JP 摩根-亚太地区-金融行业-泰国金融业:经典的“以合理价格增长”投资-313-170页.pdf

需积分: 0 59 浏览量

2023-07-26

11:47:02

上传

评论

收藏 4.09MB PDF 举报

Asia Pacific Equity Research

13 March 2019

Thailand Financials

A classic "growth at a reasonable price" investment

Thailand Banks

Harsh Wardhan Modi

AC

(65) 6882-2450

Bloomberg JPMA MODI <GO>

J.P. Morgan Securities Singapore Private

Limited/ J.P. Morgan Securities (Asia Pacific)

Limited

Jidapa Chirawattanakarn

(66-2) 684-2326

JPMorgan Securities (Thailand) Limited

Gaurav Khandelwal

(91-22) 6157 5092

J.P. Morgan India Private Limited

Anurag Rajat, CFA

(65) 6882 2407

anurag.rajat@jpmorgan.com

J.P. Morgan Securities Singapore Private

Limited/ J.P. Morgan Securities (Asia Pacific)

Limited

See page 168 for analyst certification and important disclosures, including non

-

US analyst disclosures.

J.P. Morgan does and seeks to do

business with companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in

making their investment decision.

www.jpmorganmarkets.com

We assume coverage of Thailand financials with a positive view despite many

challenges. The key reason to own the sector is a marked step up in EPSg (10% in

2019-20), while multiples are reasonable at 10.4/1.11x P/E/P/B in our view.

Credit costs are coming off from cyclical peaks, further aided by FRS9. NIM

appears to have bottomed, with an underappreciated CASA strength. These

provide earnings visibility. The wait for capex revival has been torturous, but it

stays a potential catalyst. Fee, regulation and digital risks are known, and will

likely intensify we believe. We reflect these in our stock picks. We initiate on

SAWAD with OW, upgrade Tisco to OW, maintain OW on KTB and BBL, while

downgrading KBank to N and SCB to UW.

Earnings are scarce across Asia banks, with nine out of 10 banking sectors

delivering sub-10% EPSg. Thailand financials offer 10% EPSg this and next

year while trading at 10.4x P/E, offering growth and relative value. Credit cost

driven earnings is, by definition, cyclical. Hence, technically, these earnings do

not deserve high multiples. Yet, 2019/20 provisions of 116/101bps are coming

off highs and will likely undershoot through-the-cycle averages. Thus, the

inflection in EPS revisions for the sector is here to stay. Further, Thai banks

offer 4.9% dividend yield and a hedge against risk of a sharp dollar rally.

Re-rating depends on PPoP growth. Our investment case is based on EPSg,

rather than on re-rating. PPoP gr is muted at 3% for 2019-20. Challenges to

operating profit gr include low credit demand (limited capex progress), NIM

stagnation (limited policy rate transmission), fee income decline (migration to

PromptPay continues), and cost pressures (digital investments). Out of these, a

pick-up in infrastructure investments and loan yield hike post elections are more

likely than the rest. Further, higher trade (50% exports/GDP) can lead to

cyclical revival in corporate capex. These pose upside risks to our forecasts.

M&A is likely and a risk to large banks. Equity and liquidity are ample in this

banking system (13% E/A and 1.4% BoP surplus), while credit gr is limited.

This, along with payout reluctance at large banks has likely lowered RoI hurdle

rate for a deal. This is positive for smaller banks as possible targets but

increases the risk of value eroding deal from large banks. On the flip side, an

increase in payout will partly address the risk, reflecting in higher multiples.

What could go wrong? Inventory build-up was high in last 6M. This could

derail AQ recovery, if it continues. Even after coming off 20bps in last 3Y, non-

interest income as a percentage of assets for Thai banks is higher than Asian

average. This suggests risk of further correction. The large banks have high

CASA ratio. This is a cyclical positive, if rates move up. But structurally,

CASA advantage is at risk of being undermined by digital advances, especially

PromptPay and E-KYC. Moreover, search for yield has led to a shift toward

higher-risk loans. Banks contend that use of digital channels will reduce costs,

as well as control credit risk, especially in ‘high-touch’ segments like retail and

SME. This is yet to be tested.

