Review of Economic Studies (1998) 65, 361-393

© 1998 The Review of Economic Studies Limited

0034-6527/98/00170361$02.00

Stochastic Volatility: Likelihood

Inference and Comparison with

ARCH

Models

SANGJOON

KIM

Salomon Brothers Asia Limited

NEIL SHEPHARD

Nuffield College, Oxford

and

SIDDHARTHA CHIB

Washington University, St. Louis

First version received December 1994; final version accepted August 1997 (Eds.)

In this paper, Markov chain Monte Carlo sampling methods are exploited to provide a

unified, practical likelihood-based framework for the analysis of stochastic volatility models. A

highly effective method is developed that samples all the unobserved volatilities at once using an

approximating offset mixture model, followed by an importance reweighting procedure. This

approach is compared with several alternative methods using real data. The paper also develops

simulation-based methods for filtering, likelihood evaluation and model failure diagnostics. The

issue of model choice using non-nested likelihood ratios and Bayes factors is also investigated.

These methods are used to compare the fit of stochastic volatility and GARCH models. All the

procedures are illustrated in detail.

1. INTRODUCTION

The variance of returns on assets tends to change over time. One way of modelling this

feature of the data is to let the conditional variance be a function of the squares of

previous observations and past variances. This leads to the autoregressive conditional

heteroscedasticity (ARCH) based models developed by Engle (1982) and surveyed in

Bollerslev, Engle and Nelson (1994).

An alternative to the

ARCH

framework is a model in which the variance is specified

to follow some latent stochastic process. Such models, referred to as stochastic volatility

(SV) models, appear in the theoretical finance literature on option pricing (see, for example,

Hull and White (1987) in their work generalizing the

Black-Scholes option pricing formula

to allow for stochastic volatility). Empirical versions of the SVmodel are typically formula-

ted in discrete time. The canonical model in this class for regularly spaced data is

1,

(1)

361

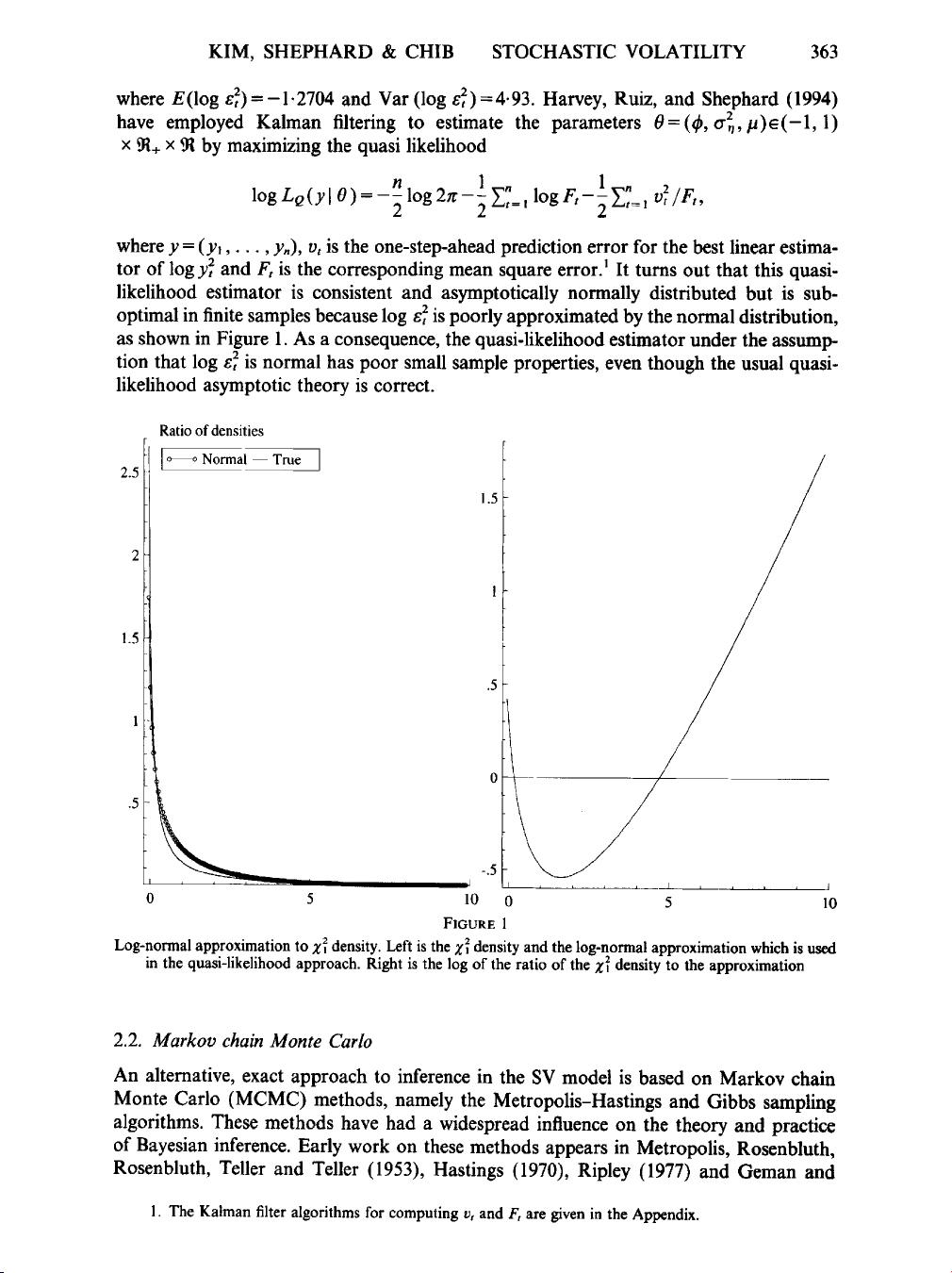

at University of Texas at Austin on October 5, 2011restud.oxfordjournals.orgDownloaded from

剩余32页未读,继续阅读

资源评论