汇丰银行-全球-石油与天然气行业-石油市场展望:价格削减——看起来具有挑战性-9-24页.pdf

需积分: 0 195 浏览量

2023-07-27

14:24:09

上传

评论

收藏 677KB PDF 举报

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Bank plc

View HSBC Global Research at:

https://www.research.hsbc.com

Demand concerns dominate at present, although the market

should tighten in the next few months

2020 could be tough, with little room for higher OPEC output

2020 Brent price forecast cut by USD10/b to USD60/b; longer

term forecasts cut by USD5/b to USD65/b

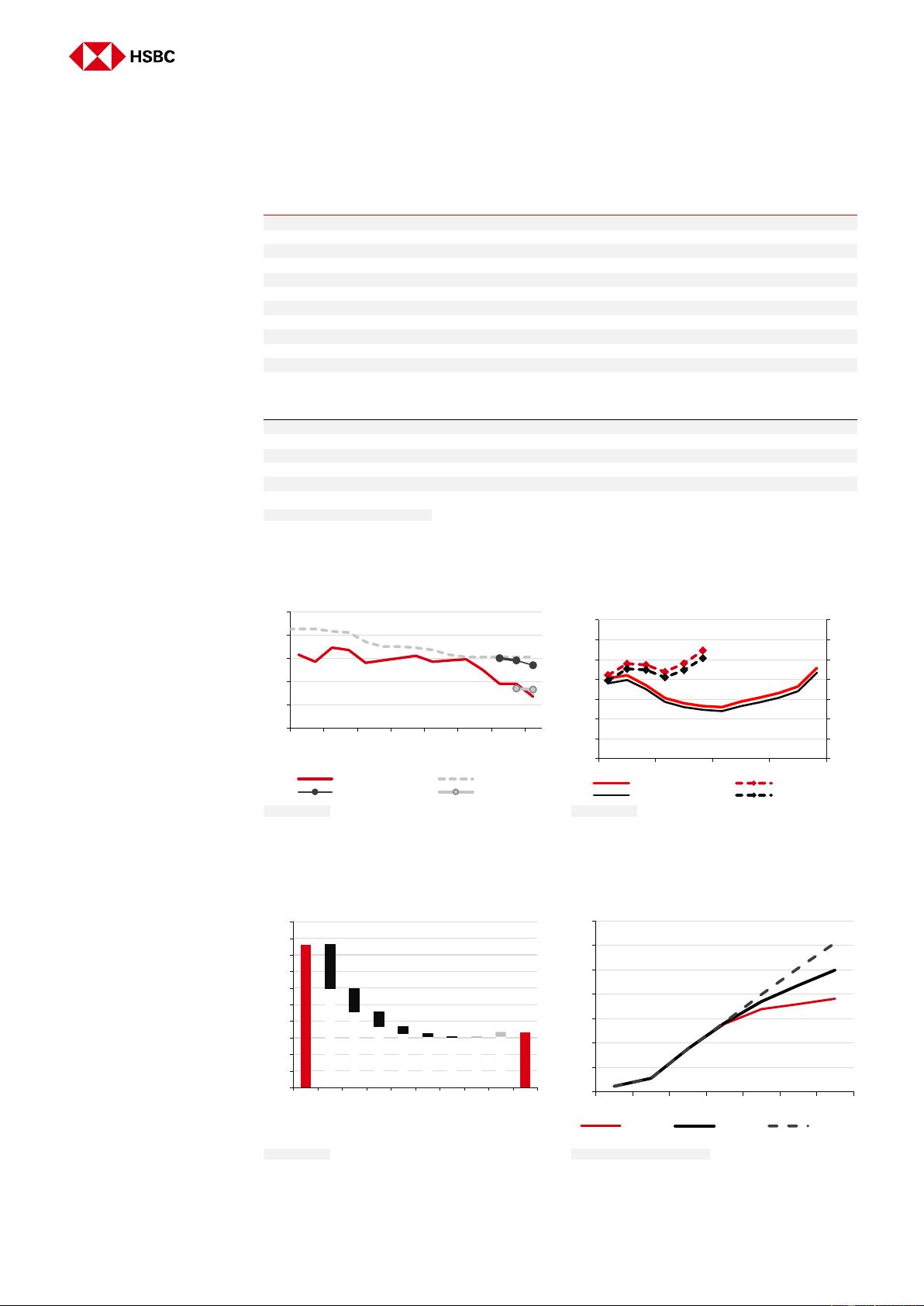

Prices languish despite harsh OPEC cuts: OPEC supply has fallen by 2.7mbd

since November as a result of aggressive production cuts (more than 1.4mbd from

Saudi Arabia alone) and involuntary losses from Iran and Venezuela. Despite this,

prices have remained under pressure from a combination of strong US supply growth

(+2mbd y/y), rising OECD inventories and sentiment dominated by demand risks.

Near-term price support? We have moved into the period where seasonal demand

strength should allow significant stock draws in the coming months. This should lend

some near-term support to prices, provided it shows up in OECD stocks and the

macro environment doesn’t deteriorate further.

Not much relief in 2020: it is hard to see the market tightening in 2020. Once again

we expect non-OPEC supply growth (+2.0mbd) to outstrip demand growth

(+1.1mbd), leaving virtually no room for OPEC to increase supply from current levels,

and needing its supply cuts to be sustained through the year if significant oversupply

and inventory builds are to be avoided.

Where are the main risks?

We see two main upside risks for prices: 1) a less pessimistic market view on the

demand outlook, particularly if US/China trade issues are resolved, and 2) a

commitment to deeper cuts from OPEC/non-OPEC, which could be possible

ahead of the seasonally weak 1Q20 given the soft outlook for balances next year

On the downside, a further worsening of the global economic outlook or an

easing of export sanctions on Iran or Venezuela could put more pressure on

prices. However, the real downside risk (though there is no sign of it at this point)

would come from any change in OPEC’s strategy of supply restraint, either from

a collapse of its accord with non-OPEC producers or from a deliberate return to

the 2014-15 policy of allowing prices to fall to squeeze out non-OPEC supply.

Lower price assumptions: We have cut our Brent crude price assumptions as

follows: 2019 from USD66.6/b to USD63.8/b (with 4Q19 at USD62/b); 2020 from

USD70/b to USD60/b, and 2021 and thereafter from USD70/b to USD65/b.

