汇丰银行-全球-股票策略-全球股票策略:盈利——已过了最差的情况-217-22页.pdf

需积分: 0 192 浏览量

2023-07-26

11:53:58

上传

评论

收藏 899KB PDF 举报

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities (USA) Inc

View HSBC Global Research at:

https://www.research.hsbc.com

Earnings downgrade cycle is arguably through the worst and

we see upside, especially to US consensus estimates

Our proprietary analysis of US and European earnings calls

highlights margin resilience, China pessimism, political risks

Present four stock screens: conservative guidance, DM stocks

with China exposure, and ESG interest in Europe and US

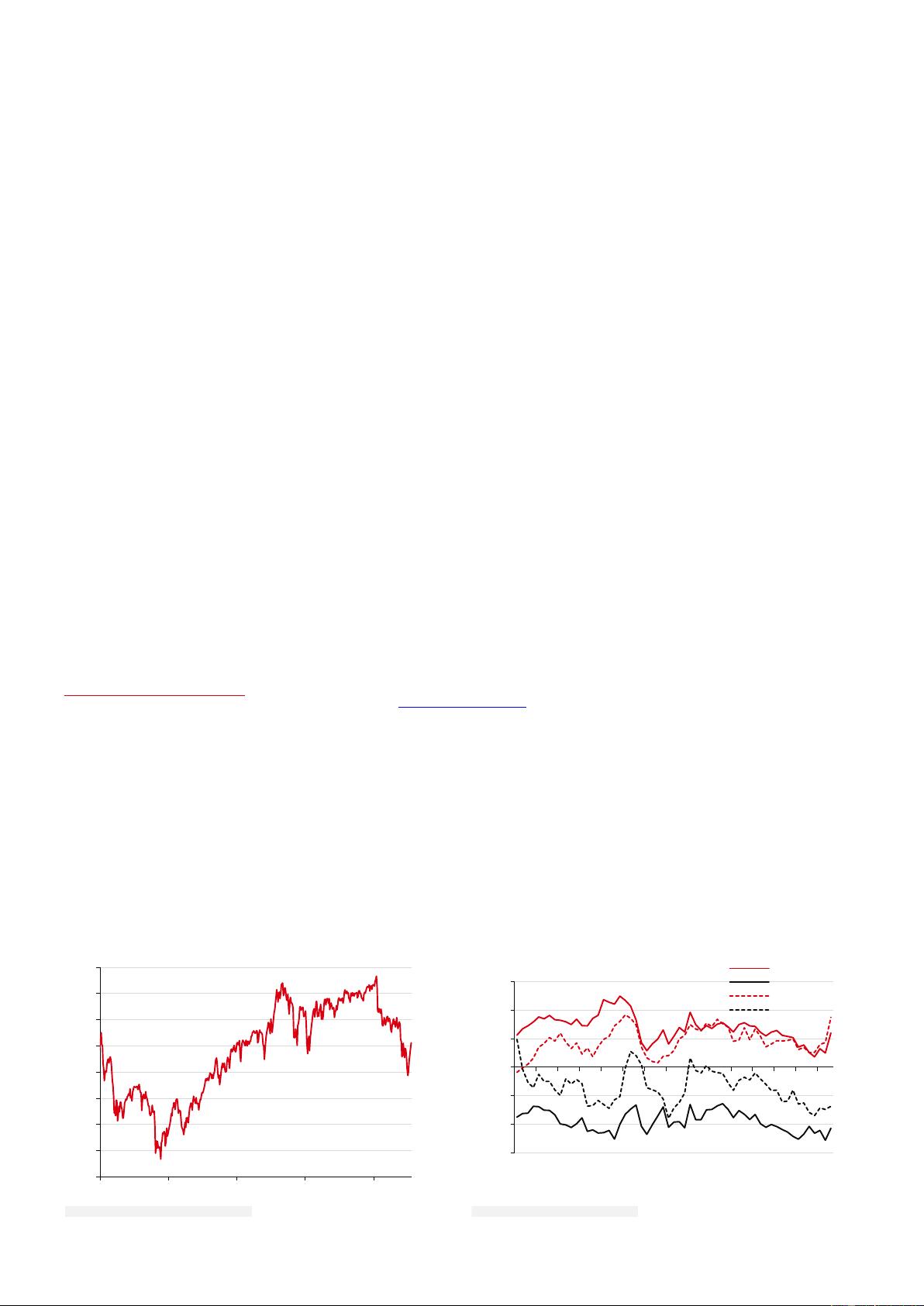

Global equity markets have been on a tear in 2019, up 8.5% YTD, largely fuelled by

a re-rating of overly depressed valuations. We believe the rally has further to go, but

it will likely need a firmer earnings outlook. In our view, the recent poor earnings

revisions cycle is through the worst. Economic activity is easing but above-trend, and

we see upside to a US-China trade deal and China policy stimulus.

