Approved by USDA’s World Agricultural Outlook Board

Approved by USDA’s World Agricultural Outlook Board

,

Rice Outlook

Nathan W. Childs, coordinator

U.S. Rice Export Forecasts Lowered for Both

2019/20 and 2020/21

There were several changes this month to both the 2019/20 and 2020/21 U.S. rice balance

sheets. For 2019/20, imports were raised, domestic use increased, and exports were lowered,

resulting in a 1.5-million-hundredweight (cwt) increase in the ending stocks forecast. For

2020/21, carryin, imports, and domestic use were revised up, while exports were lowered

slightly. On balance, these revisions resulted in a 2.5-million-cwt increase in the 2020/21 ending

stocks forecast. The 2020/21 U.S. season-average farm prices were unchanged from a month

earlier. In the global market, record production is projected for 2020/21 despite a reduction this

month in Vietnam’s crop forecast. The 2021 global rice trade forecast was lowered fractionally

but is still 6 percent above a year earlier. Global ending rice stocks were revised higher and

remain record high. Thailand’s trading prices have declined from early May, while U.S. prices

are unchanged and Vietnam’s prices are up slightly.

0

10

20

30

40

50

60

70

0

20

40

60

80

100

1985/85 1990/91 1995/96 2000/01 2005/06 2010/11 2015/16 2020/21f

Ending Stocks Stocks-to-Use

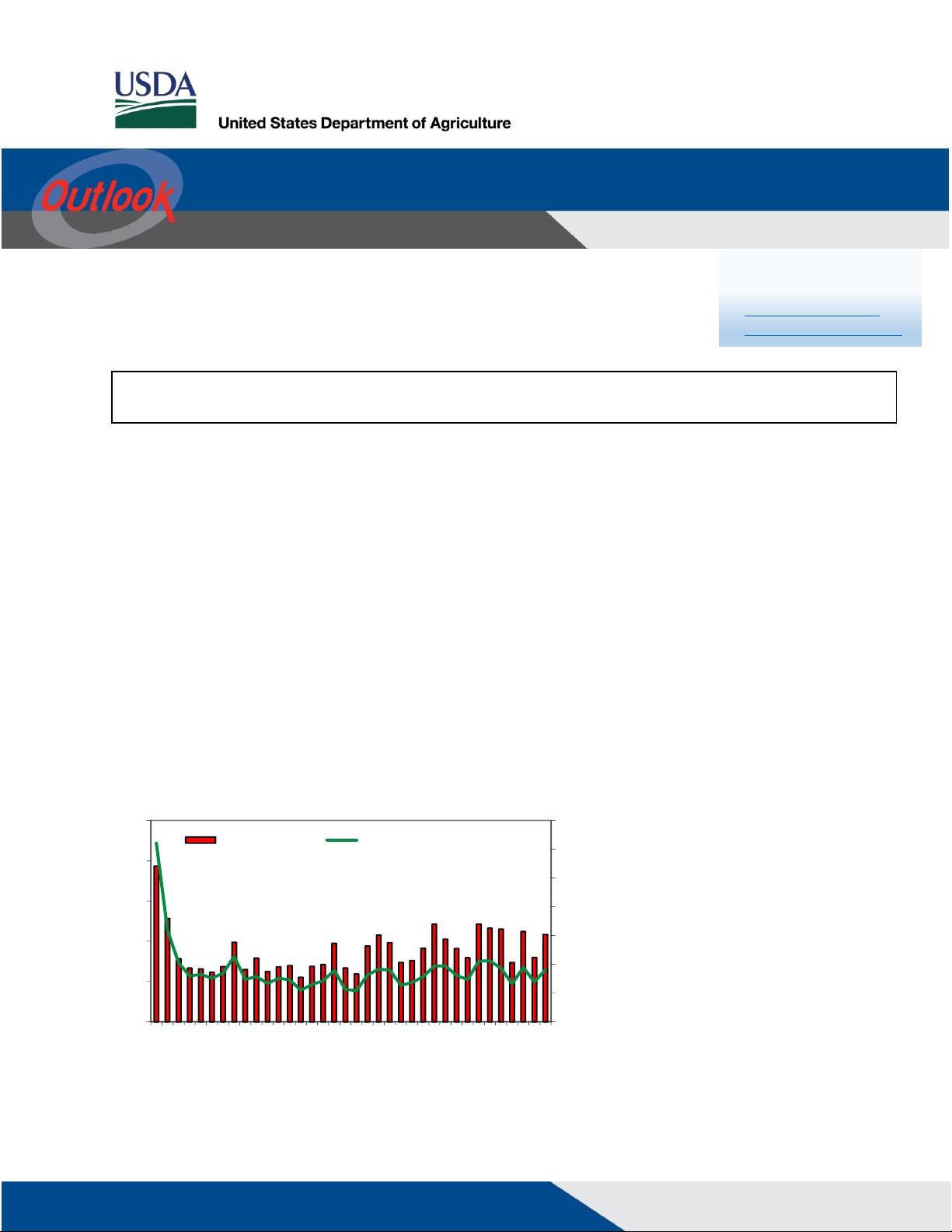

Figure 1

U.S. rice stocks projected to increase 35 percent in 2020/21

Million cwt (rough basis)

Percent

Cwt = Hundredweight. 2019/20 and 2020/21f = forecasts.

Sources: 1985/86-2017/18, Rice Yearbook Data Set, USDA, Economic Research

Service; 2018/19-2020/21, World Agricultural Supply and Demand Estimates, USDA,

World Agricultural Outlook Board.

August-July Market Year

Next release is July 14, 2020

RCS-20F June 15, 2020

In this report:

- Domestic Outlook

- International Outlook

Rice Outlook monthly tables, in excel format, can be found on the Rice Outlook report page on USDA’s

Economic Research Service website.

Economic Research Service | Situation and Outlook

Report

2

RCS-20F, June 15, 2020

USDA, Economic Research Service

Domestic Outlook

U.S. 2020/21 Total Rice Supply Forecast Raised 2.5 Million

Cwt

There were two supply-side revisions this month to the 2020/21 U.S. all-rice balance sheet.

First, the 2020/21 carryin was increased 1.5 million cwt to 32.0 million cwt, still down almost 29

percent from a year earlier. The increase was due to an upward revision—all for long-grain—in

the 2019/20 import forecast. By class, the long-grain 2020/21 carryin was raised 1.5 million cwt

