JP 摩根-全球-石油与天然气行业-Q1石油市场季报:美国利用其能源例外主义-315-38页.pdf

需积分: 0 174 浏览量

2023-07-26

11:46:03

上传

评论

收藏 1.18MB PDF 举报

Global Commodities Research

15 March 2019

Oil Market Quarterly 1Q19

US leverages its energy exceptionalism

Global Commodities Research

Abhishek G Deshpande

AC

(1-212) 834-3102

JPMorgan Chase Bank NA

Thomas Anthonj

(44-20) 7742-7850

J.P. Morgan Securities plc

Arindam Sandilya

(65) 6882-7759

JPMorgan Chase Bank, N.A., Singapore

Branch

Prateek Kedia

(91-22) 6157-3317

prateek.kedia@jpmchase.com

J.P. Morgan India Private Limited

See page 36 for analyst certification and important disclosures.

J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aw

are that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a

single factor in

making their investment decision.

www.jpmorganmarkets.com

As risky assets focused on macro concerns, oil markets have largely

overlooked supply-side tightness in 1Q19 that has helped global oil markets

to rebalance since the end of 2018. With a potential for a US-China trade

talk resolution emerging, oil prices should finally break out of the narrow

trading range and should be supported in the very near-term due to policy-

driven supply-side tightness. The recovery is likely to fade towards the end of

2019 unless OPEC+ continues to over-comply and demand growth holds up.

In 2019, we revised down total oil products demand growth marginally by

58kbd to 1.03mbd whereas total supply growth has been revised down by

0.74mbd to 0.3mbd y/y due to OPEC+ cuts and Canadian curtailments as

assumed in our central balances. This is supportive for oil prices in 1H19. In

2H19 we are somewhat skeptical of the direction oil prices could take at this

stage given the strong price elasticity of supply and sustainability of OPEC+

cuts if oil prices or non-OPEC production were to rise unabated. At this

stage, in order to take a direction/view, we would rather give benefit of the

doubt to OPEC+ managing supply in order to avoid a surplus. Hence, we

think OPEC+ cuts will need to be extended not just to the end of 2019 but

also into 2020 if they want to avoid another oil price crash.

Given the support is very strongly pivoted on continued OPEC+ cuts (and

over-compliance), US foreign policy could very much influence those cuts as

neither US nor OPEC wants oil prices to rally too high at this stage of global

economic expansion. Talks of US SPR release and NOPEC bill could gain

traction if oil prices were to rise significantly from current levels. Hence, our

risk bias is negative relative to our base case scenario especially in 2H19 when

US supply growth returns.

Oil technical: The rally off the December 2018 lows remains intact for the

time being, but coming closer to the target zone for the first leg up (A-wave)

of the broader countertrend rally, usually a 50% retracement of the

preceding sell-off, we expect the up-momentum to fade in preparation of

the B-wave sell-off, which could potentially retrace 76.4% of the ongoing

wave A up.

Oil derivatives: Oil volatility has fully normalized from the multi-sigma

spike in 4Q18 when unexpected waivers on Iranian sanctions roiled

markets. Vols now screen fair vs. medium-term fundamental drivers. Oil

volatility should remain contained this year due to continued OPEC+

management of prices around $70/bbl on Brent. The lack of overvaluation

in implied volatility prevents an aggressive short vol stance; however,

cautious structuring via -M6/+M12 calendar spreads offers better risk-

reward. Bullish oil views are well-expressed via Jun’19 call spreads that

have cheapened sharply in vol, and line up timeline-wise with the Iranian

sanctions waiver deadline, an expected ramp up in Russian production

compliance ahead of the April OPEC+ meeting, and the end of the refinery

maintenance season.

