JP 摩根-亚太地区-交通运输业-铁路行业(JR Cos):财年第三季度后更新-213-55页.pdf

需积分: 0 8 浏览量

2023-07-24

13:40:29

上传

评论

收藏 840KB PDF 举报

www.jpmorganmarkets.com

Asia Pacific Equity Research

13 February 2019

Equity Ratings and Price Targets

Mkt Cap

Rating

Price Target

Company

Ticker

(

¥

bn)

Price (

¥

)

Cur

Prev

Cur

End

Date

Prev

End

Date

East Japan Railway (9020)

9020 JT

3,881.22

10,165

N

n/c

11,400

Dec

-

19

11,200

n/c

West Japan Railway (9021)

9021 JT

1,521.95

7,907

OW

n/c

9,200

Dec

-

19

8,800

n/c

Central Japan Railway (9022)

9022 JT

4,942.97

23,995

OW

n/c

27,800

Dec

-

19

26,100

n/c

Kyushu Railway (9142)

9142 JT

573.60

3,585

N

n/c

3,900

Dec

-

19

n/c

n/c

Source: Bloomberg, J.P. Morgan estimates. n/c = no change.All prices as of 12 Feb 19.

Railways (JR Cos): Post

-

3Q

FY2018 Update

When Concerns Arise, Count on JR

Japan Equity Research

Transportation, Real Estate, REIT

Ryota Himeno

AC

(81-3) 6736-8639

Bloomberg JPMA RHIMENO <GO>

JPMorgan Securities Japan Co., Ltd.

See page 50 for analyst certification and important disclosures, including non

-

US analyst

disclosures.

J.P. Morgan does and seeks to do business with companies covered in its research reports. As a result, investors should be aw

are that

the firm may have a conflict of interest that could affect the objectivity of this report. Investors should c

onsider this report as only a single

factor in making their investment decision.

