汇丰银行-全球-股票策略-全球股票观点:勇敢的自由裁量权-52-23页.pdf

需积分: 0 163 浏览量

2023-07-24

17:49:14

上传

评论 1

收藏 888KB PDF 举报

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities (USA) Inc

View HSBC Global Research at:

https://www.research.hsbc.com

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE'S REPUBLIC OF CHINA (THE "PRC")

(EXCLUDING SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

With significant further market rally unlikely we trim some

cyclicals, and add to defensives and consumer

Raise Real Estate sector and cut back Materials

Consumer and Technology showing Radar improvement

We lean against market rally, trimming cyclicals and adding to defensives and

consumer. ACWI is +15% YTD and near our year-end target. We see room for an

overshoot, with consensus EPS too low at +4% vs HSBCe 8%, and valuations

supported by low bond yields and equity volatility (see Room to run?, 21 April), but

most of the return for the year is likely made. We do a deep-dive on two of the

smallest and least understood sectors: Real Estate and Materials.

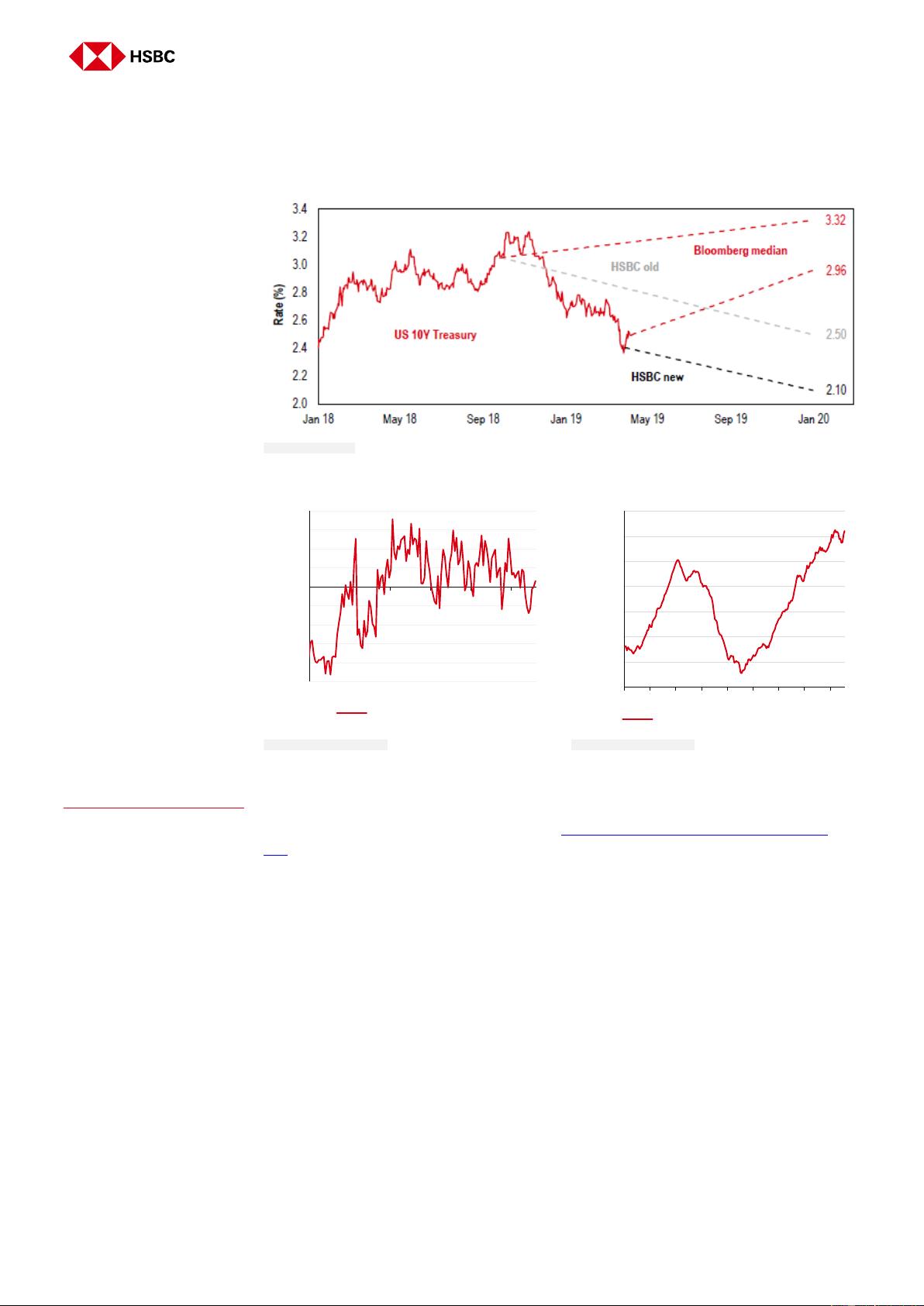

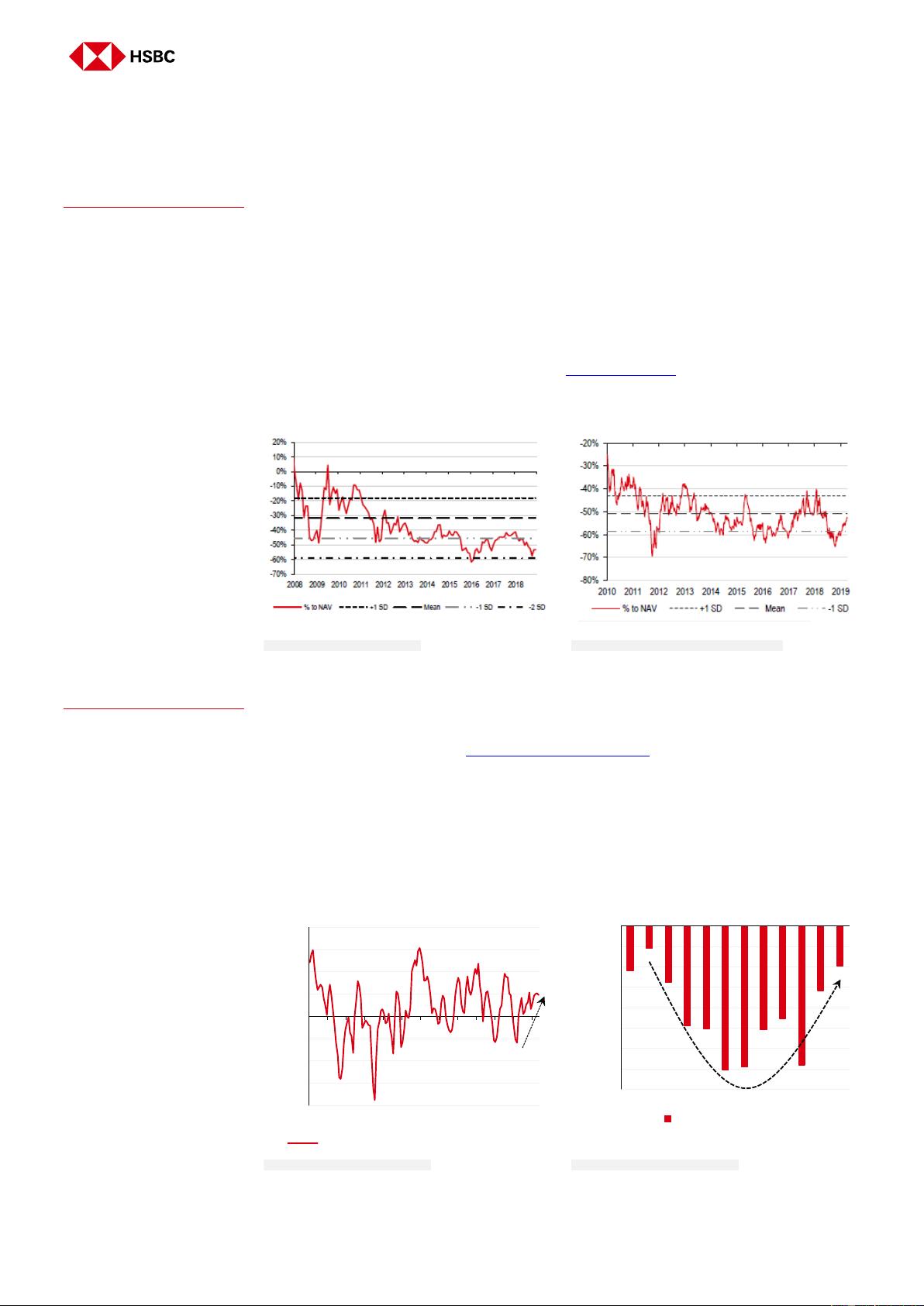

Raise Real Estate to overweight, supported by our lower-for-longer 2.1% US 10-

year yield forecast, and rising DM real wages, with the sector out-of-favor but seeing

strong relative dynamics. US and China/HK account for three-quarters of the sector,

with HSBC real estate analysts particularly highlighting Hong Kong. See page 8 for

HSBC Buy-rated stocks, from Germany’s Adler to Hong Kong’s Wheelock & Co.

Cut Materials to underweight, with sector dynamics deteriorating though it’s in favor

with investors; 45% is Chemicals and 9% Construction Materials, with less than 40%

Metals & Mining. Earnings weakness is led by Chemicals, where we do not see supply

rebalancing until mid-2020. See chart 28 for HSBC Buy-rated stocks in Construction

