JP 摩根-亚太地区-互联网与媒体行业-九号台娱乐(NEC)与七西传媒公司投资策略-9-87页.pdf

需积分: 0 96 浏览量

2023-07-29

09:34:50

上传

评论

收藏 1.11MB PDF 举报

www.jpmorganmarkets.com

Asia Pacific Equity Research

11 September 2019

Nine Entertainment and Seven

West Media

NEC.AX, NEC AU

Overweight

Price: A$1.99 (10-Sep)

Price Target: A$2.55 (Jun-20)

Initiate coverage of NEC with OW rating and $2.55

PT, SWM with OW rating and $0.65 PT

SWM.AX, SWM AU

Overweight

Price: A$0.41 (10-Sep)

Price Target: A$0.65 (Jun

-

20)

Australia

Telecom Services, Media and

Internet

Eric Pan, CFA

AC

(61-2) 9003-8207

eric.pan@jpmorgan.com

Bloomberg JPMA EPAN <Go>

Abhinay Jeggannagari

(61-2) 9003 6734

abhinay.jeggannagari@jpmorgan.com

J.P. Morgan Securities Australia Limited

Equity Ratings and Price Targets

Mkt Cap

Rating

Price Target

Company

Ticker

(A$ mn)

Price (A$)

Cur

Prev

Cur

End

Date

Prev

End

Date

Nine Entertainment

NEC AU

3,409.52

1.99

OW

—

2.55

Jun

-

20

— —

Seven West Media

SWM AU

618.21

0.41

OW

—

0.65

Jun

-

20

— —

Source: Company data, Bloomberg, J.P. Morgan estimates. n/c = no change. All prices as of 10 Sep 19.

See page 84 for analyst certification and important disclosures, including non-US analyst disclosures.

J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aw

are that

the firm may have a conflict of interest that could affect the

objectivity of this report. Investors should consider this report as only a single

factor in making their investment decision.

We initiate coverage of NEC with an OW rating and $2.55 Jun-20 PT and of

SWM with an OW rating and $0.65 Jun-20 PT. NEC has successfully diversified

its revenue base away from its traditional broadcast TV business into digital media

post the acquisition of FXJ, and its low debt level provides opportunities for

further M&A or capital return. We expect SWM to undergo a similar

transformation as the new CEO has been brought in to transform the company

through M&A, either through a sale of the company or acquisitions that will

dramatically change the revenue composition. We also expect SWM's metro TV

revenue share to catch up eventually to its industry-leading audience share.