to 16.2 million cwt, down 50 percent from a year earlier and second-smallest since 2004/05. In

contrast, the combined medium- and short-grain 2020/21 carryin remains forecast at 13.7

million cwt, up 35 percent from a year earlier.

The 2020/21 all-rice import forecast was raised 1.0 million cwt to a record 33.6 million cwt, up

just 0.1 million cwt from the 2019/20 revised import forecast. The 2020/21 import revision was

also all for long-grain and was based on stronger-than-expected purchases in 2019/20 through

April 2020 and expectations of continued large imports in 2020/21. Specific Asia aromatic

varieties not currently grown in the United States account for virtually all of the steady expansion

in U.S. long-grain imports. At 27.0 million cwt, U.S. 2020/21 long-grain imports are up 1.0 million

cwt from the previous forecast and unchanged from the year-earlier revised record.

U.S. medium- and short-grain imports in 2020/21 remain forecast at a record 6.6 million cwt, an

increase of just 0.1 million cwt from 2019/20. U.S. medium- and short-grain imports have

increased sharply since 2017/18 due to continued large purchases of China’s rice by Puerto

Rico. This rice is sold at substantially discounted prices from multi-year Government-held

stocks. Since May 2018, China has sent three or four shipments of about 21,000 tons of milled

medium- and short-grain rice to the United States every 12 months. These shipments are

expected to continue in 2020/21. China and Thailand each now account for about a third of total

U.S. medium- and short-grain rice imports. India supplies around 15 percent, with Italy a regular

supplier of smaller quantities of its Arborio rice.

The 2020/21 U.S. rice crop remains projected at 216.2 million cwt, up 31.5 million cwt from a

year earlier, a result of both larger area and a higher yield. The harvested area estimate of 2.81

million acres is based on the NASS March 31 Prospective Planting report and uses a 5-year

Olympic average of planted-to-harvested ratio by class. The first survey of actual plantings of

the 2020/21 U.S. rice crop will be reported by the National Agricultural Statistics Service (NASS)

in the June Acreage report, scheduled for release on June 30. The 2020/21 average rice yield

remains projected at 7,699 pounds per acre, up 228 pounds from a year earlier and the highest

on record. The yield is based on trend yield by class. The first survey yield forecast for the

2020/21 U.S. rice crop will be released on August 12 in the NASS Crop Production report.

