汇丰银行-全球-零售行业-食品零售的生命阶段:零售经济学-48-48页.pdf

需积分: 0 97 浏览量

2023-07-27

15:03:43

上传

评论

收藏 1.05MB PDF 举报

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Bank plc

View HSBC Global Research at:

https://www.research.hsbc.com

Voting opens 11

th

March – 12

th

April

If you value our serviceand insight, please vote

Click here to vote

Vote in Extel 2019

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE'S REPUBLIC OF CHINA (THE "PRC")

(EXCLUDING SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

Food retail has various life stages and these drive industry

structure & strategies. We examine these in detail inside.

Profits, returns & cash flow evolve through different life

stages. The winning strategy depends on the life stage.

Understanding the relevant life stage for each country helps

identify winning strategies, retailers and investments.

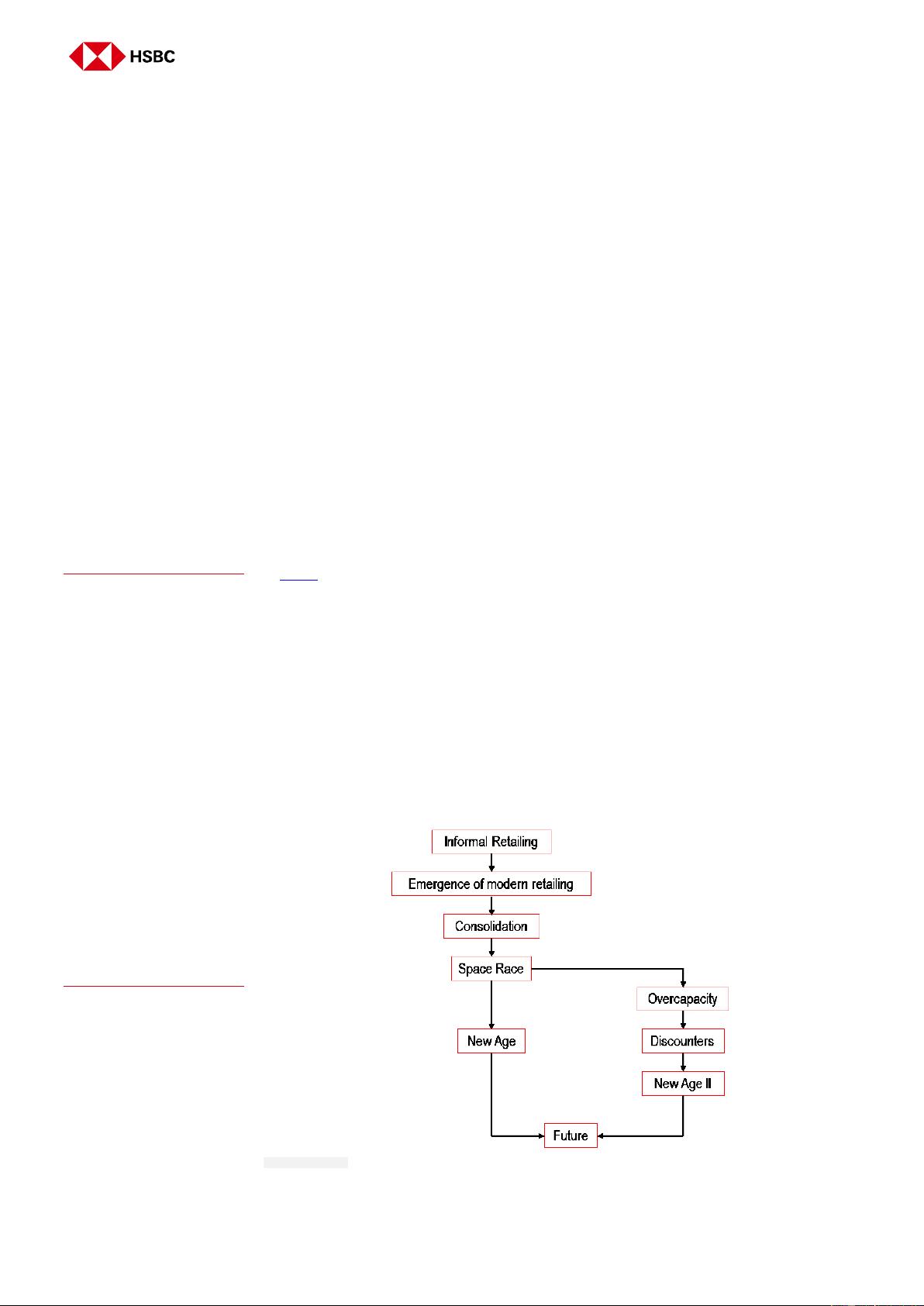

The Life Stages of Food Retail. This is the second theme in our series on Retail

Economics. In this issue we study the life stages of food retail, from the birth of organised

retail through to maturity, the discount era and the new age. As with our previous theme,

the findings transcend time and geography and we believe the life stages highlight the

natural evolution of the 4 principles of food retail economics. We examined these

principles in detail in Global Retail Digest: Issue 1. As a reminder they are:

Demand is inelastic at the industry level

Demand is highly elastic at the company level

Retailers have high operational gearing

Industry has high economies of scale (relative to profits)

A crunch time is when the industry passes through the Space Race. If expansion

continues unabated, we end up in a capital war with overcapacity as the UK suffered

c2010. This leads to an inevitable fall in profits and a collapse in returns. It can expedite

discounter entry. On the other hand if the industry is well managed with a strong leader,

these stages are not inevitable. Within the report we look at different geographies and

highlight which life stage each is at. Lessons learnt in one country can be applied to

others. We also remind readers of the Prisoner’s Dilemma which explains how rational

