瑞信-亚太地区-公用事业行业-澳大利亚公用事业:拿回权力-72-32页.pdf

需积分: 0 142 浏览量

2023-07-26

12:00:44

上传

评论

收藏 1.26MB PDF 举报

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST

CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit

Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware

that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report

as only a single factor in making their investment decision.

2 July 2019

Asia Pacific/Australia

Equity Research

Multi Utilities

Australian Utilities

SECTOR REVIEW

Research Analysts

Peter Wilson

61 2 8205 4107

Chloe Lim

61 2 8205 4739

Take the power back; Upgrade ORG/AGL

We upgrade the ratings for both AGL and Origin Energy. Our prior premise

was that forecast decreases in wholesale prices would be passed-through to

customers and earnings FY19-22F. However, wholesale electricity prices

remain high, and July retail repricing introduces doubt over the pass-through.

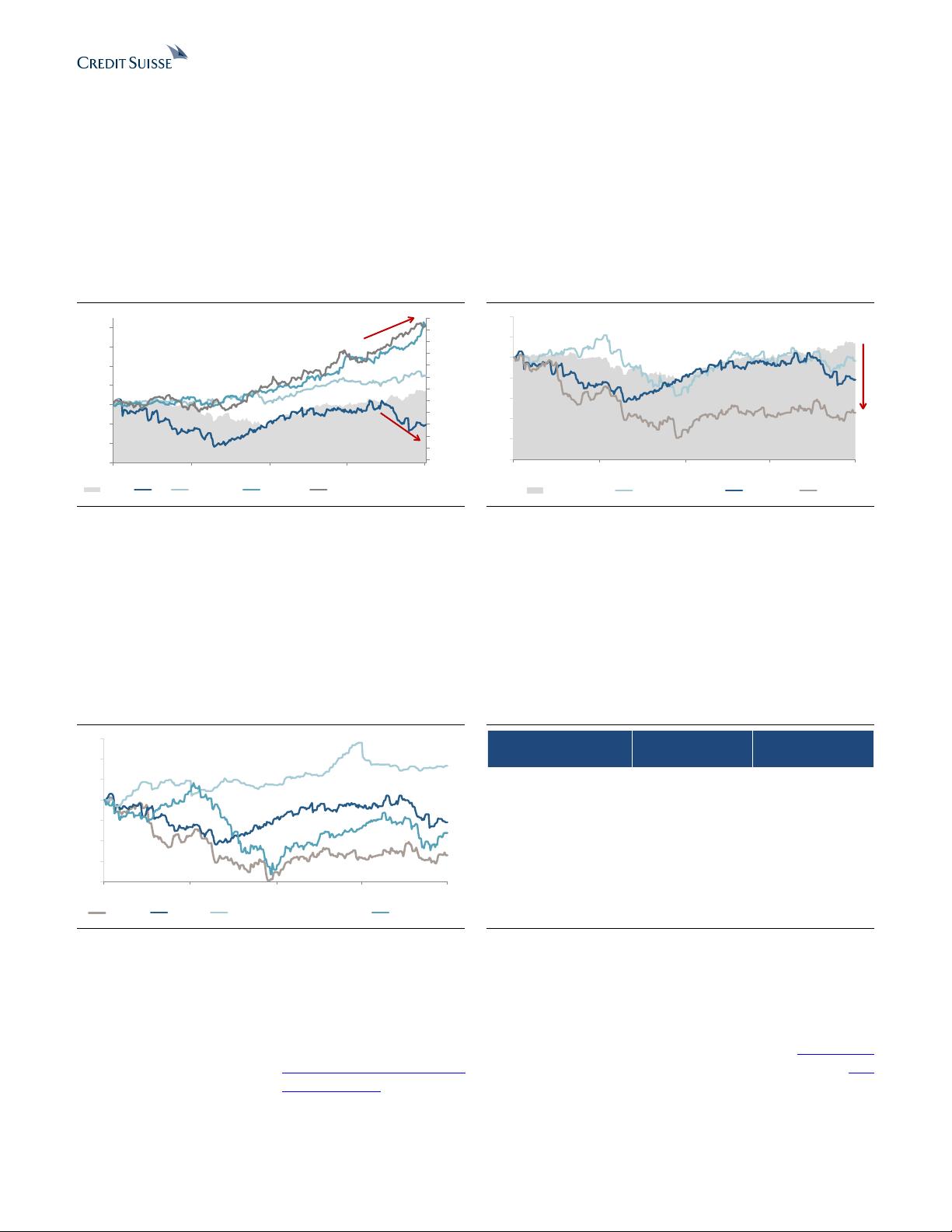

■ Upgrade AGL and Origin: both have underperformed the market,

peers, and key earnings input. Whilst we continue to see downside to

electricity prices from renewables and government intervention, a 12M rally

shows a subdued impact so far. AGL and Origin have underperformed this

key earnings input, underperformed oil (ORG), and underperformed the

ASX200 even as bond yields have pushed peer valuations higher.

■ July retail resets show repricing power retained under DMO,

introduces doubt on pass-through of price downside. The first reset

coinciding with the introduction of the DMO illustrates that retailers have

retained the freedom to reprice their back book, introducing doubt that

wholesale price falls will be passed through in full. For existing customers

on discounts, we estimate that AGL/ORG have retained A$30-55mn in

costs; in ORG's case, it has redirected these savings to other customers.

Further, best offers from the large retailers are now higher than in Apr/May,

indicating an easing of competition, although we expect this to be volatile.

■ Risks. A fall in wholesale electricity futures remains the largest risk, with

soft spot LNG prices and government intervention the contributing factors.

■ Upgrade Origin Energy (ORG.AX) to OUTPERFORM, target price

A$8.50/sh (from A$7.55/sh). Origin has underperformed AGL and E&P

peers; it has a superior earnings, FCF and dividend profile to AGL; and we

expect the FY19 results to be a positive catalyst, with a strong Energy

Markets EBITDA and an update on the ongoing dividend policy.

■ Upgrade AGL Energy (AGL.AX) to NEUTRAL, target price A$19.20/sh

(from A$18.30/sh). Upgrade based on relative underperformance, with

resilient electricity futures and July retail pricing resets diminishing

wholesale price downside.

剩余31页未读,继续阅读

资源评论