

continued softness in foreign demand. Dairy exports are expected to grow 3.3 percent next year as

global demand for dairy products grows.

2.7

7.4

-8.4

2.3

3.0

-3

3.3

-10

-8

-6

-4

-2

0

2

4

6

8

10

Beef

Pork

Lamb & Mutton

Broilers

Eggs

%

Percent change in exports (2020/2019)

Dairy*

Source: USDA, Economic Research Service.

*Dairy exports are reflected on a skim-solids milk-equivalent basis.

Turkey

Economic Research Service | Situation and Outlook Report

Next release is July 17, 2019

LDP-M-300 | June 17, 2019

剩余26页未读,继续阅读

资源评论

icwx_7550592

- 粉丝: 20

- 资源: 7163

最新资源

- 基于Delmia白车身侧围焊接的仿真分析与研究.pdf

- 基于Delmia白车身侧围焊接的研究.pdf

- 基于DSC的数字化逆变焊接电源的研制 - .pdf

- 基于FLUENT的CMT焊接熔池流场的数值分析 - .pdf

- 基于FPGA的焊接电源给定电流波形的研究 - .pdf

- 基于FPGA的焊接电源控制系统设计.pdf

- 基于GA算法的协调机器人双光束激光焊接轨迹规划研究.pdf

- 基于GMAW焊接快速制造的控形研究新进展 - .pdf

- 基于HMI和运动控制器的数控焊接系统设计.pdf

- 基于ISO15614-2标准的焊接工艺评定数据库系统 - .pdf

- 基于JB4708-2005的承压设备焊接工艺评定系统 - .pdf

- 基于MPC07运动控制卡的数控焊接机控制系统的开发.pdf

- 基于Labview平台的焊接电弧图像研究.pdf

- 基于MATLAB的仿人焊接机械手运动学分析和仿真 - .pdf

- 基于LabVIEW的搅拌摩擦焊焊接力监测系统设计.pdf

- 基于MFC和OpenGL的相贯线焊接仿真系统设计.pdf

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