巴克莱-美股-医疗保健行业-美国生命科学与诊断行业展望-13-397页.pdf

需积分: 0 71 浏览量

更新于2023-07-26

收藏 5.72MB PDF 举报

《美国生命科学与诊断行业展望:工具与诊断的避风港》

在医疗保健行业中,美国的生命科学工具与诊断行业被视为一个相对稳定的领域。2018年虽然以动荡收尾,但该行业仍然跑赢市场,实现了10%的增长,而同期S&P 500指数下跌了6%,这表明其具有一定的抵御风险能力。2019年的展望中,我们预计生命科学工具与诊断将继续保持强劲的增长势头。

生物制药行业将继续作为增长引擎。随着对研发投资的增加,生物制药公司对创新技术和差异化服务的需求不断增长,特别是在生物制品生产、伴随诊断(CDx)以及合同研究组织(CRO)的服务方面。近期的融资和投资数据显示出积极的态势,这为工具类公司的增长提供了有力支持。

全球范围内对学术研究的资金支持将推动生命科学工具行业的发展。学术研究的进步是创新技术的重要来源,持续的投入将有助于推动行业的长期增长。

然而,尽管医疗保健行业拥有可持续的长期增长动力,但我们对诊断领域的选择仍然谨慎。近年来国家实验室面临的挑战,如临床实验室公正性法案(PAMA)带来的价格削减和整合趋势,是我们关注的主要风险因素。这将对我们的实验室和诊断覆盖范围内的公司产生显著影响。

在我们2019年的展望报告中,我们特别关注了两个关键部分:

1. 冷冻电子显微镜(Cryo-EM)调查——分辨率革命:通过对17家客户的访谈和调查,我们发现Thermo Fisher Scientific收购FEI后的Cryo-EM技术在结构生物学研究中开辟了新的机会,客户反馈非常积极。结合Thermo Fisher的客户服务理念和战略,我们将其选为我们的首选股票。

2. Jack的工作板——推出生命科学工具与诊断职业追踪器:我们利用网络爬虫技术监控覆盖范围内公司的招聘活动。初期发布时,我们注意到MYGN(未上市)在基因检测领域的招聘活动增加,这可能预示着公司在这一领域的扩张和技术创新。

美国生命科学工具与诊断行业在2019年将面临机遇与挑战并存的局面。投资者应关注行业内的技术创新、市场需求以及政策影响,以做出明智的投资决策。同时,对于那些能够提供独特价值和应对市场变化的公司,如Thermo Fisher Scientific,可能蕴藏着更大的投资潜力。

Equity Research

3 January 2019

FOCUS

U.S. Life Science Tools & Diagnostics

2019 Outlook: Tools & Dx a Relative

Safe Haven, TMO Our New Top Pick

Looking into 2019, our view is that Life Science Tools & Diagnostics should continue

to be a relative safe haven in healthcare. While 2018 ended on a rocky note, the group

again outperformed the market – up 10%, vs the S&P 500 down 6%. Looking across

end markets, we believe biopharma will remain a growth engine supported by R&D

investment. The push toward personalized medicine drives demand for bioproduction,

