瑞信-美股-房地产行业-Q4美国按揭REITs盈利预览:账面价值下降,但利好的Q1会缓解其影响-128-37页.pdf

需积分: 0 68 浏览量

2023-07-27

13:37:53

上传

评论

收藏 1.42MB PDF 举报

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST

CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit

Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware

that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report

as only a single factor in making their investment decision.

28 January 2019

Americas/United States

Equity Research

Mortgage Finance

Mortgage REITs

SECTOR FORECAST

Research Analysts

Douglas Harter, CFA

212 538 5983

douglas.harter@credit-suisse.com

Josh Bolton, CFA

212 325 8963

joshua.bolton@credit-suisse.com

Sam Choe, CFA

212 325 5957

samuel.choe@credit-suisse.com

4Q18 Earnings Preview: Book Value Declines,

But Favorable 1Q Update Softens The Impact

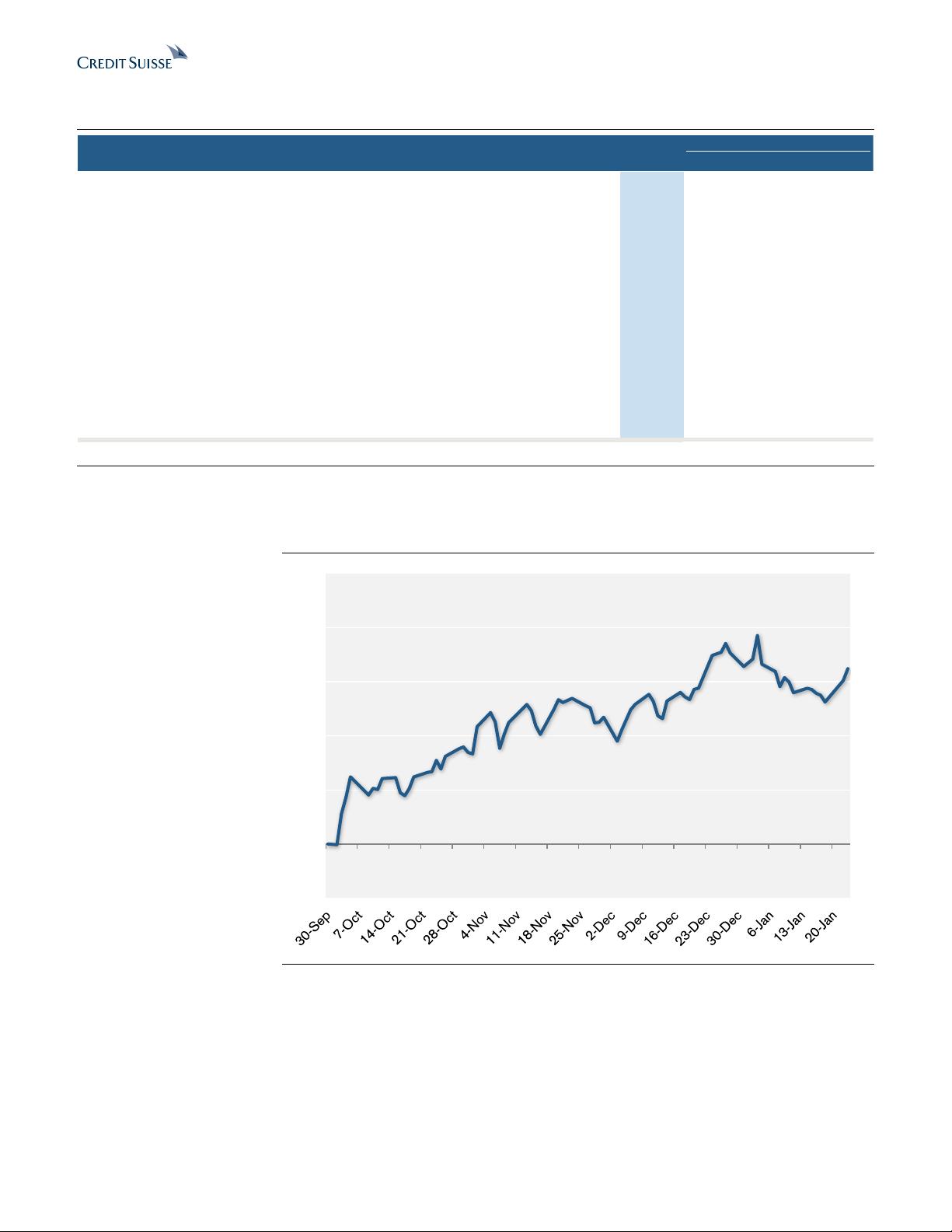

As the mREITs begin to report 4Q earnings (AGNC and CMO after the close

on 1/30) we expect to hear of a weak 4Q with a partial rebound in January.

This improved tone in markets has led to a strong start to 2019 for the mREIT

sector (up 8% on average). While the market feels stronger today we expect

volatility (from both rates and the economy) to be elevated for the year. We

continue to favor the mREITs with better risk controls and less historical

volatility in returns. Our top picks are NRZ and PMT on the residential mREITs

and STWD among the commercial mREITs; additionally we are downgrading

ANH to Underperform (from Neutral).

■ Downgrade ANH to Underperform: We are downgrading Anworth

Mortgage (ANH) to Underperform (from Neutral), and lowering our target

price to $4 (from $4.25), which represents a 18% discount to our 4Q18

book value estimate (previous target price represented 12% discount).