In this report we apply our natural language processing methodology to nearly

60,000 earnings calls covering US and European companies. This analysis extends

our work in Alternative Data (see Text analysis of earnings calls 13-Sep-18, and

China sentiment, 17-Jan-19). The results identify four key themes from the earnings

season in the US and Europe so far:

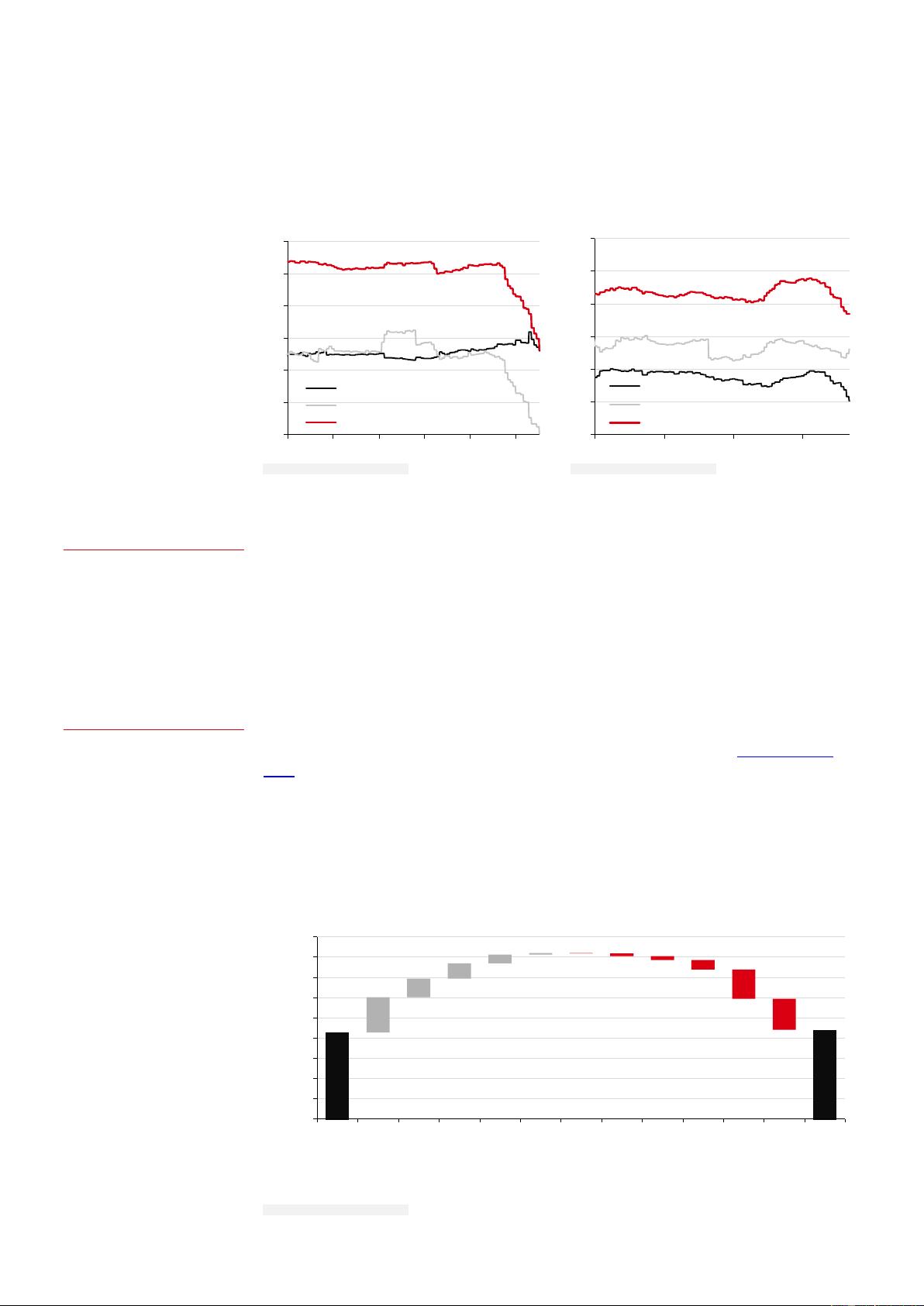

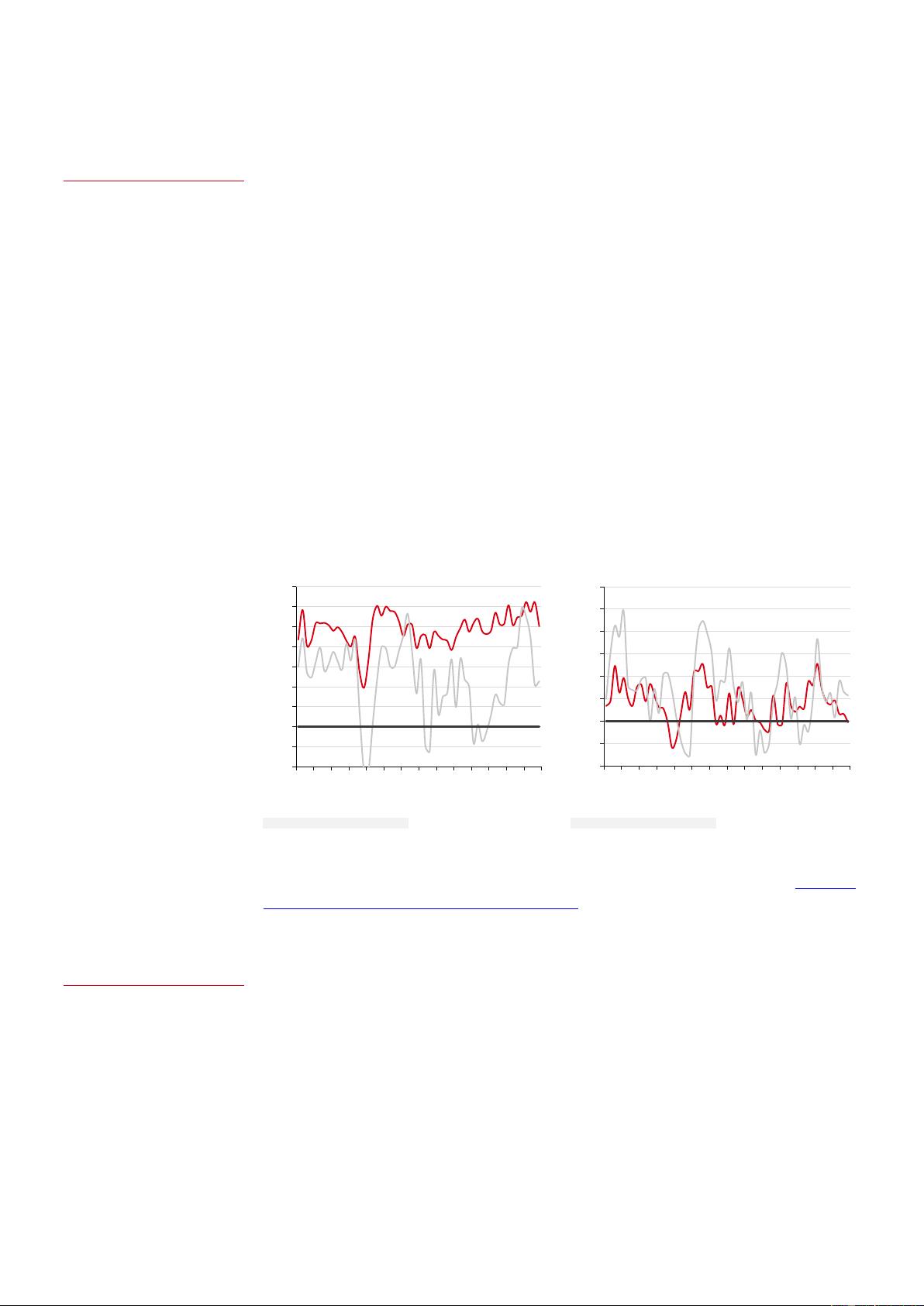

#1: Margins resilient: Corporate concerns about profit margins remain below

average and fears over wage growth have receded. The strong USD is a headwind

for US firms but a tailwind for those based in Europe. Longer term, US record-high

profit margins seem structurally supported by tech and tax reform.

#2: Don’t overdo politics: Focus has been on US-China relations, Brexit and US

government shutdown. Many corporates indicated they can offset tariff headwinds,

and had already incorporated worst-case scenarios into guidance (see Appendix 1).

We estimate that the US Government shutdown cost 1.7pp of Q1 EPS growth.