Materials, which is more correlated with infrastructure and Real Estate. See chart 27 for

HSBC Reduce-rated Materials stocks. HSBC Radar highlights (page 13) include:

1) Consumer improvement. Accelerating DM wage growth and falling core inflation

is driving real wages and consumer earnings revisions. Food & Beverage and Retail

now enter the attractive top-left Radar quadrant, alongside Household Products.

2) Technology less bad. Tech Hardware saw a significant upward Radar move, and

Semiconductors also nudged higher, supporting recent strong performance. Both

remain out of favor with investors, especially in US. We are overweight the IT sector.

3) Financials unattractive. The macro environment is challenging for the largest

global sector, with low bond yields, flat curves, and slowing GDP growth. Earnings

revisions have turned more negative, and the sector remains well-liked by investors.

4) Energy improvement may be short-lived. The sector was one of the largest

Radar risers this month, with earnings revisions following the oil price. With Brent

now above our forecast, and with sector risks asymmetric, we are neutral-weighted.

See www.research.hsbc.com/Radar for our interactive sector allocation framework

that looks for out-of-favor sectors with improving dynamics. See page 16 ‘HSBC

Radar Methodology: How it works’ for a description of the methodology.

2 May 2019

Ben Laidler

Global Equity Strategist

HSBC Securities (USA) Inc.

ben.m.laidler@us.hsbc.com

+1 212 525 3460

Alastair Pinder, CFA

Equity Strategist

HSBC Securities (USA) Inc.

alastair.pinder@us.hsbc.com

+1 212 525 4131

Amit Shrivastava*

Analyst

HSBC Securities and Capital Markets (India) Private Limited

amit1.shrivastava@hsbc.co.in

+91 80 4555 2759

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is

not registered/ qualified pursuant to FINRA regulations

Global Equity Insights

Equity Strategy

Global

Radar: Discretion over valor

剩余22页未读,继续阅读

资源评论