斯坦福机器学习讲义

需积分: 10 197 浏览量

2017-12-20

15:28:46

上传

评论

收藏 4.77MB PDF 举报

CS229 Lecture notes

Andrew Ng

Supervised learning

Lets start by talking about a few examples of supervised learning problems.

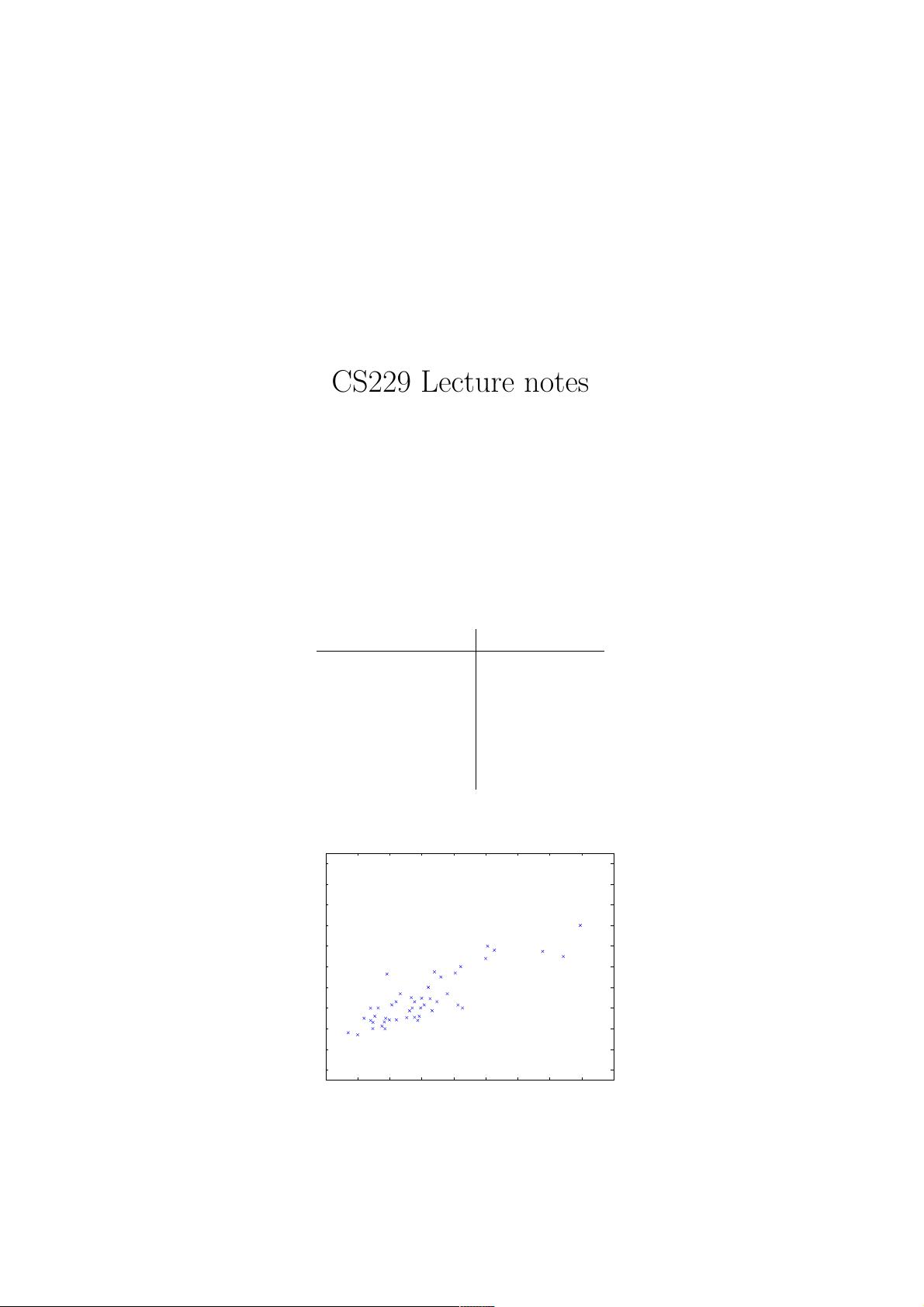

Suppose we have a dataset giving the living areas and prices of 47 houses

from Portland, Oregon:

Living area (feet

2

) Price (1000$s)

2104 400

1600

330

2400

369

1416

232

3000

540

.

.

.

.

.

.

We can plot this data:

500 1000 1500 2000 2500 3000 3500 4000 4500 5000

0

100

200

300

400

500

600

700

800

900

1000

housing prices

square feet

price (in $1000)

Given data like this, how can we learn to predict the prices of other houses

in Portland, as a function of the size of their living areas?

1

剩余133页未读,继续阅读

资源评论

qiuqiu374

- 粉丝: 1

- 资源: 1

最新资源

- 通道处理过程的模拟通常涉及对通道处理机制的理解与实现.txt

- Flume进阶-自定义拦截器jar包

- Dubins曲线算法讲解和在运动规划中的使用.pdf

- 上市公司-股票性质数据-工具变量(民企、国企、央企)2003-2022年.dta

- 上市公司-股票性质数据-工具变量(民企、国企、央企)2003-2022年.xlsx

- Reeds+Shepp曲线算法讲解和实现.pdf

- 毕业设计基于SpringBoot+MyBatisPlus+MySQL+Vue的外卖配送信息系统源代码+数据库

- 词向量(Word Embeddings)是自然语言处理(NLP)领域的一种重要技术.txt

- Surfer,线性函数

- MyBatis 的动态 SQL 是其核心特性之一.txt

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