JP 摩根-美股-房地产行业-美国住宅建筑:的9大问题-18-72页.pdf

需积分: 0 99 浏览量

2023-07-26

11:44:37

上传

评论

收藏 1.47MB PDF 举报

www.jpmorganmarkets.com

North America Equity Research

08 January 2019

Homebuilding

Nine Questions for 2019; We Maintain Our Cautious

Stance; Top Pick = LEN

Homebuilders & Building Products

Michael Rehaut, CFA

AC

(1-212) 622-6696

Bloomberg JPMA REHAUT <GO>

Elad Hillman

(1-212) 622-6435

Maggie Wellborn

(1-212) 622-5909

J.P. Morgan Securities LLC

See page 69 for analyst certification and important disclosures.

J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aw

are that

the firm may have a conflict of interest that could aff

ect the objectivity of this report. Investors should consider this report as only a single

factor in making their investment decision.

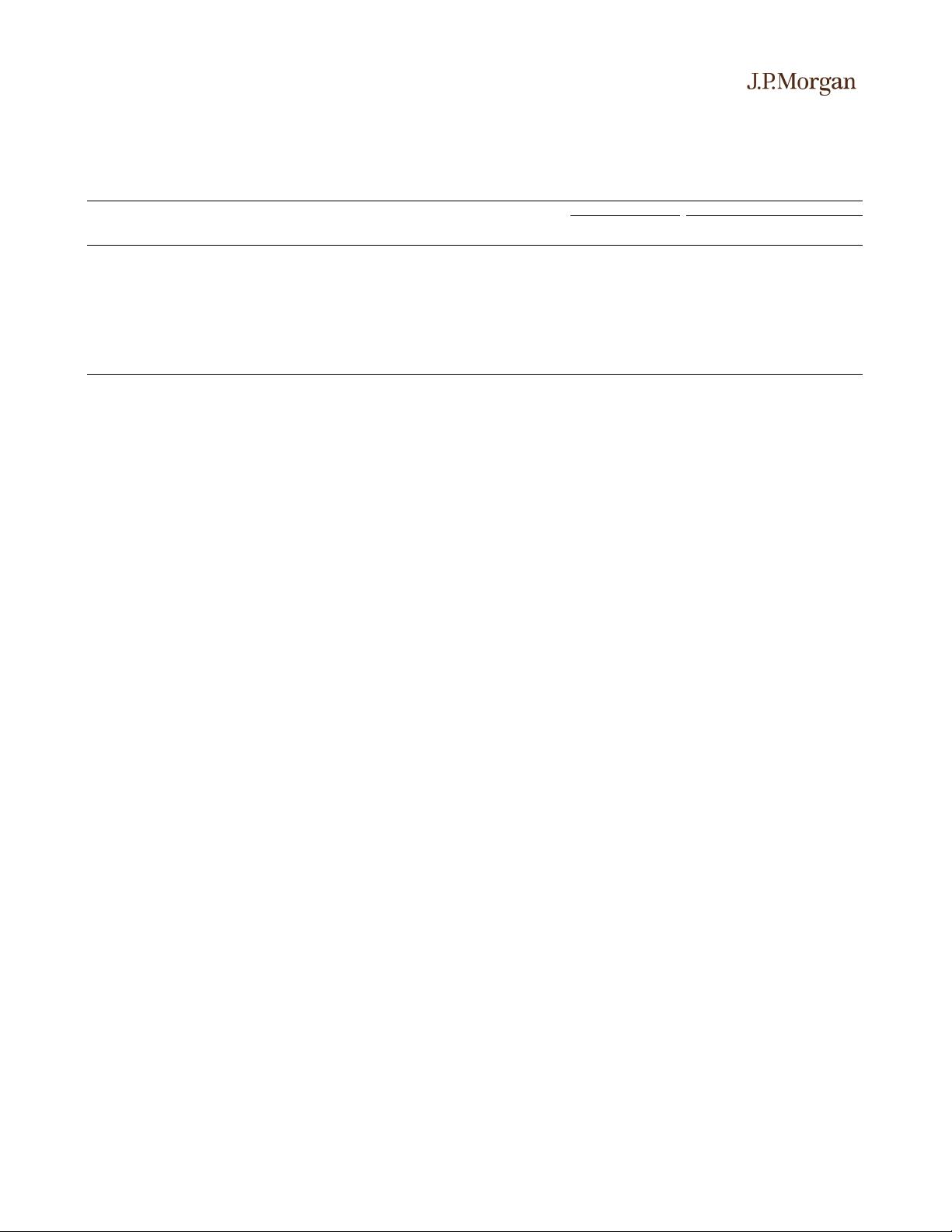

Table

1

: J.P. Morgan Coverage Universe

Homebuilders

Ticker

Rating

Larger

-

Cap

D.R. Horton

DHI

N

Lennar

LEN

OW

NVR, Inc.