While ANH already trades at a 10% discount to 4Q18 book value, the

outlook for continued weak risk-adjusted returns leads us to see better total

return opportunities elsewhere in our mREIT coverage.

■ Increasing target prices 1%: We are increasing target prices by 1% on

average for the residential mREITs following the strong move in risk assets

to start 2019. The biggest change is a reduction in the expected

non-Agency price declines. We continue to expect modest Agency MBS

spread widening for the full year 2019, despite the strong start to the year.

■ Estimates: We are changing estimates on 14 mREITs given a delay in the

timing of the next Fed Funds increase to September and December (from

March and June). This is directionally positive for the residential mREITs

and negative for the commercial mREITs, but of relatively small magnitude

(2019 estimates increased by 1% on average).

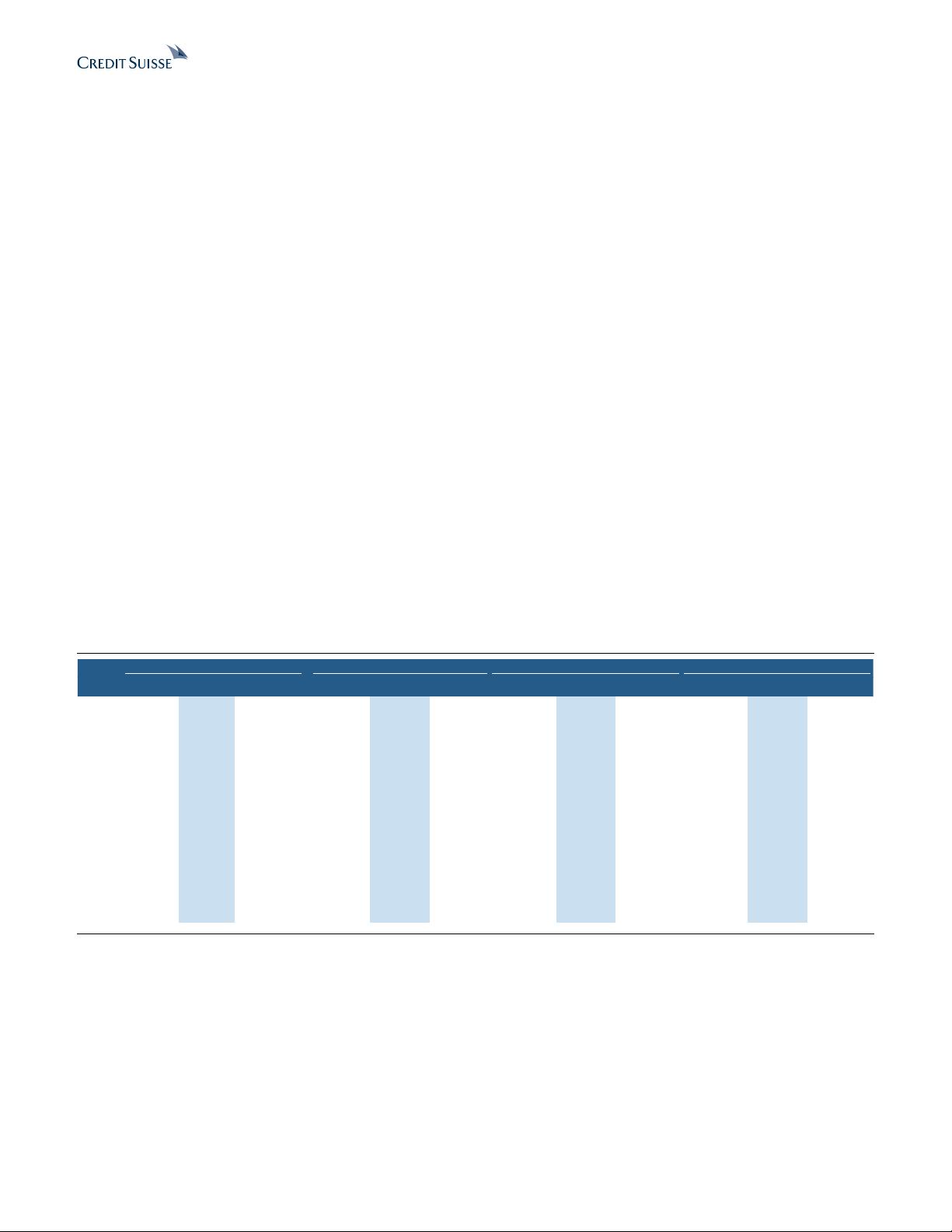

■ Residential mREITs 4Q book values challenging, but 1Q off to a good

start: The fourth quarter was a challenging quarter for the mREITs with an

expected 4.8% decline in book value for the quarter (on average); this is

1.5% lower than our prior estimate as spread widening in December was

greater than our initial read on January 2. This weakness can be seen in

the 4.6% decline in book value posted by ARR in December. On a positive

note we expect management commentary about January book value

performance to be positive given the improved tone in risk assets, including

Agency MBS (spreads tighter by 1-3 bps month to date); as of January 25

we estimate that 1Q book values are up 0.5-1%. The historical correlation

between Agency MBS spreads and risk assets (S&P 500 as a proxy)

remains elevated compared to the long-term average, which has reduced

the attractiveness of Agency-focused mREITs as a relatively safer haven in

these periods of market volatility.

剩余36页未读,继续阅读

资源评论