瑞信-美股-银行业-美国大型银行业Q4盈利预览-18-32页.pdf

需积分: 0 115 浏览量

2023-07-26

11:59:20

上传

评论

收藏 853KB PDF 举报

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST

CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit

Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware

that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report

as only a single factor in making their investment decision.

8 January 2019

Americas/United States

Equity Research

Large Cap Banks

Large Cap Banks

4Q18 Earnings Preview

EARNINGS

Research Analysts

Susan Roth Katzke

212 325 1237

susan.katzke@credit-suisse.com

Adam Krasner, CFA

212 325 7116

adam.krasner@credit-suisse.com

Gerard Padilla

212 325 3579

gerard.padilla@credit-suisse.com

Past as Prologue for the Present? It's All

About the Forward Look

The CS Large Cap Bank group will begin reporting fourth quarter earnings on

Monday morning January 14

th

; Citigroup weighs in first. What to expect…

mixed fundamentals, seemingly well understood. Slower top line growth is

to be expected (moderate loan growth; limited net interest margin expansion;

weak mortgage banking; challenging market environment); operating leverage,

still very low credit costs and a greater benefit from share repurchases (the

silver lining to lower share prices) provide EPS support. All in, we forecast

~22% yr-to-yr EPS growth with a respectable ~14% average ROTE. More

important is the forward look, with earnings growth and ROTE prospects

tied to macro strength, market health and competitive positioning.

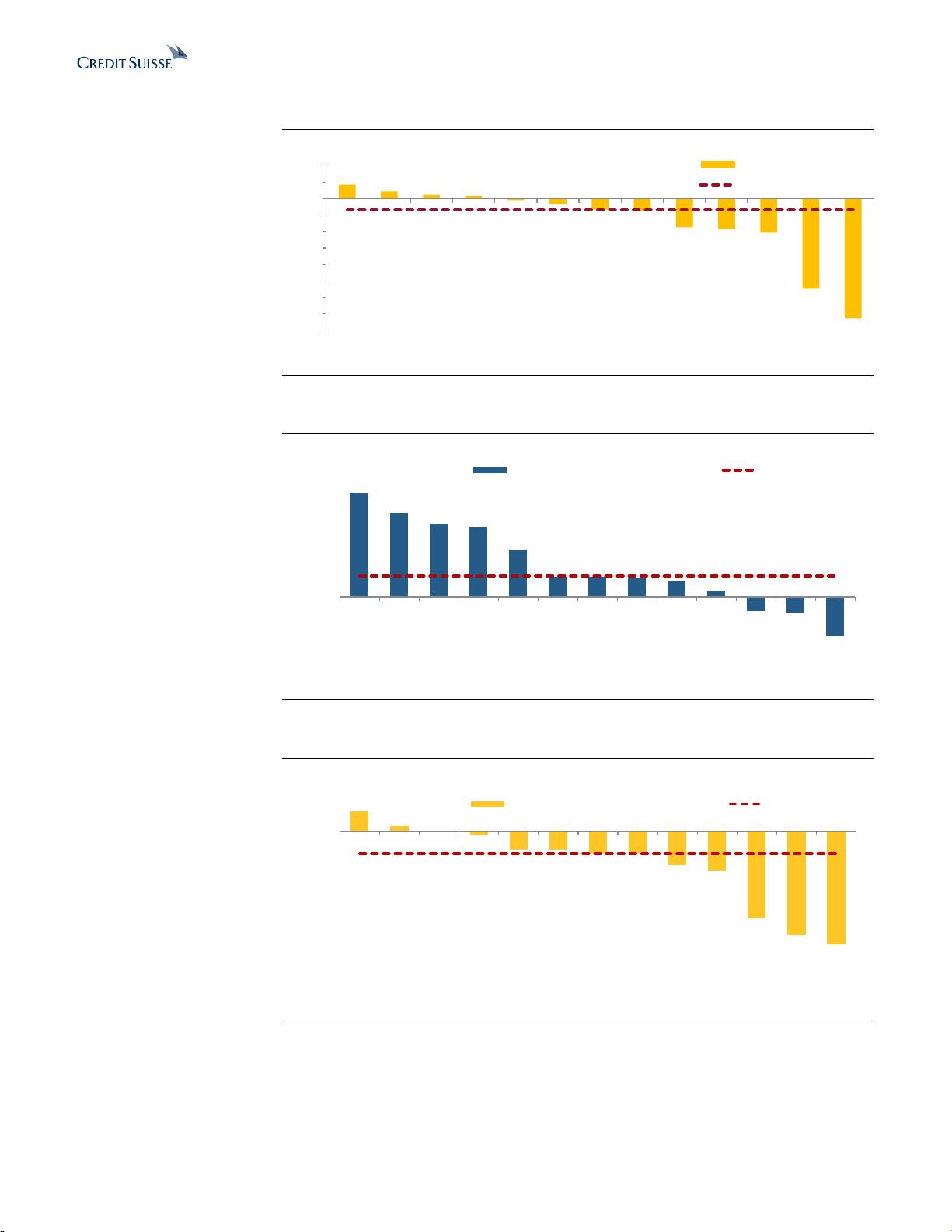

■ Large Cap Banks' 4Q18 EPS expected to increase 22% yr/yr but

decline 3% qtr/qtr (consensus similar, on average). Excluding the

benefit of tax reform, we note slower but still quite healthy growth, with

pretax income expected to increase 16% yr/yr (comparisons reflect

additional spending in 4Q17 post tax reform). With less of a market-related

revenue headwind, the Mid Cap Banks are expected to put up stronger

results, with consensus forecasting +27% yr/yr and 3% qtr/qtr EPS growth.

■ Some revenue growth, some operating leverage realization, low credit

costs and more valuable capital returns are driving comparisons.

Underpinning our +3% yr/yr and flattish qtr/qtr revenue growth forecast: (i)

flattish NIMs; modest sequential NII growth, (ii) no more than 1% sequential

quarter loan growth; slower deposit growth will manifest unevenly, from

both a volume and price perspective, and (iii) challenging capital markets

conditions: trading flat to down 5% yr/yr (down 15-20% sequentially);

investment banking down 13% yr/yr industrywide. We expect the Large

Cap Banks' efficiency ratios to average out at ~59% (ex. trust banks)

driving nearly 100bps of incremental improvement in 2018. With respect to

credit... our 4Q18 estimates embed ~20% sequentially higher credit costs—

modest, if any increase in net charge-offs with comparisons most impacted

by less loan loss reserve depletion/some additions.

■ What we're watching… (i) competitive dynamics--loan and deposit

pricing and the impact of the shape of the curve on liquidity deployment

and NIM prospects (we expect this will be a focus point on conference

calls); (ii) financing demand—C&I loan growth and capital markets

activity; (iii) the cost of market value weakness and volatility/capital

markets health--investment banking pipelines (underwriting pipelines and

strategic dialogue) and the health of the trading markets (will we see an

ability to monetize volatility in 1Q19); (iv) operating leverage/investment

spend; (v) credit quality migration, and (vi) regulatory reform—CCAR

and CECL in focus (2019 CCAR instructions due out at month end).

剩余31页未读,继续阅读

资源评论