www.jpmorganmarkets.com

North America Equity Research

04 January 2019

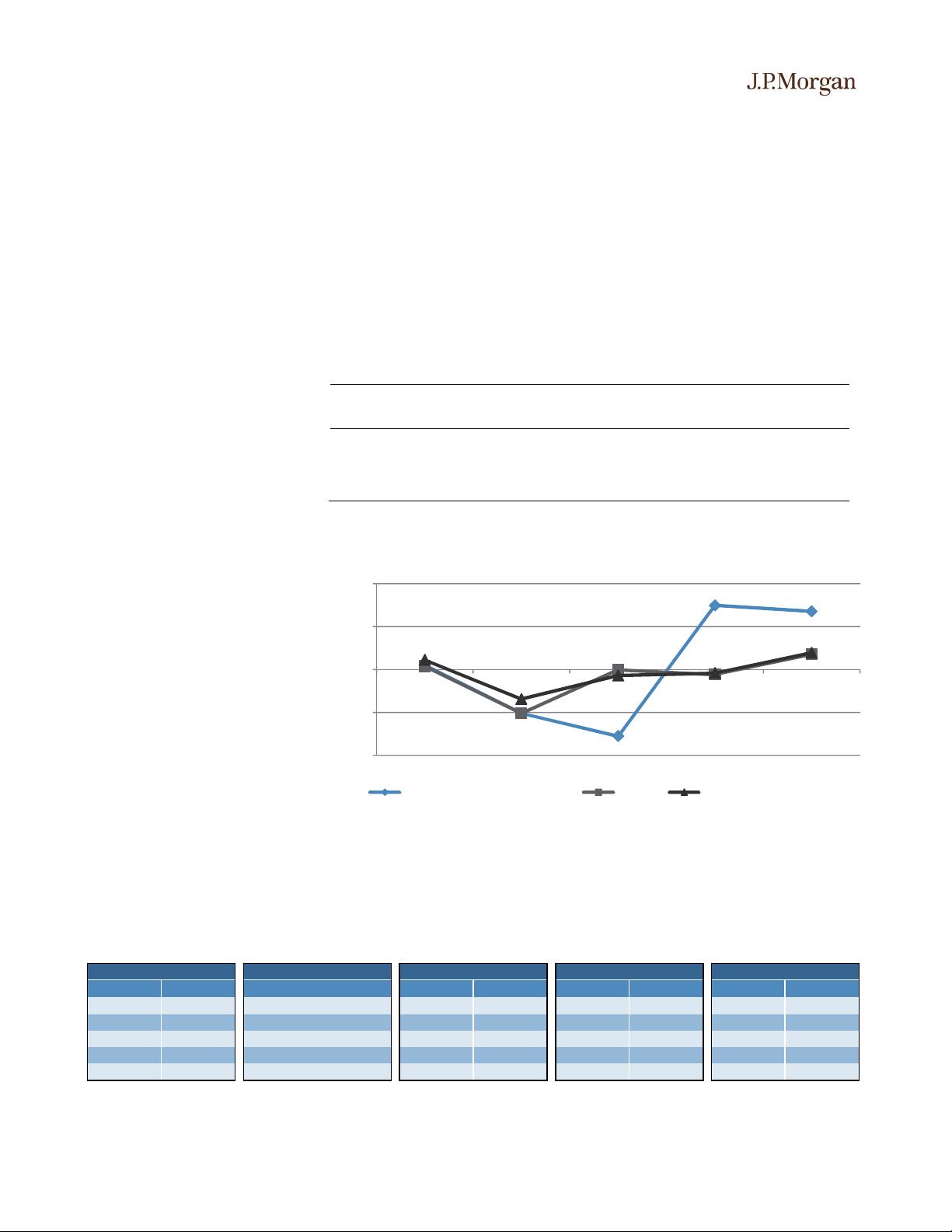

Equity Ratings and Price Targets

Mkt Cap

Rating

Price Target

Company

Ticker

($ mn)

Price ($)

Cur

Prev

Cur

End

Date

Prev

End

Date

AmerisourceBergen

ABC US

15,957.39

73.37

N

n/c

89.00

Dec

-

19

n/c

n/c

Cardinal Health

CAH US

13,512.96

44.16

N

n/c

59.00

Dec

-

19

n/c

n/c

McKesson Corporation

MCK US

22,429.88

112.94

OW

n/c

160.00

Dec

-

19

n/c

n/c

Owens & Minor, Inc.

OMI

US

387.31

6.47

UW

n/c

10.00

Dec

-

19

n/c

n/c

CVS Health

CVS US

66,665.06

65.23

OW

n/c

106.00

Dec

-

19

n/c

n/c

Walgreens Boots Alliance Inc

WBA US

64,057.76

67.33

OW

n/c

91.00

Dec

-

19

n/c

n/c

Rite Aid

RAD US

792.05

0.75

N

n/c

— —

n/c

n/c

Diplomat

Pharmacy, Inc.