By class, long-grain rice production in 2020/21 remains projected at 155.5 million cwt, up 24

percent from a year earlier. Almost all U.S. long-grain rice is grown in the South. The 2020/21

combined medium- and short-grain crop remains projected at 60.7 million cwt, up almost 3

percent from a year earlier and the largest since 2011/12. About 80 percent of the U.S.

medium- and short-grain crop is grown in California.

Progress of the 2020/21 U.S. rice crop remains slightly behind normal in parts of the Delta, a

result of persistent rain and wet conditions this Spring, similar to 2019/20 but not as severe. For

the week ending June 7, 95 percent of the U.S. rice crop was reported planted, unchanged from

mRtPpNxPwO8O9RbRoMrRnPrReRrRpRiNmNoRbRoPsMuOsRoRuOpOrP

3

RCS-20F, June 15, 2020

USDA, Economic Research Service

last year’s rain-delayed crop but 3 percentage points behind the U.S. 5-year average. Progress

varied by region and State. On the Gulf Coast, planting was completed in Louisiana by June 7,

just 1 percentage point ahead of a year earlier and even with the State’s 5-year average.

Harvest should begin in Louisiana in early July. Planting was only slightly slower in Texas, with

98 percent of the crop reported planted by June 7, 1 percentage point ahead of both a year

earlier and the Texas 5-year average. For both Gulf Coast States, early planting bodes well for

a good yield and a successful ratoon crop.

In the Delta, the Arkansas crop was reported 93-percent planted by June 7, unchanged from a

year earlier but behind the Arkansas 5-year average of 98 percent, a result of the persistent rain

this Spring. Missouri’s crop was reported 86-percent planted by June 7, 2 percentage points

ahead of a year earlier but behind the Missouri 5-year average of 95 percent, also a result of the

continued rain and wet conditions. Mississippi’s crop was reported 98-percent planted by June

7, up 3 percentage points from a year earlier but unchanged from the State’s 5-year average.

Finally, in California, 100 percent of the rice crop was reported planted by June 6, 1 percentage

point ahead of both a year earlier and the California 5-year average.

Emergence of the 2020/21 U.S. rice crop remains behind normal in much of the Delta as well,

with the pace of emergence varying by State and region. For the week ending June 7, 88

percent of the U.S. 2020/21 rice crop had emerged, 4 percentage points ahead of a year earlier

but behind the U.S. average of 93 percent. On the Gulf Coast, 98 percent of the Texas crop had

emerged by June 7, ahead of both 91 percent a year earlier and the Texas 5-year average of 94

percent. In Louisiana, 97 percent of the crop had emerged by June 7, 1 percentage point ahead

of a year earlier and 2 percentage points ahead of the Louisiana 5-year average.

In the Delta, 87 percent of the Arkansas crop had emerged by June 7, 5 percentage points

ahead of the year-earlier rain-delayed crop but behind the Arkansas 5-year average of 95

percent. In nearby Missouri, 78 percent of the rice crop had emerged by June 7, just 1

percentage point ahead of last year’s rain-delayed crop but well behind the Missouri 5-year

average of 91 percent. Mississippi’s crop was reported 89 percent emerged by June 7, 4

percentage points ahead of a year earlier but behind the Mississippi 5-year average of 93

percent. In California, 85 percent of the crop had emerged by June 7, 4 percentage points

ahead of last year and 5 percentage points ahead of the California 5-year average.

Crop conditions for 2020/21 are much improved from a year earlier in most States, mostly due

to more favorable weather in most areas, despite the persistent rainfall in parts of the Delta. For

the week ending June 7, 70 percent of the U.S. 2020/21 rice crop was rated in good or excellent

condition, compared with 61 percent a year earlier. In Arkansas, 64 percent of the 2020/21 crop

was rated in good or excellent condition for the week ending June 7, up from 56 percent a year

earlier. In nearby Missouri, 54 percent of the 2020/21 rice crop was rated in good or excellent

condition, up from 48 percent a year earlier. In contrast, 56 percent of Mississippi’s 2020/21 rice

crop was rated good or excellent, down from 63 percent a year earlier. In Louisiana, 83 percent

of the 2020/21 rice crop was rated in good or excellent condition, up from 68 percent a year

earlier. Similarly, in Texas, 62 percent of the 2020/21 rice crop was rated in good or excellent

condition for the week ending June 7, well above just 35 percent a year earlier. Finally, in

California 85 percent of the 2020/21 rice was rated in good or excellent condition, unchanged

from a year earlier.

