2024年美赛35篇特等奖O奖论文-E-2401102.pdf

版权申诉

96 浏览量

2024-05-06

11:41:29

上传

评论

收藏 10.39MB PDF 举报

Problem Chosen

E

2024

MCM/ICM

Summary Sheet

Team Control Number

2401102

In Face of Increasingly Severe Extreme Weather:

Sustainable Property Insurance under Risk

Summary

The rst priority of survival is getting protection from the extreme weather. —Bear Grylls

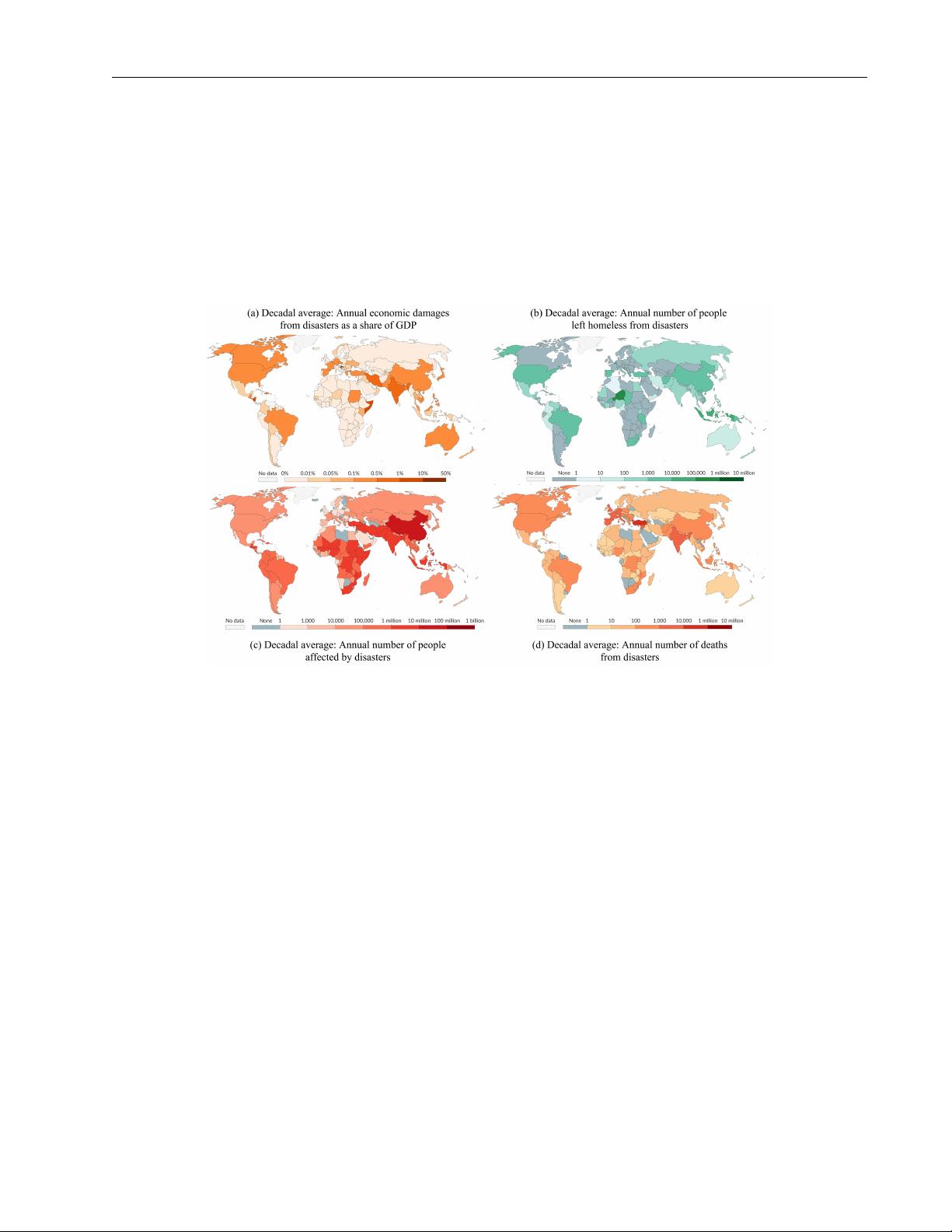

More frequent and severe extreme weather events are causing greater damage to people’s prop-

erty, leading to a reevaluation of the sustainability of insurance companies. On one hand, maintaining

enough customers for long-term healthy operation is crucial; on the other hand, avoiding excessively

high compensation risks to remain protable is essential. Therefore, we assessed the sustainability of

the insurance sector in areas that were frequently impacted by extreme weather events from two per-

spectives: insurance demand and total risk.