10 September 2019

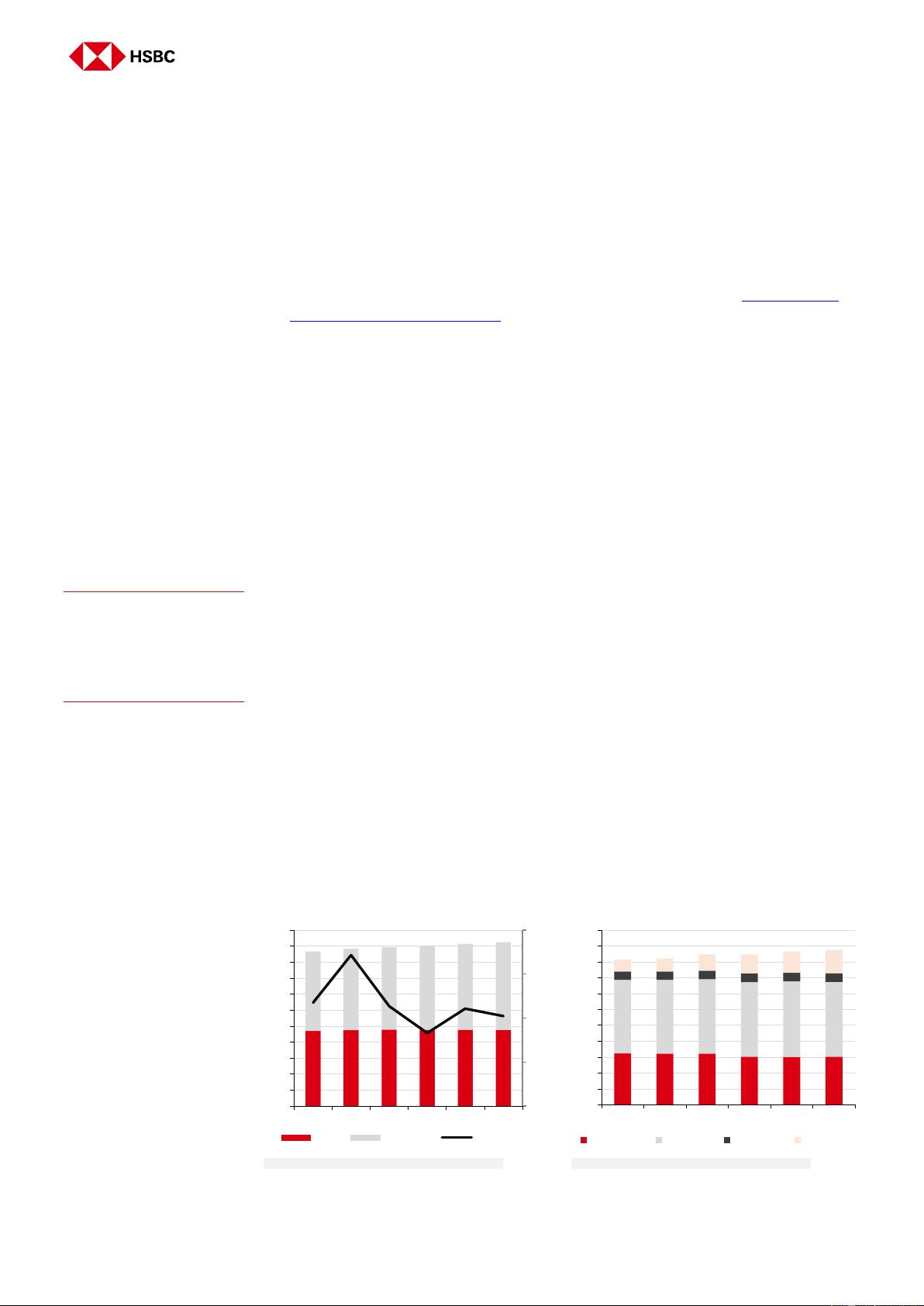

HSBC OIL AND GAS PRICE ASSUMPTIONS

Annual average

2018

2019e

2020e

2021e

Brent

1

71.6

63.8

60.0

65.0

Prev.

66.6

70.0

70.0

WTI

1

64.8

56.1

55.0

62.0

Nymex gas

2

3.07

2.60

2.50

2.75

UK spot gas

2

7.87

4.88

5.60

6.10

Quarterly average

1Q19

2Q19

3Q19e

4Q19e

Brent

1

63.7

68.3

61.0

62.0

Prev.

67.0

67.0

WTI

1

54.7

59.8

55.0

57.0

Nymex gas

2

2.9

2.5

2.4

2.6

UK spot gas

2

6.3

4.5

3.8

5.3

Note: 1 = USD/b, 2 =

USD/mBtu

Source: Refinitiv

Datastream, HSBC

Oil market outlook

Equities & Commodities

Global

Gordon Gray*

Global Head of Oil and Gas Equity Research

HSBC Bank plc

gordon.gray@hsbcib.com

+44 20 7991 6787

Charles Swabey*

Analyst

HSBC Bank plc

charles.swabey@hsbc.com

+44 20 3268 3954

Thomas C. Hilboldt*, CFA

Head of Resources & Energy Research, Asia Pacific

The Hongkong and Shanghai Banking Corporation Limited

thomaschilboldt@hsbc.com.hk

+852 2822 2922

Kim Fustier*

Analyst, Oil & Gas

HSBC Bank plc

kim.fustier@hsbc.com

+44 20 3359 2136

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is

not registered/ qualified pursuant to FINRA regulations

Cutting price deck – 2020 looks challenging

剩余23页未读,继续阅读

资源评论