2020年3月13日

吕漫妮

3

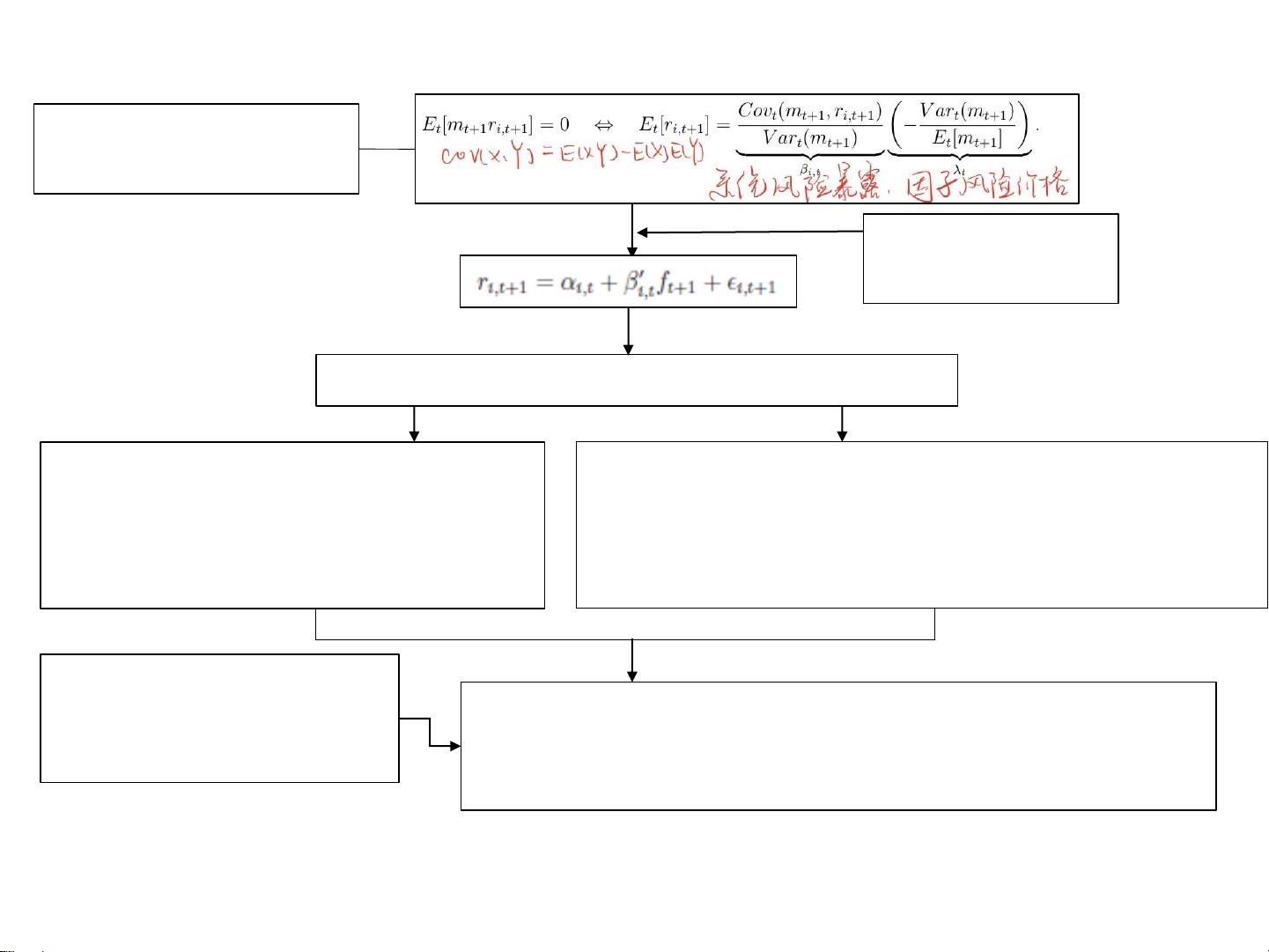

the Euler equation for

investment returns

Discount factor is

linear in factors.

The factors and loadings are unobservable, how?

Treats these factors as observable by

the econometrician, and estimates

betas and alphas via regression

e.g. Fama and French (1993).