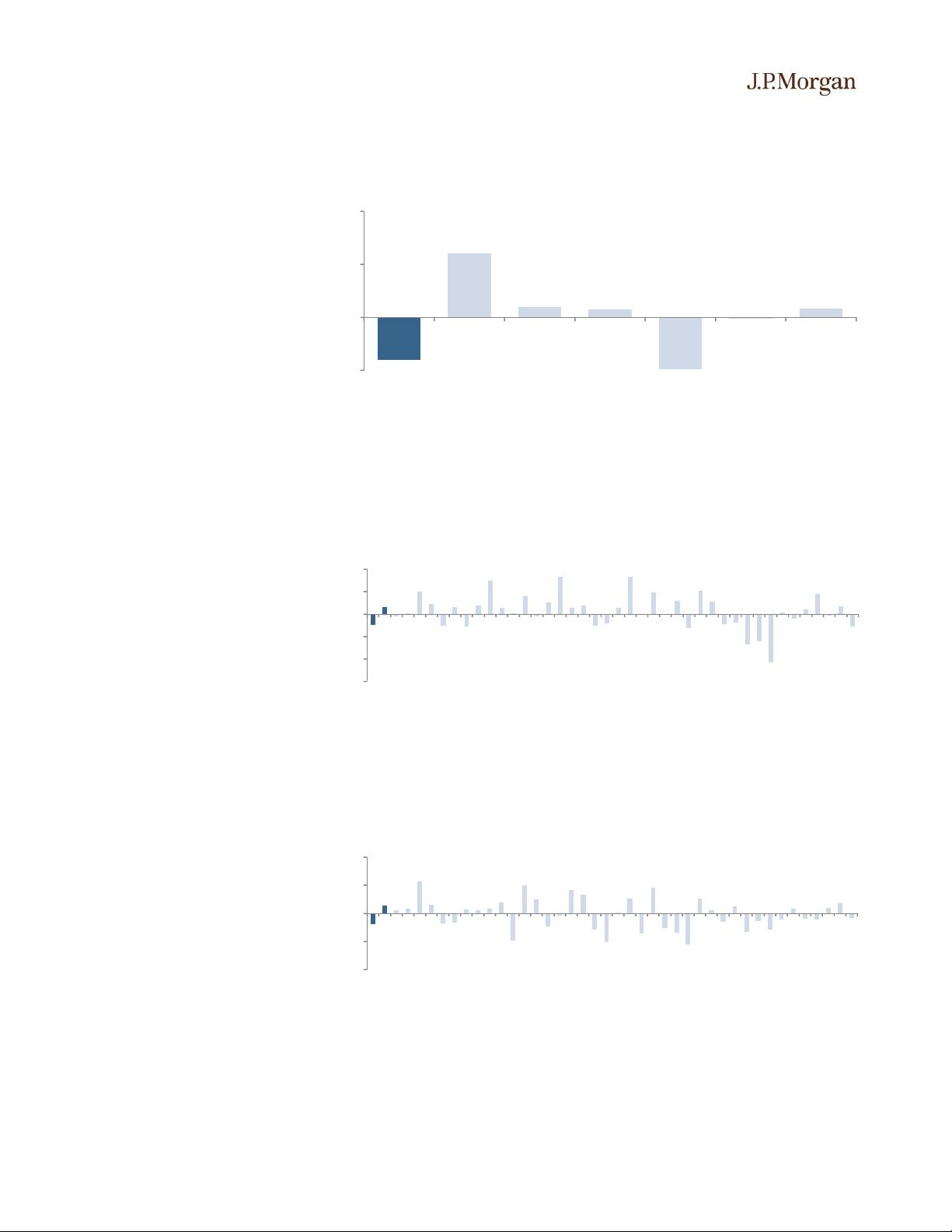

Overall, 3Q results were unsurprising at the JR companies. Although catalysts are

scant, we still have a high preference for railways in the transportation sector, as

passenger demand remains brisk and they have considerable potential as

defensive plays in an uncertain environment marked by concerns about the impact

of the planned consumption tax hike on the domestic economy and deceleration in

the global macroeconomy. Looking at the past three months with TOPIX in a

slump, performance rankings were JR companies > air transportation > logistics

> marine transportation > TOPIX. As share prices regained ground, YTD

performance has been on a par with the TOPIX.

Earnings outlook: We would not be surprised if operating profit finished 1-3%

above guidance at each company in FY2018. Excluding Kyushu Railway (JR

Kyushu), where a profit decline is likely, we forecast modest growth in profits at

each company in FY2019. However, we see guidance risk for lower profits at

East Japan Railway (JR East) and West Japan Railway (JR West), where rising

costs are a factor, and at Central Japan Railway (JR Central), where rising costs is

a limited factor but management has always had conservative revenue forecasts.

JR Central in 1H FY2019: At JR Central, we note that (1) demand is robust on

the Tokaido Shinkansen and (2) profit visibility is clear with limited risk of

higher costs over the short term. In 2H FY2019, however, the planned

consumption tax hike could become a drag on the domestic economy, and this

may heighten awareness of downside risk at JR Central, which is the most

exposed to economic trends.

JR West in 2H FY2019: At JR West, we expect revenue to bounce back in

FY2019 after natural disasters the previous year, but maintenance and repair costs

and depreciation should also increase. We look for costs to gradually decrease

from 2020, the third year of its medium-term business plan. In the event that the

domestic economy decelerates, we think JR West will be a better defensive play

than JR Central. Although its earnings structure is not as defensive as JR East, we

anticipate support for its share price from shareholder returns and dividend yields.

JR West targets a dividend payout ratio of 35% in FY2022 and intends to flexibly

buy back its own shares in order to achieve a total return ratio of 40% during the

medium-term plan.

JR East and JR Kyushu in a similar situation: Both companies have long-

term growth stories. JR East’s story entails the redevelopment of the Shinagawa

剩余53页未读,继续阅读

资源评论