麦格理-美股-消费品行业-消费之王:堡垒坚固-318-23页.pdf

需积分: 0 32 浏览量

2023-07-26

11:55:52

上传

评论

收藏 681KB PDF 举报

18 March 2019 North America/United States/Canada

Sales and Trading personnel at Macquarie are not independent and, therefore, the information herein may be subject to certain conflicts of

interest, and may have been shared with other parties prior to publication. Note: To the extent Macquarie Research is referenced, it is

identified as such and the associated disclaimers are included in the published research report. Please refer to the important disclosures

www.macquarie.com/salesandtradingdisclaimer.

ECONOMICS

Source: Federal Reserve, Macquarie Macro Strategy, March 2019

Source: Federal Reserve, Macquarie Macro Strategy, March 2019

Source: BLS, Bloomberg, Macquarie Macro Strategy, November 2018

Economists

Macquarie Capital Markets Canada Ltd.

David Doyle, CFA +1 416 848 3663

david.doyle@macquarie.com

Neil Shankar +1 416 607 5055

neil.shankar@macquarie.com

Macquarie Securities (Australia) Limited

Ric Deverell +61 2 8232 4307

ric.deverell@macquarie.com

This publication has been prepared by Sales and Trading personnel at Macquarie

and is not a product of the Macquarie Research Department.

King Consumer

The Fortress stands strong

Powerful fundamentals underpin the US Consumer

As the economic expansion approaches ten years, its engine, the US consumer,

appears as resilient as ever. Spending has risen over $600 billion over the past

four quarters and ~$4.4 trillion over the past decade.

Consumer confidence is strong and unemployment is near multi-decade lows and

likely to fall further. While recent spending data have shown some softness, we

do not believe this is representative of consumer health. Real income growth is

robust supported by favourable trends in jobs growth and real wage growth.

These anchor our consumer outlook and view of still solid growth in the US.

2019 is likely to be a banner year for real wage growth. Nominal wages are

pushing higher even as inflation stays contained. Strength in real wage growth is

not a recent phenomenon. Despite what some naysayers may suggest, the past

ten years have been amongst the strongest in history.

Real wage growth has not been confined to those with higher incomes. Recently,

wage gains have been strongest in the lowest paying sub-industries. Moreover,

real median household income, after trending sideways for nearly three decades

(through 2014), has risen ~13% over the past 4 years.

The US consumer has deleveraged and is as resilient as ever

Deleveraging has put the consumer in a favourable position. There are few signs

of froth or concern – delinquencies and bankruptcies remain low. Several factors

suggest the consumer is well positioned to withstand potential shocks.

1) Household debt service low. As a share of disposable income it has never

been lower, suggesting ample capacity to absorb higher interest rates.

2) Gasoline expense low. As a share of disposable income, this stands at just

~2.2%, near the lowest level in 70 years and suggesting the consumer is well

positioned to absorb any potential increases in energy prices.

3) Secular rise in services reduces spending volatility. Spending on services

comprises ~70% of total personal consumption and has been rising. As it is

less volatile than goods spending, its rising share adds to resiliency.

4) Retirements and an aging population. As the share of population over 65

rises so has the share of income generated from sources such as defined

benefit pension plans and social security. These are more stable than

employment income, providing an added source of consumption stability.

5) Low labor force growth. Due to retirements, this should be much lower than

in prior decades. The result should be that only ~70K jobs per month will be

needed to prevent the unemployment rate from rising, suggesting the labor

market can withstand slowing jobs growth.

Key themes likely to impact consumption trends ahead

Consumption patterns are shifting. The fastest growth categories over the past

year are concentrated in services and include spectator sports, air transportation,

and internet access. Categories in decline are skewed more towards goods.

We analyze three key themes likely to impact spending patterns ahead: e-

commerce, the wealth effect, and financial pressures on the millennial generation.