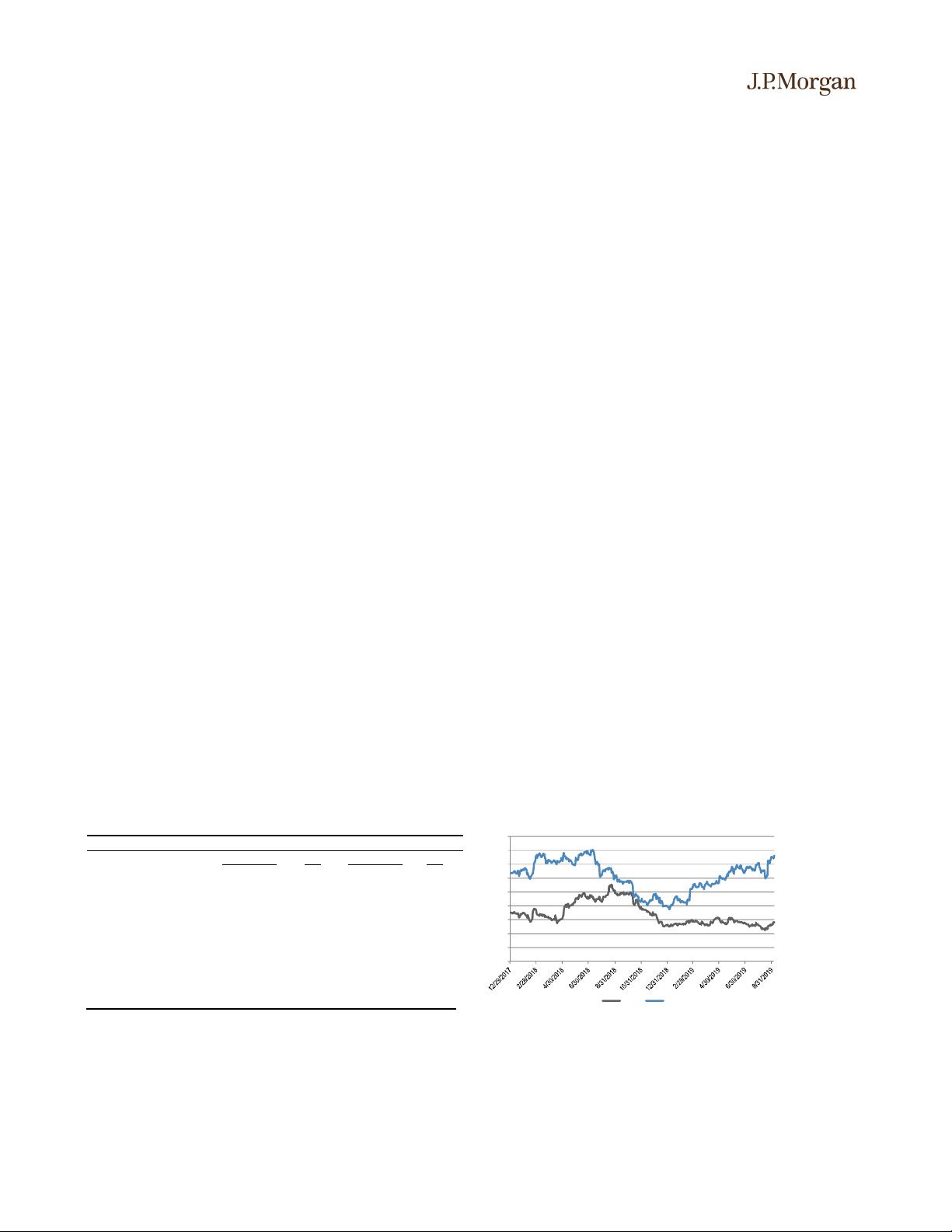

We estimate the TV ad market to decline in the low single-digits in the near

and medium term. The TV ad market has been relatively stable for the past

decade, despite double-digit declines in other traditional media, such as print.

However, the declines have recently accelerated to low single-digits over the

last one-, three- and five-year periods as more consumers take up SVOD and

BVOD programming; we expect this trend to continue for the foreseeable

future. We estimate NEC and SWM will both retain a 39% share of metro TV

ad revenues in this environment in the near and medium term, with Ten at 22%.

We initiate coverage of NEC with an OW rating and a Jun-20 PT of $2.55.

NEC has successfully diversified its revenue base away from its traditional

broadcast TV business into growth areas in digital media. With only 47% of

group revenues coming from TV, the business is now less susceptible to the

structural and cyclical headwinds of TV ad spend and its ownership of Domain

and Stan should help boost long-term growth. NEC’s low debt level should also

provide opportunities for further M&A or capital return.

We initiate coverage of SWM with an OW rating and a Jun-20 PT of $0.65.

We believe the new CEO has been brought in to transform the company through

M&A, either through a sale of the company or acquisitions that will

dramatically change the revenue composition, with the former more likely due

to its high debt level. In addition, the company is under-earning its metro TV

audience share and should see upside as its revenue share catches up.

SWM trades at a discount to domestic and global peers, while NEC is more

diversified. SWM currently trades at 4.6x FY20E EV/EBITDA and 6.4x P/E,

which is a significant discount to NEC at 7.2x and 15.3x and CBS in the U.S. at

7.6x and 8.0x. NEC derives only 47% of reported group revenues from TV, 15%

from digital and publishing, 22% from Domain and Stan and 6% from radio,

which is more diversified than CBS which derives 83% of revenues from

FTA/cable TV, 11% from local media, and 5% from book publishing.

剩余86页未读,继续阅读

资源评论