This document is intended for institutional investors and is not subject to all of the

independence and disclosure standards applicable to debt research reports prepared for retail

investors under U.S. FINRA Rule 2242. Barclays trades the securities covered in this report for its

own account and on a discretionary basis on behalf of certain clients. Such trading interests

may be contrary to the recommendations oered in this report.

Barclays Capital Inc. and/or one of its ailiates does and seeks to do business with companies

covered in its research reports. As a result, investors should be aware that the firm may have a

conflict of interest that could aect the objectivity of this report. Investors should consider this

report as only a single factor in making their investment decision.

* This individual is a member of the Product Management Group and is not a Research Analyst

All research referenced herein has been previously published. You can view the full reports,

including analyst certifications and other required disclosures, by clicking the hyperlinks in this

publication or by going to our Research portal on Barclays Live.

FOR ANALYST CERTIFICATION(S) PLEASE SEE PAGE 37.

FOR IMPORTANT EQUITY RESEARCH DISCLOSURES, PLEASE SEE PAGE 37.

FOR IMPORTANT FIXED INCOME RESEARCH DISCLOSURES, PLEASE SEE PAGE 38.

Global Portfolio Manager's Digest

Tricks of the Trade

We provide context and perspective on research across regions

and asset classes, this week highlighting our analysis of the

economic impacts of a potential global trade war; key

takeaways from the Barclays Global Financial Services

Conference; and our latest FX & EM Macro Strategy Quarterly.

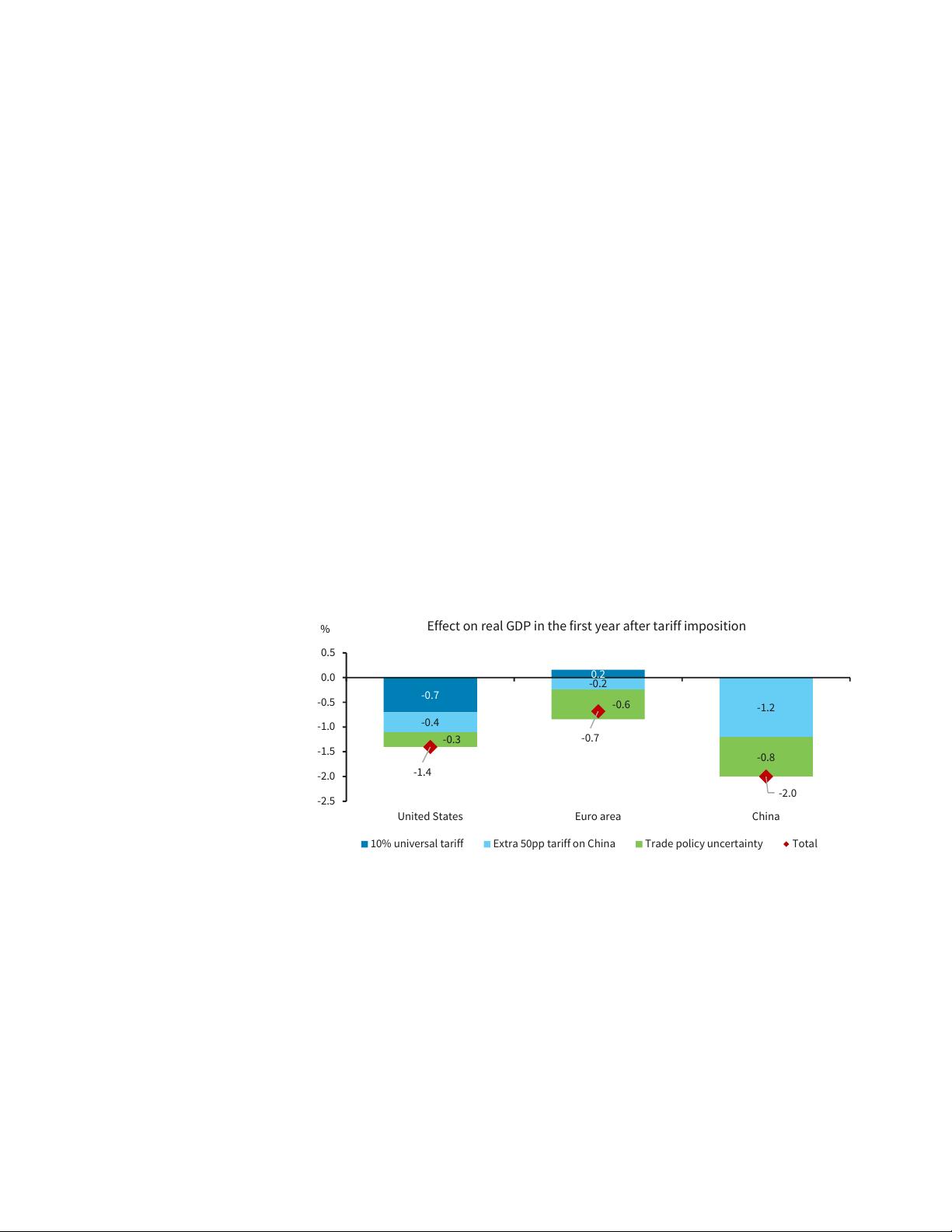

• Impacts of a Global Trade War: In our view, US tari increases to 60% and 10% on goods

imports from China and the RoW, respectively, as proposed by former President Trump,

would be a significant escalation of trade restrictions. Assuming symmetric retaliation from

all US trading partners, but accounting for dierent confidence eects, we estimate the eect

on the level of real GDP to be -2.0%, -1.4%, and -0.7% for China, the US, and the euro area

(EA), respectively, in the first 12 months. Inflation would rise in the short run, especially in the

US, by around 0.9pp, by our estimates, as the negative supply shock from higher taris

increases prices. US monetary policy would initially likely remain slightly tighter than in our

baseline of no tari increases, as inflation rises. But as activity starts weakening, amid trade

policy uncertainty and tighter financial conditions, we would expect the Fed to ease policy

rates more aggressively, possibly as much as 100bp. For the larger and more closed US

economy, the negative short-term eect would also likely more easily dissipate in the

following years. It could be more persistent for the more export-dependent China, EA, and

small open EM economies, especially if global trade tensions were to escalate beyond the

initial US tari increases.

