│

│

Powered by the

EFA Platform

Opportunities along with challenges

■ HK-listed TMT names, in general, underperformed the market in 2018 and in China’s

TMT sector, non-hardware outperformed hardware.

■ We still prefer the non-hardware segment, as investment themes such as

increasing adoption of cloud computing and AI remain intact. The

segments are likely to outperform the toC segment.

■ The hardware segment was dragged down by handset components, since the

market is maturing. 5G and related names will remain the

focus of the market despite

their outperformance in 2H 2018. 5G-

related applications such as IoV, IoT, IIOT and

Smart City will be investment themes in the medium term.

■ Any share price weakness around 2018 results announcements

in Mar 2019 will offer

a good buying opportunity.

China TMT underperformed the market in 2018

In terms of share

-price performance, on average, the HK-listed TMT non-

hardware names

outperformed the

hardware names, but both segments underperformed the overall

market

in 2018. On average, share prices in the TM

T non-hardware sector dropped 26.1

018 vs. -29.4% for the hardware sector, -13.6% for the HSI, -13.5

-20.9% for MSCI China. The TMT non-

hardware sector performance was

dragged down by the weak share price performance of sub

-

ertainment and e-commerce, while IT services and media outperformed.

was dragged down by handset component names

, given weaker-than-expected shipment volume,

bout Apple’s order cut and concerns about peaking of the semiconductor cycle. In 2018

the trade dispute between China and US, RMB depreci

ation, slower

economic growth and weaker

-than-

expected downstream demand also put pressure on

the

China TMT sector. We see divergence in the valuation of HK-listed TMT names

, with

those under major investment themes trading at

a much higher valuation, while

concerns about the growth outlook have been de-rated. Names with

s and high trading liquidity have performed better than their smaller cap peers.