decisions by individual firms can lead to irrational outcomes for the collective.

Key Reports: The Global Retail Team has published a large number of important reports

recently, several of which are highly applicable to readers in each region. See page 28 for

details, but in particular we would highlight:

Lease accounting: IFRS 16: the biggest changes in over 30 years, 19-Feb

Poland food retail: Proximity formats working for Dino, 21-Mar

LatAm food retail: Protecting groceries from being clicked away, Mar-19

The curious case of disappearing CEOs, 04-Mar

Emerging Market-Developed Market Bridge. Also inside is our Global Retail Diary and

Global Comp Sheet. We also include important ESG and other reports that have

important implications for retail.

Extel is very important to us this year. If you think this report is helpful, please show

your appreciation by voting for HSBC Retail. The link is here.

8 April 2019

David McCarthy*

Global Head of Consumer Retail Research

HSBC Bank plc

david1.mccarthy@hsbcib.com

+44 20 7992 1326

Ravi Jain

Senior Analyst, LatAm Retail

HSBC Securities (USA) Inc.

ravijain@us.hsbc.com

+1 212 525 3442

Jeanine Womersley*, CFA

Analyst, South African Retail

HSBC Securities (South Africa) (Pty) Ltd

jeanine.womersley@za.hsbc.com

+27 21 795 0779

Nigel Kiernan*

Director, ASEAN Consumer Analyst

The Hongkong and Shanghai Banking Corporation

Limited, Singapore Branch

nigel.kiernan@hsbc.com.sg

+65 6658 0809

Bulent Yurdagul*

Head of EEMEA Consumer Research

HSBC Yatirim Menkul Degerler A.S.

bulentyurdagul@hsbc.com.tr

+90 212 376 46 12

Karen Choi*

Head of Consumer and Retail Research, Asia Pacific

The Hongkong and Shanghai Banking Corporation

Limited, Seoul Securities Branch

karen.choi@kr.hsbc.com

+82 2 3706 8781

Paul Rossington*

Analyst

HSBC Bank plc

paul.rossington@hsbcib.com

+44 20 7991 6734

Andrew Porteous*, CFA

European Retail Analyst

HSBC Bank plc

andrew.porteous@hsbc.com

+44 20 7992 4647

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is

not registered/ qualified pursuant to FINRA regulations

The Life Stages of Food Retail

Equities

Consumer Retail

Global

Global Retail Digest 2: Retail Economics Part II

剩余47页未读,继续阅读

资源评论