CDx, and differentiated offerings from the CROs. Recent data on funding and

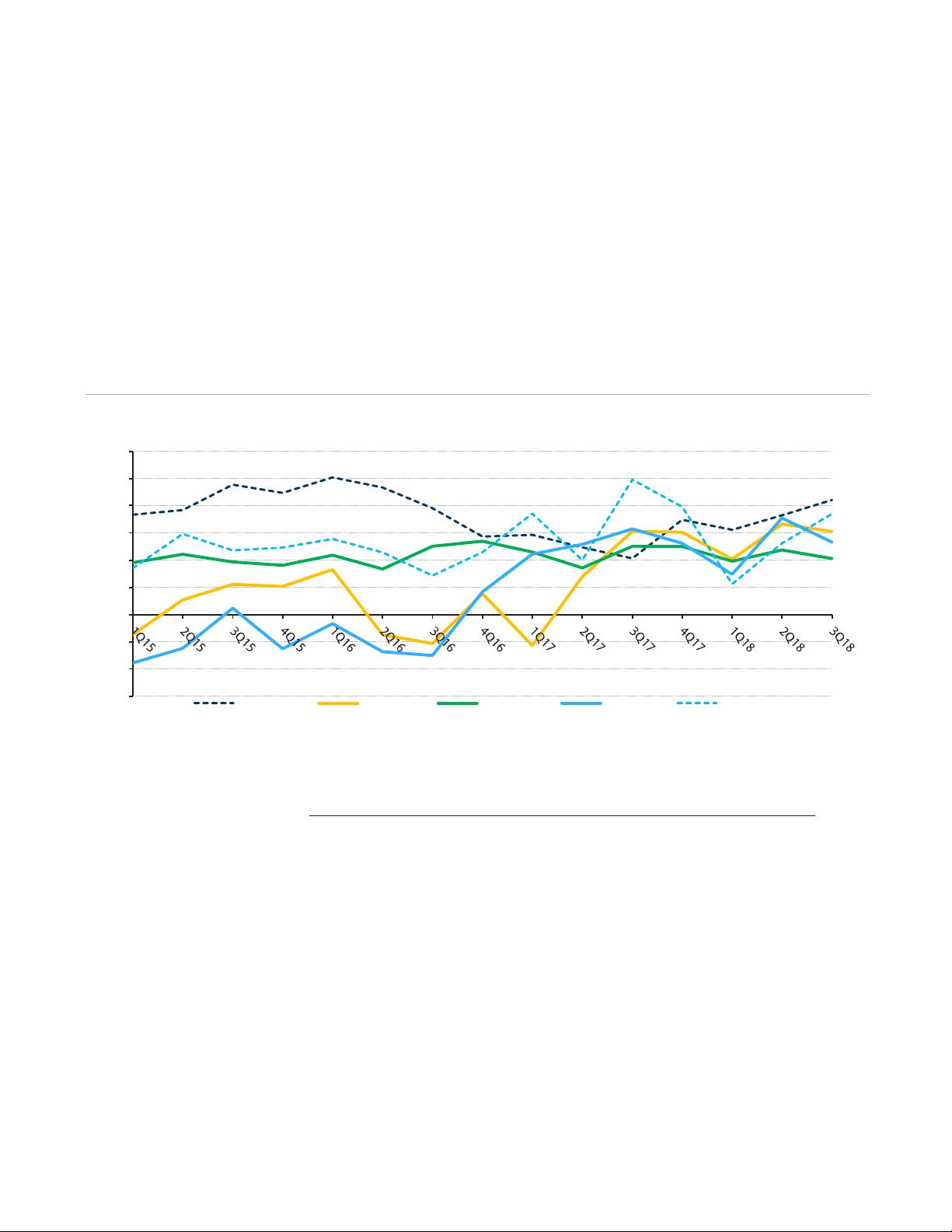

investment has been strong. Additionally, industrial macro datapoints provide 2-3

quarters of visibility into end market momentum, an important growth driver for our

Tools coverage. Next, global support for academic funding should continue to drive

LSD growth. Finally, while healthcare has sustainable long-term drivers of growth, we

remain selective in Dx given recent challenges at the national labs. PAMA remains a key

risk, where cuts and consolidation are major themes for our labs & Dx coverage.

We highlight several proprietary sections of our 2019 Outlook:

- Cryo-EM Survey – the Resolution Revolution, TMO Our Top Pick: Customer

feedback on Cryo-EM is very positive – further strengthening the strategic rationale of

Thermo Fisher’s FEI acquisition, and our conviction that the company can sustain peer-

leading growth into 2019. In 4Q18, we performed a series of interviews and survey of

17 customers. Feedback was very positive on how Cryo-EM at FEI is pioneering new

research opportunities in structural biology. Coupled with Thermo Fisher’s customer

value proposition and compelling strategy, we designate TMO as our Top Pick.