NVR

N

PulteGroup

PHM

UW

Toll

Brothers

TOL

N

Smaller-Cap

Beazer Homes

BZH

N

KB Home

KBH

UW

MDC Holdings

MDC

UW

Meritage Homes

MTH

N

Taylor Morrison

TMHC

N

Higher Growth Smaller Caps

Century Communities

CCS

N

Green Brick Partners

GRBK

N

LGI Homes

LGIH

OW

William Lyon

Homes

WLH

OW

Land Development Cos.

Five Point Holdings

FPH

N

Building Products

Ticker

Rating

Beacon Roofing Supply

BECN

N

Caesarstone

CSTE

UW

Fortune Brands

FBHS

OW

Griffon Corporation

GFF

UW

Jeld

-

Wen

JELD

N

Masco

MAS

N

Masonite

DOOR

OW

Mohawk

MHK

UW

Owens Corning

OC

N

PGT Innovations

PGTI

N

Stanley Black & Decker

SWK

OW

Whirlpool

WHR

N

Source: J.P. Morgan.

Looking into the upcoming year, we offer our views on nine key questions on the

homebuilding sector that are among the most commonly asked by investors.

Regarding our sector view, following our Sector Update on 9/21/18 in which we

became more cautious and downgraded five builders, we maintain our cautious

approach to the builders, as we believe potentially higher rates, a maturing macro

cycle, rising inventory levels and downside risk to gross margins should hold

valuation multiples at current levels and hence limit upside in the stocks. Moreover,

despite already likely being reflected in the stocks’ valuations and buyside

expectations, we believe the Street’s 2019 and 2020 EPS remain aggressive, and

hence, following continued softer order trends in 4Q, we lower our 4Q, 2019 and 2020

estimates for several builders, resulting in our 2019 and 2020 EPS estimates now

being 6% and 4% below the Street (ex-higher growth small-caps), respectively, vs.

previously being in-line and 2% above. The nine questions discussed in this report

include the drivers of 2018’s performance; our 2019 outlook for housing starts (up low

single-digits) and home prices (up 1-3% at most); our outlook for the homebuilders’

growth and margins; the impact of rising rates; evaluating builders from a risk

standpoint; where are builders’ profits most exposed geographically; strongest/weakest

markets; valuation and top picks. Regarding stock selection, amid our cautious

approach, we remain limited in our Overweight-rated names and focus mainly on

compelling relative valuation opportunities. Our top pick for 2019 is Overweight-rated

LEN, while we also highlight OW-rated LGIH and WLH among the higher growth

small-cap builders. By contrast, we maintain our relative Underweight ratings on

PHM, KBH and MDC. Please join us for a conference call today at 11:00 AM ET to

discuss this report. Contact us or your J.P. Morgan salesperson for details.

1

Question 1: What drove 2018’s weak performance? Following 2017 being one

of our homebuilder universe’s best performances over the last 15 years, up 65%

(S&P 500: 19%), 2018 witnessed the worst performance for our sector since 2007,

with our universe down 36% (S&P: -6%). Interestingly, in contrast to last year’s

outperformance being more driven by non-fundamental and one-time items, in our

view (i.e., a market sector rotation and corporate tax reform), this year’s

underperformance was largely driven by fundamental drivers and concerns.

Specifically, during 1H18, investors focused on a nearly 50 bps increase in 10-year

Treasury yield, while during 2H18, order trends softened materially as consumer

demand finally began to more assertively react to a combination of higher rates and

home price appreciation over the last several years.

1

On January 3, 2018, MIFID II came into effect. Therefore, you may only be eligible to participate in this event if you have the appropriate

level of access to J.P. Morgan research. Please check your eligibility before participating/accessing.

剩余71页未读,继续阅读

资源评论