• Global Financial Services Conference Takes: Despite loan growth remaining so and the

Fed widely expected to begin easing next week, most banks felt good about 2H24 net interest

income expectations as deposit trends show continued signs of stabilization. Still, investors

remain uncertain about how to think about 2025 net interest income. While fee income

should remain sound, some felt near-term trading and investment banking results could be a

little soer than expected; investment banking fees, however, should continue to rebound

Cross Asset Research

15 September 2024

FOCUS

Equity Product Management Group

Terence Malone

*

+ 1 212 526 7578

terence.malone@barclays.com

BCI, US

Rob Bate

*

+44 (0)20 7773 3576

rob.bate@barclays.com

Barclays, UK

FICC Product Management Group

Ben McLannahan

*

+44 (0)20 3134 9586

ben.mclannahan@barclays.com

Barclays, UK

Jennifer Cardilli

*

+1 212 526 8351

jennifer.cardilli@barclays.com

BCI, US

Completed: 13-Sep-24, 21:41 GMT Released: 15-Sep-24, 13:00 GMT Restricted - External

剩余43页未读,继续阅读

资源评论

soso1968

- 粉丝: 3330

- 资源: 1万+

最新资源

- 风光柴储直流微网(并离网均可) 含: 永磁风机+整流 光伏发+boost+mppt 柴油机380V+整流 储能双向DCDC稳压直流母线800V 离网逆变器VF控制 0.85s时刻负荷突增20kW 波

- 西门子1200PLC大型项程序,生产线生产案例,包含气缸,通讯,机械手,模拟量等,各种FB块,可用来参考和学习 若能学懂这个,大型程序基本能独当一面 plc博图15以及以上,威纶通触摸屏,共计控制2

- GWO-LSTM多变量回归预测,灰狼算法优化长短期记忆网络的回归预测(Matlab) 1.data为数据集 2.MainGWO-LSTMNN.m为程序主文件,其他为函数文件无需运行 3.命令窗口输

- Abb万能密钥,带涂胶工艺包,选项快捷方便,可做工作站-涂胶

- 三菱PLC转盘机程序 三菱plc学习借鉴程序案例,没触摸屏 此程序已经实际设备上批量应用,程序成熟可靠,借鉴价值高,程序有注释,用的三菱fx3u系列plc 是入门级三菱PLC电气爱好从业人员借鉴和参

- 储能系统双向DCDC变器 双闭环控制 蓄电池充放电仿真模型有buck模式和boost模式,依靠蓄电池充放电维持直流母线电压平衡

- 软件使用:Matlab Simulink 适用场景:采用模块化建模方法,搭建14自由度整车模型,作为整车平台适用于多种工况场景 产品simulink源码包含如下模块: 工况: 阶跃工况 包含模块

- 无感FOC 滑膜观测器 算法采用滑膜观测器,启动采用Vf,全开源c代码,全开源,启动顺滑,提供原理图、smo推导过程及仿真模型

- 50KW储能逆变器变流器结构设计图源文件 SOLID WORKS工具格式 是基于高效、可靠、免维护的理念,开发的光伏储能产品,为家庭和工业不间断供电提供了灵活多样及安全可靠的系统解决方案 离并网一体

- Simulink仿真:基于DC DC双向变器的多电池主动均衡技术 关键词:锂电池;不一致性;模糊控制理论;DC DC双向主动均衡;荷电状态(SOC);均值-差值法 参考文献:基于DC DC双向变器的多

- 西门子1200立库机器人码垛机伺服视觉AGV程序 包括2台西门子PLC1215程序和2台西门子触摸屏TP700程序 PLC与工业相机视觉定位及机器人使用Modbus TCP通讯 PLC和码垛机Modb

- 声子晶体声表面波-等离子激元效应仿真案例文献复现Surface acoustic waves-localized plasmon interaction in pillared phononic cr

- 三菱FX3U PLC FX3U-485BD自由口跟23个上海众晨Z2000变频器通讯,读运行电流,写入设定频率;读RKC RD700温控表温度值,读电能表正向有功功率;程序简洁明了,注释详细 单PL

- 水处理程序,中文注释,内容齐全,风机,阀,传感器,PID样样齐全 汽车厂大程序,有很大参考借鉴意义值得你拥有

- OMRON CP1H PLC脉冲控制三轴伺服, 码垛机,实际项目,程序结构清析,有完整的注释,重复功能做成FB功能块,在其它项目可以导出直接用,MCGS触摸屏程序,有电气CAD图纸

- 新能源电池焊接1200程序 西门子PLC做的电池焊接程序,电池包里面有n*m行列个电池,主要功能: 1.每个电池的焊点坐标能够独立调整 2.每个电池的焊接能量可独立选择 3.任意一个或者多个电池可以随

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