52,000

54,000

56,000

58,000

60,000

62,000

64,000

66,000

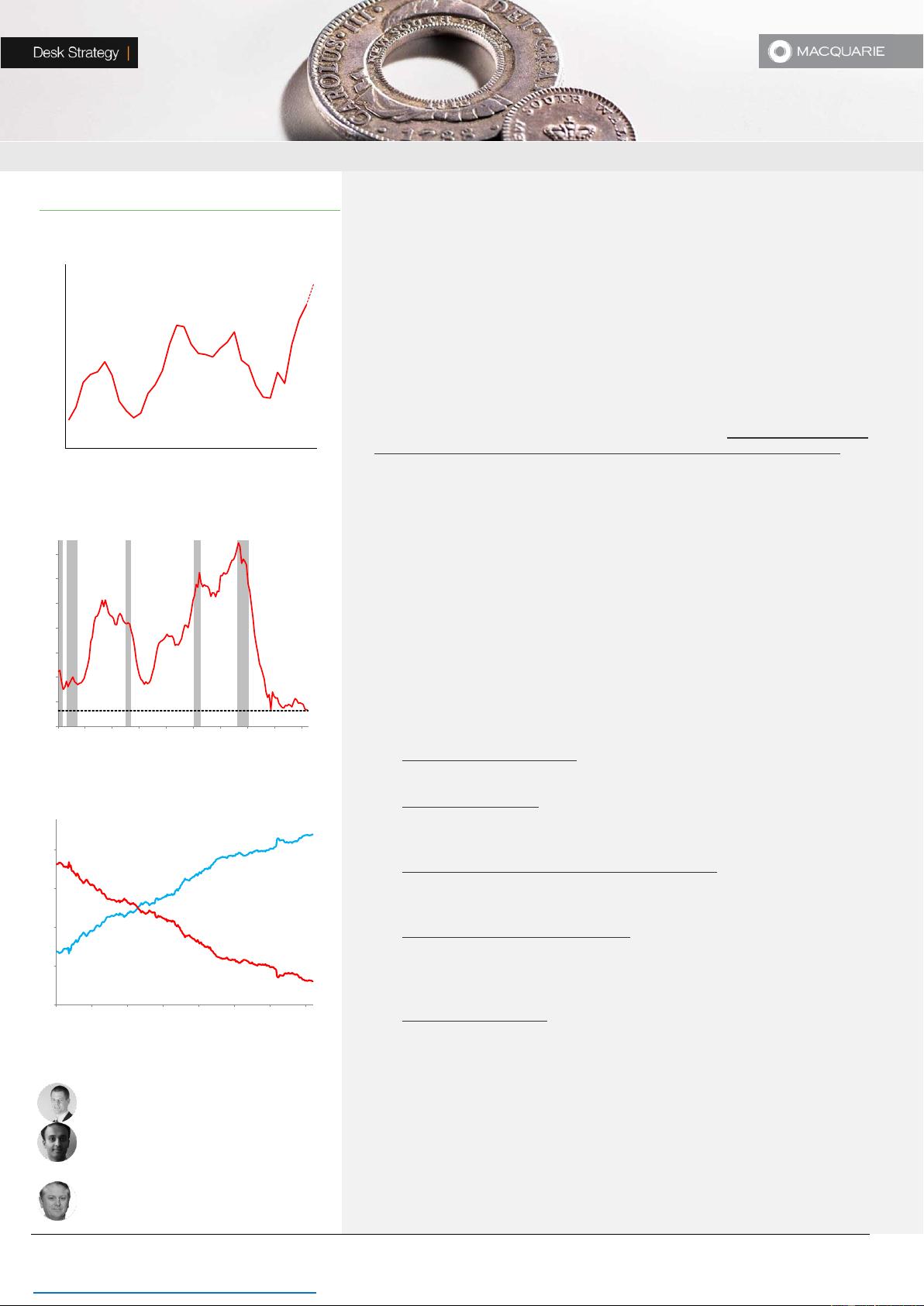

1984 1988 1992 1996 2000 2004 2008 2012 2016

Real median HH income (2018 $s)

2018

est.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

9.5

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

1980 1984 1988 1992 1996 2000 2005 2009 2013 2017

US HH debt service payments as a % of disposable personal income

3Q18 level = 9.8%

69.0%

31.0%

25%

35%

45%

55%

65%

75%

1947 1957 1967 1977 1987 1997 2007 2017

Share of personal consumption expenditures

services

goods

剩余22页未读,继续阅读

资源评论