2024年美赛35篇特等奖O奖论文-E-2400860.pdf

版权申诉

53 浏览量

2024-05-06

11:41:26

上传

评论

收藏 1.52MB PDF 举报

Veils of Uncertainty: Weaving Risk into the Tapestry of Preservation

Under the Weather's Watch

Summary

As the tapestry of nature weaves its unpredictable patterns, humanity’s quest for stability

becomes ever more pressing. In the shadow of uncertainty, we find resilience, crafting shields

against the tempests of fate.

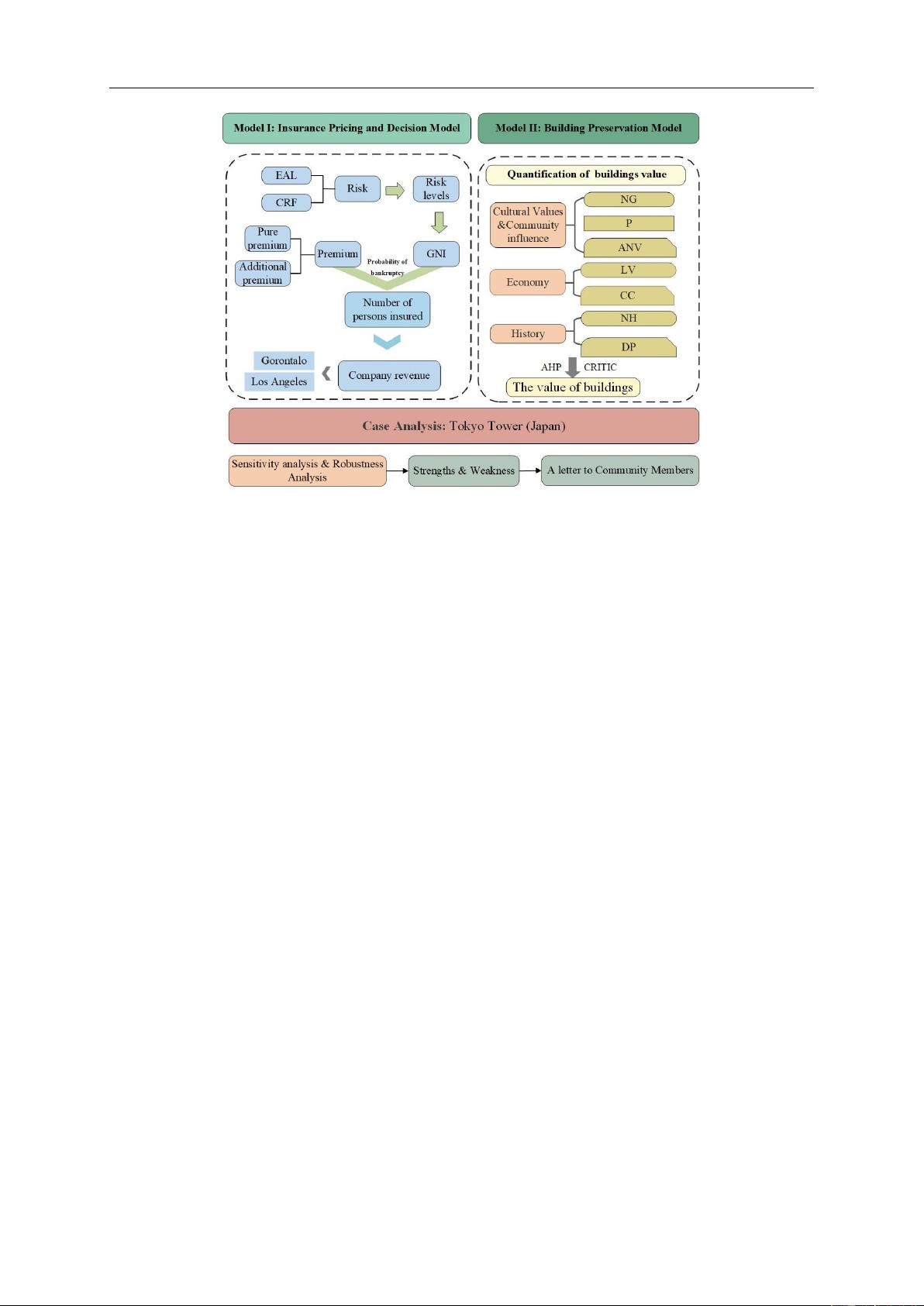

First, we establish a Risk Analysis model to comprehensively assess the Expected An-

nual Loss (EAL) from extreme weather in terms of population, building, and agriculture. The

assessment for each aspect is calculated from three perspectives: natural hazard exposure, His-

toric Loss Ratio, and the likelihood risk factor of natural hazard annualized frequency. Com-

munity Risk Factor (CRF) is calculated from social vulnerability and community resilience.

EAL and CRF are used to quantify the risk levels of various regions and rank them using the

K-means algorithm, resulting in a risk level map of the United States.

Second, we develop a Risk-incorporated Capital Asset Pricing Model (CAPM) to aid

insurance companies in underwriting decisions. This model combines market return rates, the

risk-free rate, and bankruptcy theory with a 10% bankruptcy probability to set insurance rates.

It evaluates if the region's residents can afford these premiums, providing decision-making ad-

vice for insurance companies.

More specifically, we apply our Risk-incorporated Capital Asset Pricing Model in Los

Angeles and Gorontalo. In Los Angeles, insurance companies see high profits and low risks.

However, in Gorontalo, the required premium for $10,000 coverage is $342.745, beyond local

affordability. We recommend insurance securitization and partnerships with local govern-

ments to reduce premiums. Consequently, Gorontalo residents could pay just $137.25 annually,

with companies projecting $245 million in revenue.

Third, we establish a Building Preservation Model, selecting seven secondary indicators

such as the annual number of visitors and construction cost, and three primary indicators: cul-

tural values and community influence, economy, and history. These are weighted using the

Sperman-CRITIC algorithm and AHP method to calculate building value, combined with

risk levels to determine the preservation level of buildings. Based on the preservation level, the

community's investment and measures for building protection can be determined.

Then our models inform investment and protection strategies for Tokyo Tower, acknowl-

edging its value and the necessity of preservation in an earthquake zone. We communicate these

findings and propose protection measures to the Tokyo Tower community.

Finally, we analyze the sensitivity and robustness of our models, the models can change

the insurance rate sensitively according to the change of the market predicted return and the

slight error of the risk factor calculation will not affect the models’ result, which verifies the

sensitivity and robustness of our models. In addition we analyze the strengths and weaknesses

of the models.

Keywords: Risk Analysis, Risk-Capital Asset Pricing Model, Sperman-CRITIC, AHP,

Building Preservation Model.

Problem Chosen

E

2024

MCM/ICM

Summary Sheet

Team Control Number

2400860

剩余26页未读,继续阅读

资源评论