fer non-hardware over hardware

the increasing macro uncertainties, we believe that investors will remain short-

term

focused and that the share price performance of the HK

-

listed TMT names in particular

might remain volatile in 1H 2019

, especially in

Q1 2019, given the seasonality impact and

the

lack of near-

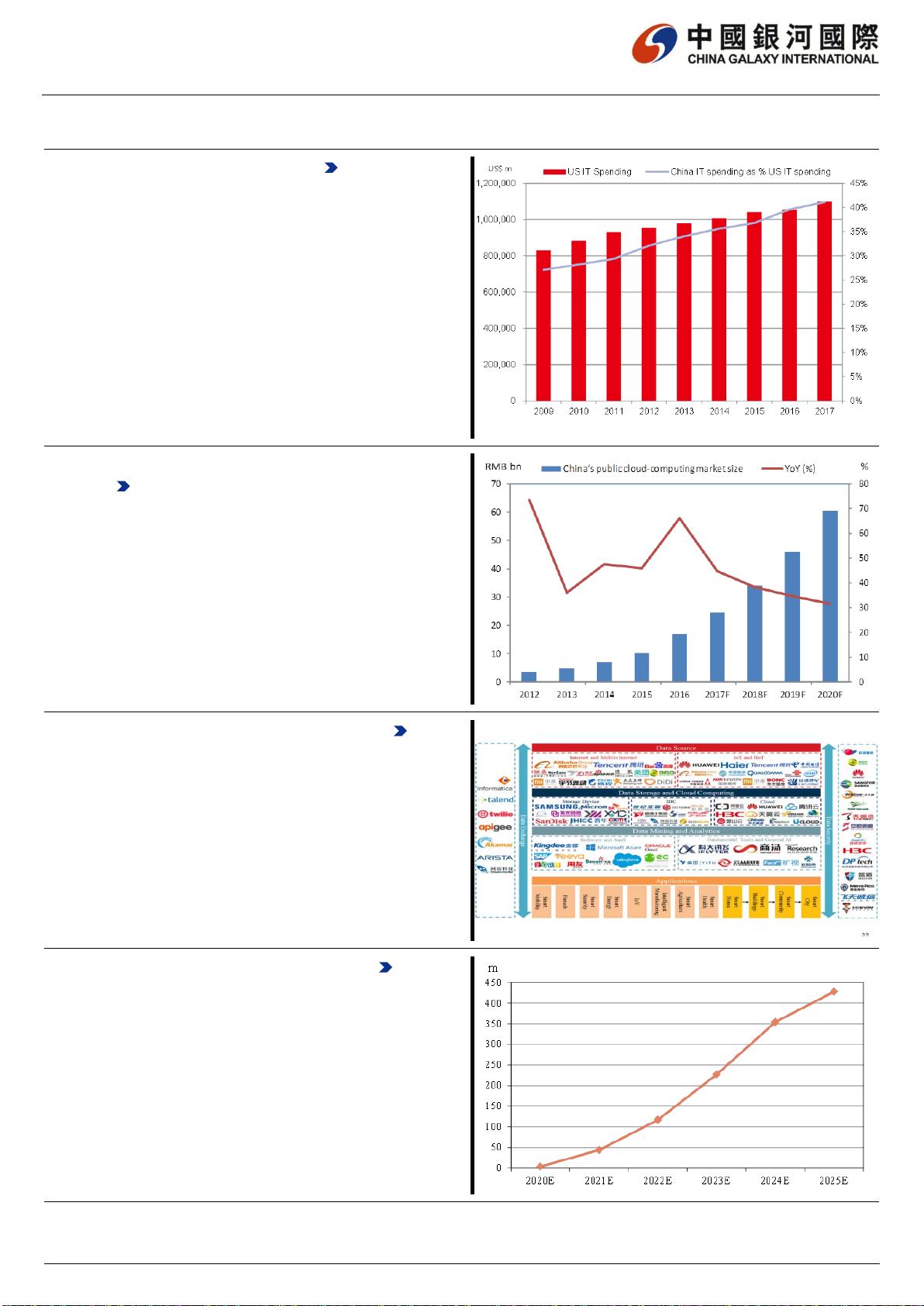

term catalysts. However, industry development, including higher IT

spending by corporates and government, continuing cloud migration,

the adoption of 5G

-

related technologies and applications

,

and supportive government policies, remains intact.

We be

lieve that early Q2 2019 will be a good entry point for the leading TMT names,

a realization of share price catalysts, such as the

relaxation of government

regulations on

other verticals in China’s internet sector, the 5G timetable and road

map

release by telecom services providers

, and more concrete policies

to boost economic

growth.

We still expect our preferred names to report decent growth in 2019 and 2020, given

favourable industry development trends. In general, we prefer the TMT non

-

hardware

sector over the hardware sector, as the former will be less impacted by the mature

hardware market

, and leading names will gain market share. In the non-

hardware TMT

sector, we believe that IT services, online video, AI development, IT services

, o

, and 5G-

related applications are the hot spots, and that the leading players in

mobile games will continue to gain market share. In the hardware segment, the leading

players with exposure to high

-growth areas, such as 5G, optical sensors, IoV, IoT,

the Industrial Internet,

will continue to benefit from industry development. However,

TMT hardware names in segments with concerns about

the

growth outlook will continue to

underperform.

China Tower

BUY, TP HK$1.81, HK$1.48 close

The Company is an early 5G CAPEX cycle

name with limited exposure

to overseas

markets and faces less macro risk.

Inspur International

BUY, TP HK$4.50, HK$3.39 close

Inspur is an under-appreciated IT services

name, which will benefit from increasing IT

spending. The Company is trading at a lower

valuation than its peers.