- Jack’s Job Board - Launching our Life Science Tools & Dx Careers Tracker: We are

using web-scraping to monitor hiring activity for our coverage universe. For our initial

publication, we highlight A) MYGN (UW): increased GeneSight sales rep openings,

almost 30% annualized since April. B) HOLX (EW): adding “Customer Success

Managers” at CynoSure, while GYN Surgical openings have increased. C) CROs: a

significant increase in the number of employees being hired, which could suggest an

approaching inflection in revenue growth. IQV’s (OW) hiring stands out among peers.

- Lab Survey Says: Network Access Drives Share Changes to Start 2019: We surveyed

primary care docs (n=50) on lab ordering patterns with upcoming network access

expansion. 1) Quest (OW) is expected to gain share (+570bp to 36.1%), predominantly

at the detriment of hospital based labs (-360bp to 19.8%). LabCorp (OW) is expected to

lose modest share (-80bp to 28.6%). 2) Quest and LabCorp were expected to gain

share with 16 and 22 physicians, respectively; a wide margin over hospital labs (3) and

other independent labs (1). 3) Regionally, Quest’s strength was broad-based.

Actions: We designate Thermo Fisher (TMO) as our Top Pick, and raise our PT to $280.

We also upgrade Bio-Rad (BIO) to OW. Finally, we lower our PTs on Myriad Genetics

(MYGN) to $21 and Syneos Health (SYNH) to $45.

In this report, we provide a comprehensive update on the Life Science Tools,

Diagnostics, Labs & CRO industries – including our proprietary end market trackers

and industry overviews. Please join us for a 2019 Outlook conference call today,

January 3, at 11:00am ET: Dial-in: 1-800-706-8249, Passcode: 7757098.

INDUSTRY UPDATE

U.S. Life Science Tools & Diagnostics

NEUTRAL

Unchanged

For a full list of our ratings, price target and

earnings changes in this report, please see

table on page 2.

U.S. Life Sc

ience Tools & Diagnostics

Jack Meehan, CFA

+1 212 526 3909

jack.meehan@barclays.com

BCI, US

Mitchell Petersen

+1 212 526 3367

mitchell.petersen@barclays.com

BCI, US

Andrew Wald

+1 212 526 9436

andrew.wald@barclays.com

BCI, US

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only a single factor in making their investment decision.

PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE

391.

剩余396页未读,继续阅读

资源评论

xox_761617

- 粉丝: 29

- 资源: 7802

最新资源

- 基于Springboot+Vue的影院订票系统的设计与实现-毕业源码案例设计(源码+数据库).zip

- 基于Springboot+Vue的疫情管理系统-毕业源码案例设计(高分项目).zip

- 基于Springboot+Vue的影城管理电影购票系统毕业源码案例设计(95分以上).zip

- 贝加莱控制系统常见问题手册

- uDDS源程序subscriber

- 基于Springboot+Vue的游戏交易系统-毕业源码案例设计(源码+数据库).zip

- 基于Springboot+Vue的在线教育系统设计与实现毕业源码案例设计(源码+论文).zip

- 基于Springboot+Vue的在线拍卖系统毕业源码案例设计(高分毕业设计).zip

- PDF翻译器:各种语言的PDF互翻译,能完美保留公式、格式、图片,还能生成单独或者中英对照的PDF文件

- 基于Springboot+Vue的智能家居系统-毕业源码案例设计(源码+数据库).zip

- 基于Springboot+Vue的在线文档管理系统毕业源码案例设计(源码+项目说明+演示视频).zip

- 基于Springboot+Vue的智慧生活商城系统设计与实现-毕业源码案例设计(95分以上).zip

- 基于Springboot+Vue的装饰工程管理系统-毕业源码案例设计(源码+项目说明+演示视频).zip

- 基于Springboot+Vue的租房管理系统-毕业源码案例设计(高分毕业设计).zip

- 基于Springboot+Vue电影评论网站系统设计毕业源码案例设计(高分项目).zip

- 基于Springboot+Vue服装生产管理系统毕业源码案例设计(95分以上).zip