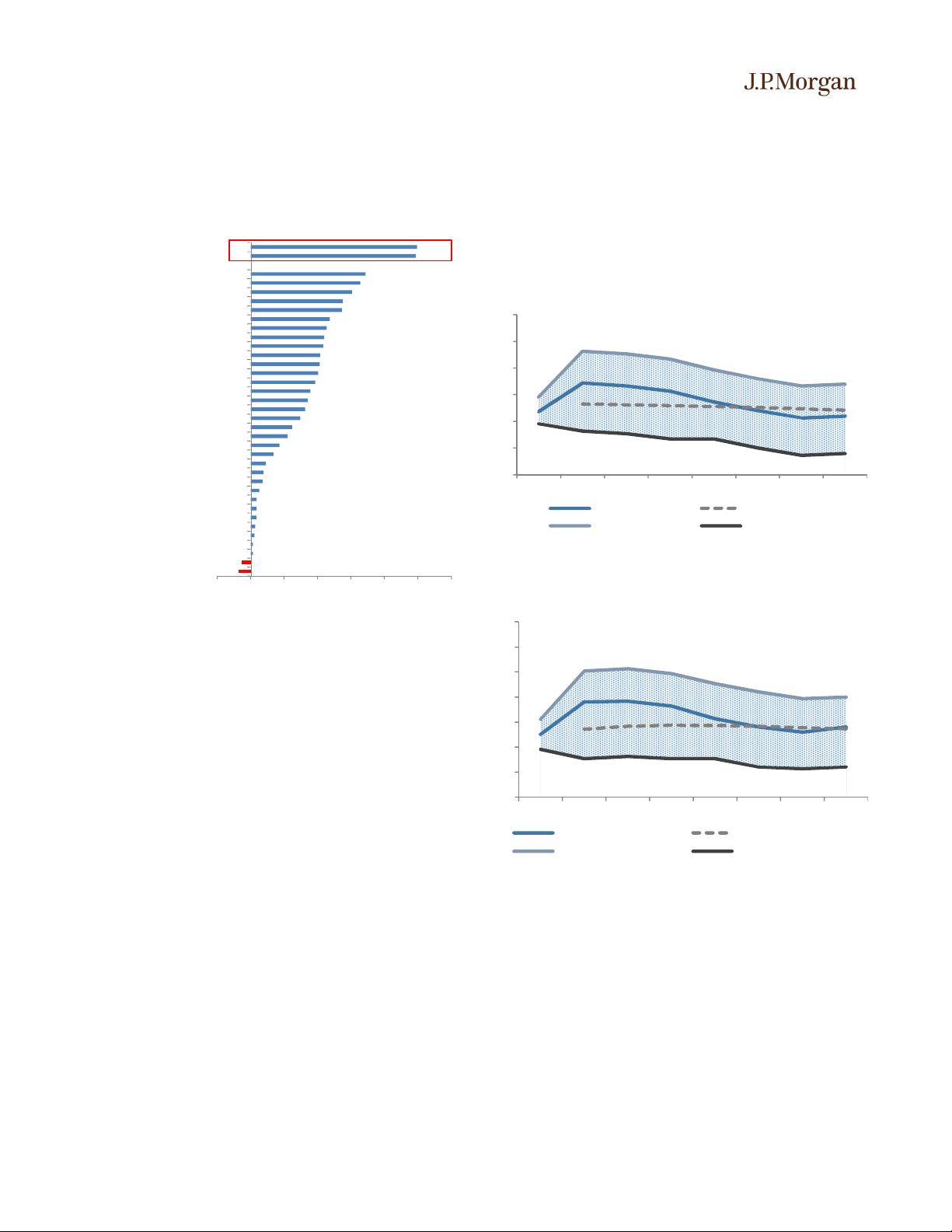

J.P. Morgan Oil Price Forecast (Brent)

$/bbl

Source: J.P. Morgan Commodities Research

J.P. Morgan Oil Price Forecast (WTI)

$/bbl

Source: J.P. Morgan Commodities Research

40

50

60

70

80

90

100

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20

Central Scenario Forward Curve

High Case Scenario Low Case Scenario

30

40

50

60

70

80

90

100

1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20

Central Scenario Forward Curve

High Case Scenario Low Case Scenario

剩余37页未读,继续阅读

资源评论