Tencent

BUY, TP HK$341.87, HK$314.00 close

The resumption of online game approval is

expected to boost sentiment on sector

companies, including Tencent. Other business,

such as online advertising and online

entertainment, will support medium to long-

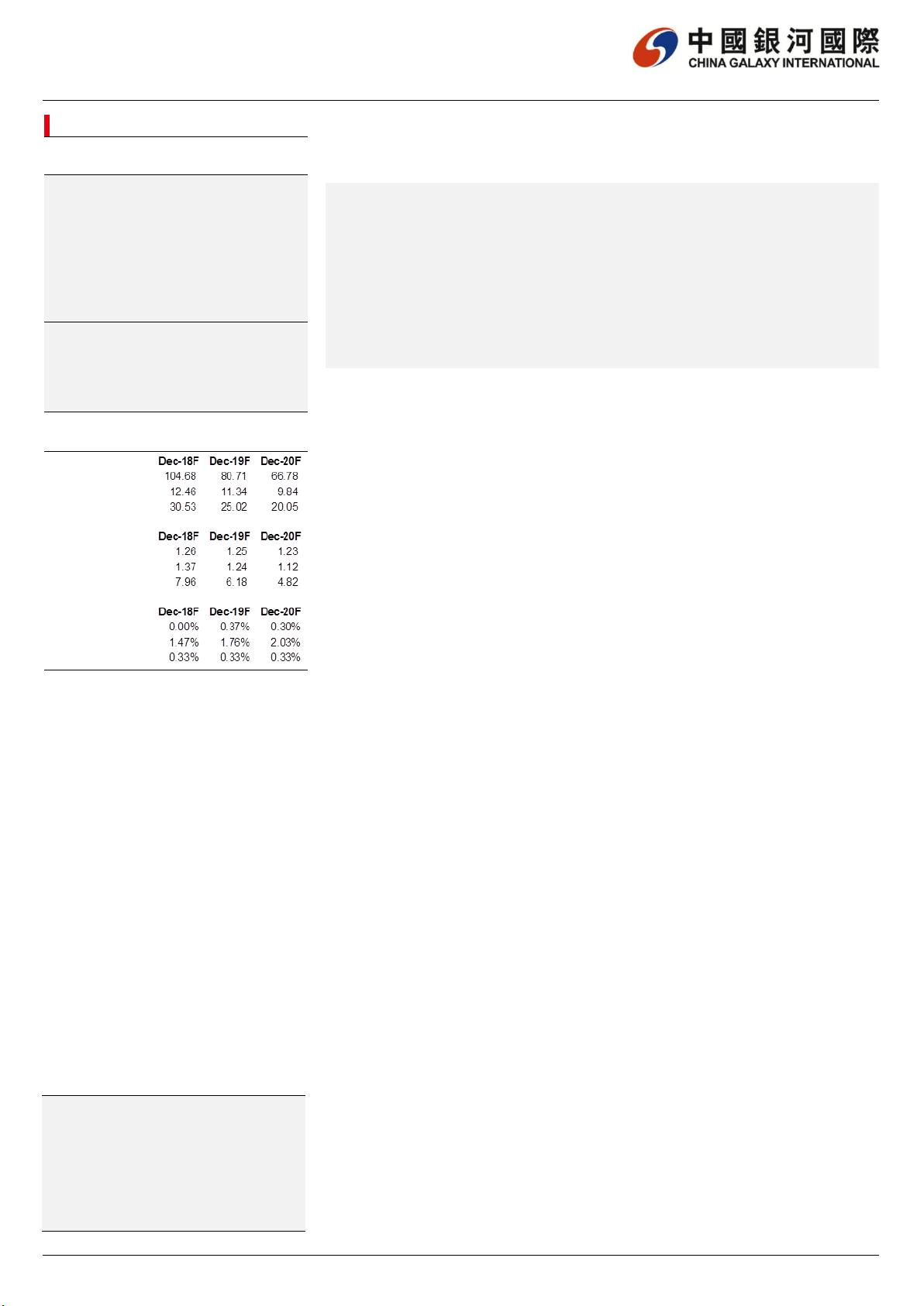

Summary valuation metrics

E markpo@chinastock.com.hk

E cmwong@chinastock.com.hk

P/E (x) Dec-18F Dec-19F Dec-20F

China Tower 104.68 80.71 66.78

Inspur International 12.46 11.34 9.84

Tencent 30.53 25.02 20.05

P/BV (x) Dec-18F Dec-19F Dec-20F

China Tower 1.26 1.25 1.23

Inspur International 1.37 1.24 1.12

Tencent 7.96 6.18 4.82

Dividend Yield Dec-18F Dec-19F Dec-20F

China Tower 0.00% 0.37% 0.30%

Inspur International 1.47% 1.76% 2.03%

Tencent 0.33% 0.33% 0.33%