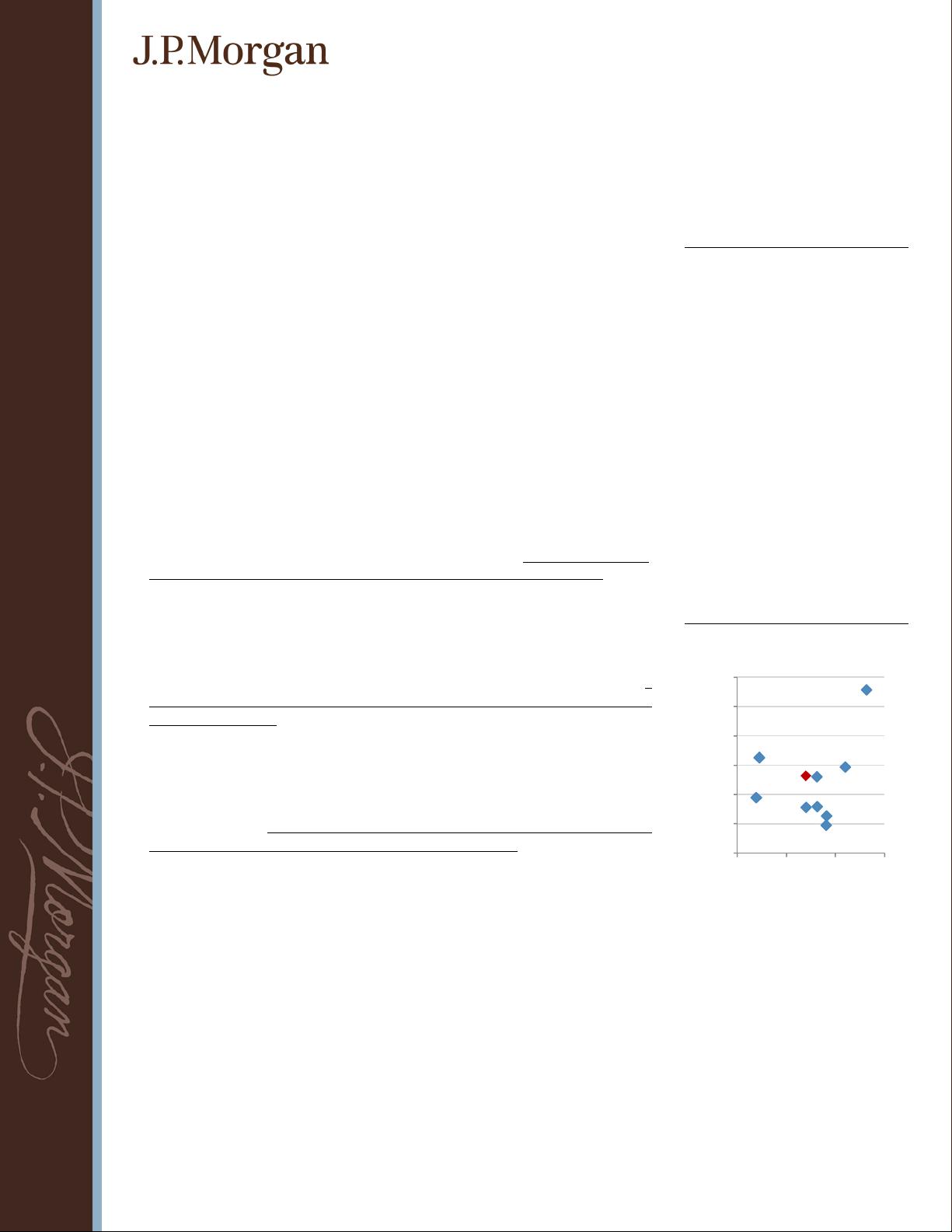

AxJ Banks: P/E vs. EPS CAGR

Source: Bloomberg, J.P. Morgan. Note: Based on 12M

fwd PE and 2018-20E EPS CAGR. Note: Thailand

excludes Sawad.

SG

ID

PH

MY

TH

IN

KR

CH

TW

HK

3%

5%

7%

9%

11%

13%

15%

3.0 8.0 13.0 18.0

EPS CAGR (18-20E)

2019E PE (x)

剩余169页未读,继续阅读

资源评论