This month’s upward revision in both carryin and imports boosted the 2020/21 U.S. total rice

supply forecast 2.5 million cwt to 281.8 million cwt, 7 percent larger than in 2019/20. The

expectation of larger supplies in 2020/21 is the result of a 17-percent increase in production

more than offsetting a substantial decline in carryin, with imports just fractionally higher. At

4

RCS-20F, June 15, 2020

USDA, Economic Research Service

198.7 million cwt, the 2020/21 long-grain total supply forecast is up 2.5 million cwt from the

previous forecast and more than 7 percent larger than in 2019/20. A much larger crop and

slightly increased imports more than offset a substantial decline in carryin. Combined medium-

and short-grain total supplies remain forecast at 81.1 million cwt, also up 7 percent from

2019/20, mostly due to a larger carryin, with expected increases in production and imports much

smaller.

2020/21 U.S. Export Forecast Lowered; Domestic Use Raised

Total use of U.S. rice in 2020/21 is projected at 238.5 million cwt, up 1.0 million cwt from the

previous forecast and 3 percent larger than the year-earlier revised level, with forecasts for both

exports and domestic and residual use projected to be higher in 2020/21. Long-grain total use is

projected at 176.0 million cwt, an increase of 1.0 million cwt from the previous forecast and 4

percent larger than the year-earlier revised forecast. Medium- and short-grain total use in

2020/21 remains forecast at 62.5 million cwt, up less than 1 percent from a year earlier.

Total domestic and residual use in 2020/21 is projected at 139.5 million cwt, up 2.0 million cwt

from the previous forecast, more than 3 percent larger than a year earlier and the second

highest on record. This month’s upward revision in the total domestic and residual use forecast

was primarily based on the higher import forecast. The year-to-year increase in total domestic

and residual use is primarily based on increased supplies of rice in 2020/21 and expectations of

greater post-harvest losses associated with a larger crop. By class, long-grain domestic and

residual use is projected at 105.0 million cwt, up 2.0 million cwt from the previous forecast and 4

percent larger than a year earlier. Combined medium- and short-grain domestic and residual

use remains projected at 34.5 million cwt, up almost 1.5 percent from 2019/20.

Total U.S. rice exports in 2020/21 are projected at 99.0 million cwt, down 1.0 million cwt from

the previous forecast but still 3 percent larger than the year-earlier revised estimate. Long-grain

accounts for all of the expected increase in U.S. exports in 2020/21. At 71.0 million cwt, the U.S.

2020/21 long-grain export forecast is down 1.0 million cwt from the previous forecast but still up

more than 4 percent from the year-earlier revised level. This month’s slight reduction in the

2020/21 long-grain export forecast is based on expectations of continued strong competition

from South American exporters in Latin American markets. Latin America is the largest market

for U.S. long-grain rice. On an annual basis, the expected increase in long-grain exports is

based on larger U.S. supplies and lower projected U.S. long-grain prices. Similar to recent

years, the United States is expected to ship little rice to Sub-Saharan Africa beyond food aid

shipments—which account for less than 3 percent of total U.S. rice exports—and is likely to

continue to sell almost no long-grain rice to Asia. U.S. prices are too high for these two price-

sensitive markets.

U.S. medium- and short-grain rice exports in 2020/21 remain projected at 28.0 million cwt,

unchanged from 2019/20. The United States is expected to again export little rice beyond its

current six core markets. First, the three major buyers in Northeast—Japan, South Korea, and

Taiwan, whose purchases are all made as part of World Trade Organization agreements—are

expected to again account for around two-thirds of U.S. medium- and short-grain exports (on a

rough basis). Jordan typically imports around 3 million cwt, all milled rice. Mexico typically

purchases a small amount of U.S. medium-grain rough rice. Canada is also regular buyer of

relatively small quantities U.S. medium-grain milled rice. Turkey, once a large regular buyer of

U.S. medium- and short-grain rice, returned as small buyer of U.S. rice in 2019/20, purchasing

less than a million cwt of California rough rice. Little, if any, growth in U.S. exports of medium-

and short-grain exports to Turkey is expected in 2020/21.