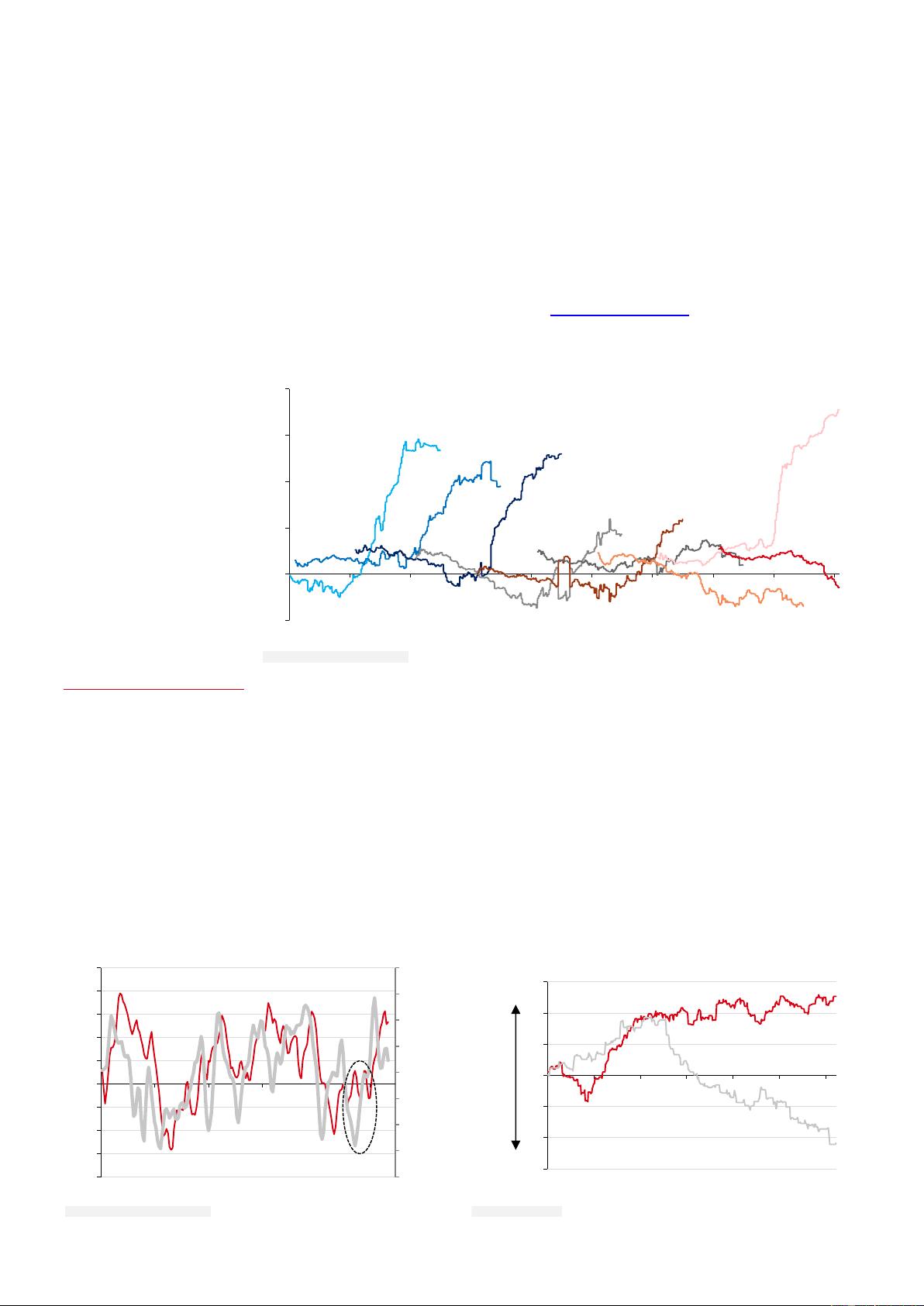

#3: Contrarian China sentiment: Analyst sentiment towards China on earnings calls

has plunged. Historically this has been a contrarian positive, with a 20% one-year

return from such levels. US and European corporate managements are more

confident on China. See Appendix 2 for HSBC Buy-rated China-exposed stocks.

#4: ESG on the agenda: Discussion of ESG matters has increased, focused on issues

such as culture and impacts on society. See Appendixes 3 and 4 for full details.

We are overweight US equities, and forecast nearly 10% EPS growth this year,

above consensus, on continued revenue growth and margin resilience. We are

underweight Europe ex UK, where we see less scope for a positive surprise.

Natural language processing is extremely flexible and can be applied to many other

topics. If you are interested in analyzing specific themes please contact Mark McDonald

and Alastair Pinder.

17 February 2019

Ben Laidler

Global Equity Strategist

HSBC Securities (USA) Inc.

ben.m.laidler@us.hsbc.com

+1 212 525 3460

Daniel Grosvenor*

Equity Strategist

HSBC Bank plc

daniel.grosvenor@hsbcib.com

+44 20 7991 4246

Alastair Pinder, CFA

Equity Strategist

HSBC Securities (USA) Inc.

alastair.pinder@us.hsbc.com

+1 212 525 4131

Mark McDonald

Head of Data Science and Analytics

HSBC Bank plc

mark.mcdonald@hsbcib.com

+44 20 7991 5966

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is

not registered/ qualified pursuant to FINRA regulations

Global Equity Strategy

EQUITY STRATEGY

GLOBAL

Listen up: Earnings – through the worst

剩余20页未读,继续阅读

资源评论