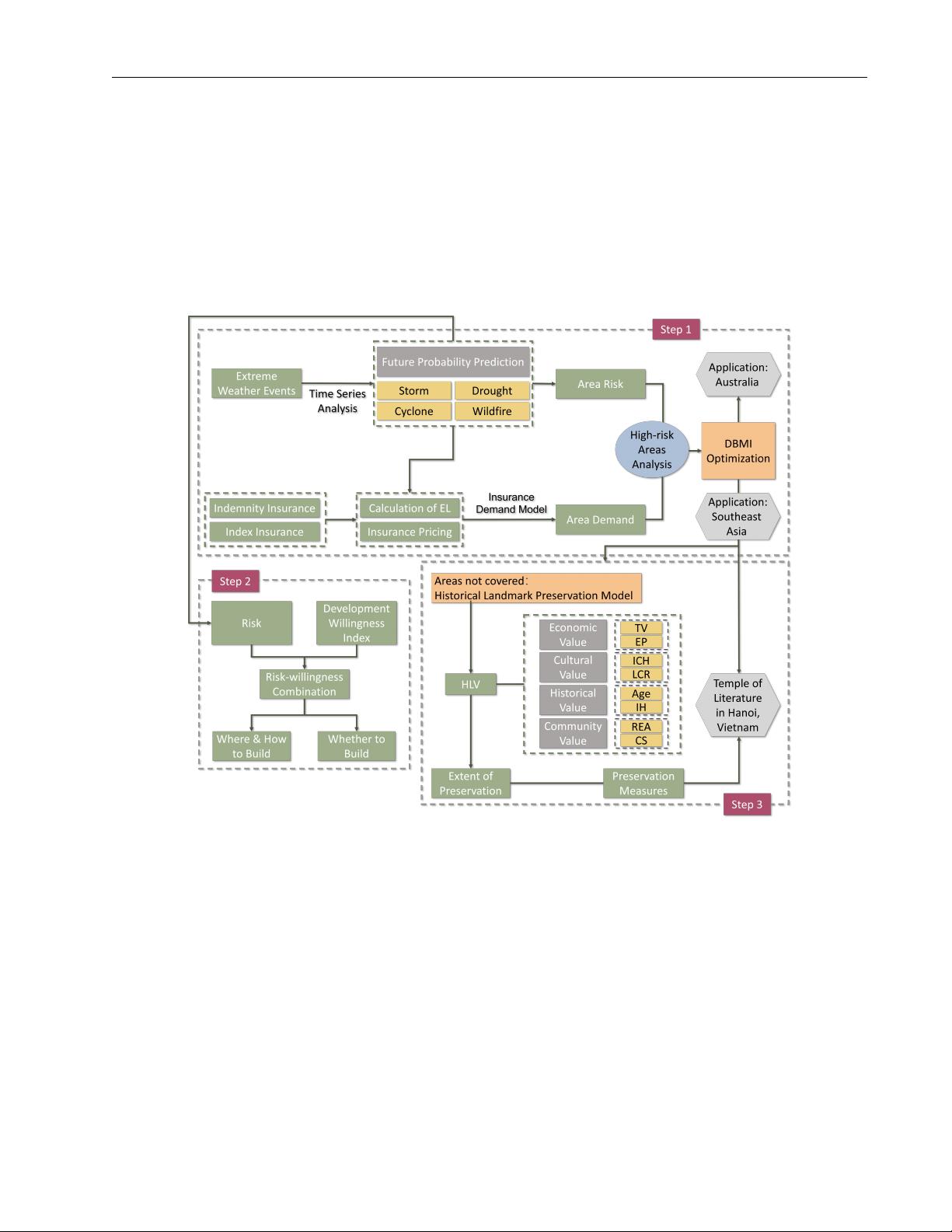

For Task 1, we developed a Property Insurance Posture Model for insurance companies. We

categorized extreme weather into 4 types and used an ARIMA model to forecast the future risk of

extreme weather for each region-disaster pair, and calculated the expected loss. Then, we used Lane’s

AFC model to calculate premiums. To measure demand with premiums, we introduced the insurance

demand curve. Finally, we established Demand-Risk Equilibrium Model for Insurance(DBMI) to

provide decisions on whether to underwrite insurance in specic regions.

Next, we applied the model above to Australia and Southeast Asia, where approximately 60 years of

data from 3000 records were available. Then we applied ARIMA model on selected area-event series,

with an eminent t: R

2

consistently above 0.625, and IC all below 300. Consequently, we forecast

the risks for 2024-2027. This has resulted in the determination of premiums ranging from $119.2 to

$1295.6. The optimal solutions indicated that in Australia, QLD and WA should be underwritten; in

SE Asia, PHL and THA.

For Task 2, we introduced Innovative Risk Prediction Property Development Method(IRPPDM),

which integrated DBMI with real estate companies’ willingness index to construct a Willingness-Risk

coordinate system. We specically targeted High Risk-High Willingness areas, providing 3 possible

risk reassessment methods to help transfer them into Low Risk-High Willingness category.

For Task 3, we used Historic Landmark Preservation Model to help community leaders. We

estimated the signicance of historic landmarks by AHP method considering 8 indicators in 4 dimen-

sions. Then we oered suggestions considering both the extent of signicance and predicted risks.

According to our model, Temple of Literature in Hanoi, Vietnam had a score of 0.463, facing risks

of oods and cyclones. Considering its features, we oered 4 tailored suggestions.

In the end, we stated the strengths and weaknesses of models. Based on their performances in

application, Property Insurance Posture Model reasonably balanced demand and risk, and Historic

Landmark Preservation Model was comprehensive in measuring value.

Keywords: Extreme Weather Event; Property Insurance; ARIMA; Dual-objective Optimization; AHP

剩余24页未读,继续阅读

资源评论