Treats risk factors as latent and use factor analytic

techniques, such as PCA, to estimate the factors and

betas, e.g. Chamberlain and Rothschild (1983) and

Connor and Korajczyk (1986).

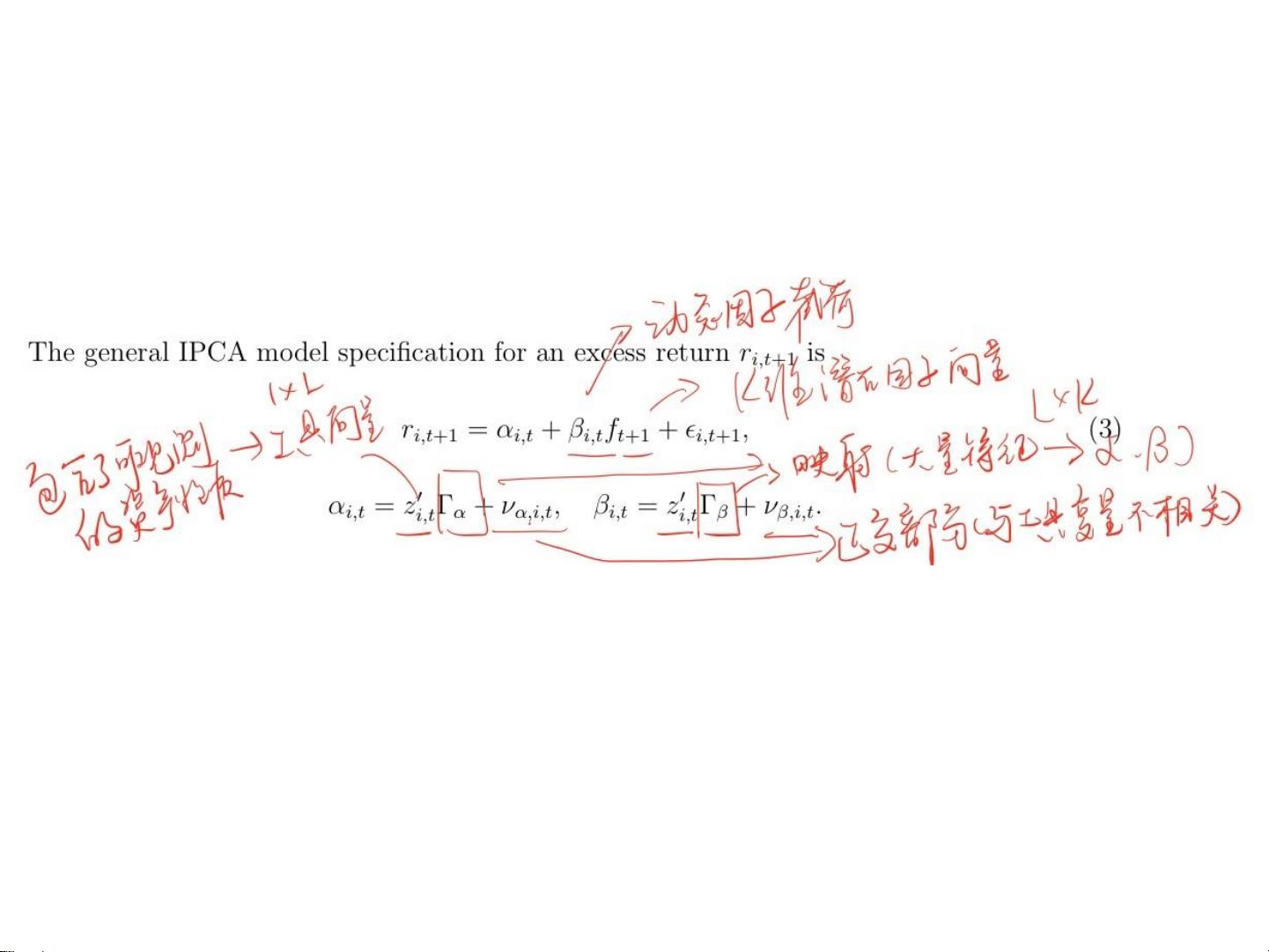

Instrumented Principal Components Analysis (IPCA)

allows factor loadings to partially depend on observable

asset characteristics that serve as instrumental variables.

Why different assets earn

different average returns?

Models stock returns as a

function of many

characteristics at once

评论0