DPLO US

998.55

13.36

OW

n/c

21.00

Dec

-

19

n/c

n/c

LabCorp

LH US

12,827.69

123.70

OW

n/c

185.00

Dec

-

19

n/c

n/c

Quest Diagnostics

DGX US

11,295.20

80.68

N

n/c

100.00

Dec

-

19

n/c

n/c

Henry Schein Inc

HSIC US

11,332.10

73.77

N

n/c

85.00

Dec

-

19

n/c

n/c

Patterson Companies

PDCO US

1,857.38

19.91

UW

n/c

22.00

Dec

-

19

n/c

n/c

Cerner

CERN US

17,176.15

50.70

N

n/c

60.00

Dec

-

19

n/c

n/c

Premier, Inc.

PINC US

5,154.93

36.65

N

n/c

45.00

Dec

-

19

n/c

n/c

Teladoc Health Inc

TDOC US

3,155.09

46.23

OW

n/c

80.00

Dec

-

19

n/c

n/c

Allscripts

MDRX US

1,760.80

9.58

N

n/c

12.00

Dec

-

19

n/c

n/c

Evolent Health

EVH US

1,315.39

19.30

N

n/c

25.00

Dec

-

19

n/c

n/c

HealthEquity

HQY US

3,390.90

54.90

OW

n/c

102.00

Dec

-

19

n/c

n/c

NextGen Healthcare,

Inc.

NXGN US

944.57

15.15

UW

n/c

17.00

Dec

-

19

n/c

n/c

Source: Company data, Bloomberg, J.P. Morgan estimates. n/c = no change. All prices as of 03 Jan 19.

Healthcare Technology &

Distribution

Gill's Guide to the 2019 J.P. Morgan Healthcare

Conference

Healthcare Technology &

Distribution

Lisa C. Gill

AC

(1-212) 622-6466

lisa.c.gill@jpmorgan.com

Bloomberg JPMA GILL <GO>

Anne E. Samuel

AC

(1-212) 622-4163

anne.e.samuel@jpmorgan.com

Michael Minchak, CFA

AC

(1-212) 622-6506

michael.minchak@jpmorgan.com

J.P. Morgan Securities LLC

See

page 60 for analyst certification and important disclosures.

J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aw

are that

the firm may have a conflict of interest that could affect th

e objectivity of this report. Investors should consider this report as only a single

factor in making their investment decision.

Happy New Year! Ahead of the 2019 J.P. Morgan Healthcare Conference next week, we

thought it might be helpful to highlight key themes across the various sub-sectors as well as

key company-specific topics we expect to be discussed at the conference. This report is

broken down by sector: Pharmaceutical and Medical/Surgical Distribution, Retail

Pharmacy, PBM/Specialty Pharmacy, Clinical Labs, Dental Distribution and HCIT. We

also include a financial snapshot for each company.

All of our covered companies are attending the conference. And we once again have

100% CEO participation among the presenting companies.

2017 and 2018 were both somewhat quieter years after a very busy 2016 conference

with respect to news flow in our space, and at this point, we are not anticipating

major announcements from companies in our space. Within our coverage universe,

all of the Rx channel names have provided FY19 guidance with the exception of CVS

(which plans to provide initial 2019 guidance with 4Q earnings on February 20), and

DPLO (which has made announcements regarding guidance around the conference in

each of the past two years and has previously indicated plans to provide guidance in

early in 2019). For the clinical labs, we expect LH and DGX to wait to issue formal 2019

guidance on their Q4 earnings calls, noting 2018 guidance for both companies was

recently reduced. While TDOC has previously discussed providing initial 2019 guidance

with 4Q18 earnings, as in previous years, we believe the company could provide

preliminary 2018 results and preliminary 2019 metrics at the conference.

We expect consumerism to be a key theme at the conference, as we believe the

consumer will be the biggest disruptor in healthcare. With healthcare rising as a

percentage of household expenditures, patients are becoming more involved in making

decisions on how to allocate their healthcare dollars, and are becoming increasingly

selective in the services they use with cost, quality, and convenience being key deciding

factors. Engaging the patient at their preferred point of service in a low cost way will

likely differentiate those with a strong reputation and a trusted brand.

剩余62页未读,继续阅读

资源评论

xox_761617

- 粉丝: 29

- 资源: 7802

最新资源

- 形状检测32-YOLO(v5至v9)、COCO、CreateML、Darknet、Paligemma数据集合集.rar

- qwewq23132131231

- 2024年智算云市场发展与生态分析报告

- 冒泡排序算法解析及优化.md

- MySQL中的数据库管理语句-ALTER USER.pdf

- 论文复现:结合 CNN 和 LSTM 的滚动轴承剩余使用寿命预测方法

- 2018年最新 ECshop母婴用品商城新版系统(微商城+微分销+微信支付)

- 形状分类31-YOLO(v5至v11)、COCO、CreateML、Darknet、Paligemma、VOC数据集合集.rar

- 常见排序算法概述及其性能比较

- 前端开发中的JS快速排序算法原理及实现方法

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