瑞信-亚太地区-银行业-新加坡银行业:运行安全-530-39页.pdf

需积分: 0 200 浏览量

2023-07-26

12:04:33

上传

评论

收藏 1.2MB PDF 举报

DISCLOSURE APPENDIX AT THE BACK OF THIS REPORT CONTAINS IMPORTANT DISCLOSURES, ANALYST

CERTIFICATIONS, LEGAL ENTITY DISCLOSURE AND THE STATUS OF NON-US ANALYSTS. US Disclosure: Credit

Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware

that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report

as only a single factor in making their investment decision.

30 May 2019

Asia Pacific/Singapore

Equity Research

Banks

Singapore Banks Sector

ASSUMING COVERAGE

Research Analysts

Nicholas Teh

65 6212 3026

nicholas.teh@credit-suisse.com

Kylie Wan

65 6212 3004

kylie.wan@credit-suisse.com

Flight to safety

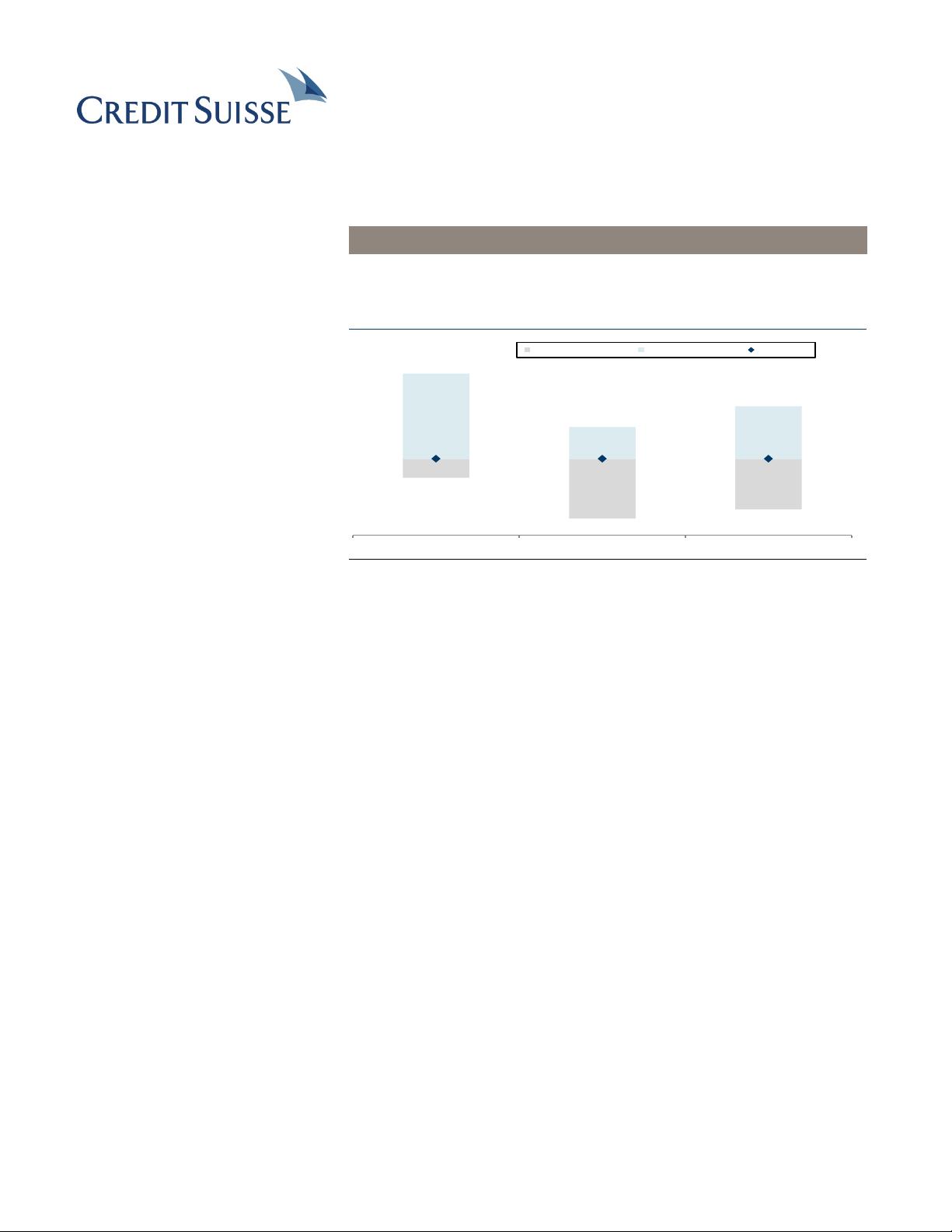

Figure 1: Risk-reward most favourable for UOB

S$24.49

S$11.37

S$23.52

UOB OCBC DBS

Downside to "grey sky" Upside to "base case" Current price

Base case = S$29.7

(+22% upside)

Base case = S$11.9

(+9% upside)

Base case = S$28.4

(+14% upside)

Grey sky = S$23.1

(5% downside)

Grey sky = S$9.2

(16% downside)

Grey sky = S$21.7

(13% downside)

Source: Company data, Credit Suisse estimates

■ Decent risk-reward. With slowing economic growth and uncertainty over

interest rate direction, our base case assumes flat-to-declining ROEs for

Singapore banks in 2019-21E. In our view, DBS and UOB have the most

levers to drive higher NIM from 1Q19 levels, with key risks being higher

loan competition mitigating pass-through of higher rates and potential US

rate cuts. By our estimates, a 50 bp reduction in the US rate would affect

DBS the most (-7.5% to net profit), then OCBC (-5.7%), and UOB (-4.7%).

Our grey-sky analysis suggests that potential earnings cuts are partially

priced in, particularly for UOB, where there might be just 5% further

downside should there be no loan growth, flat NIM, and higher credit cost.

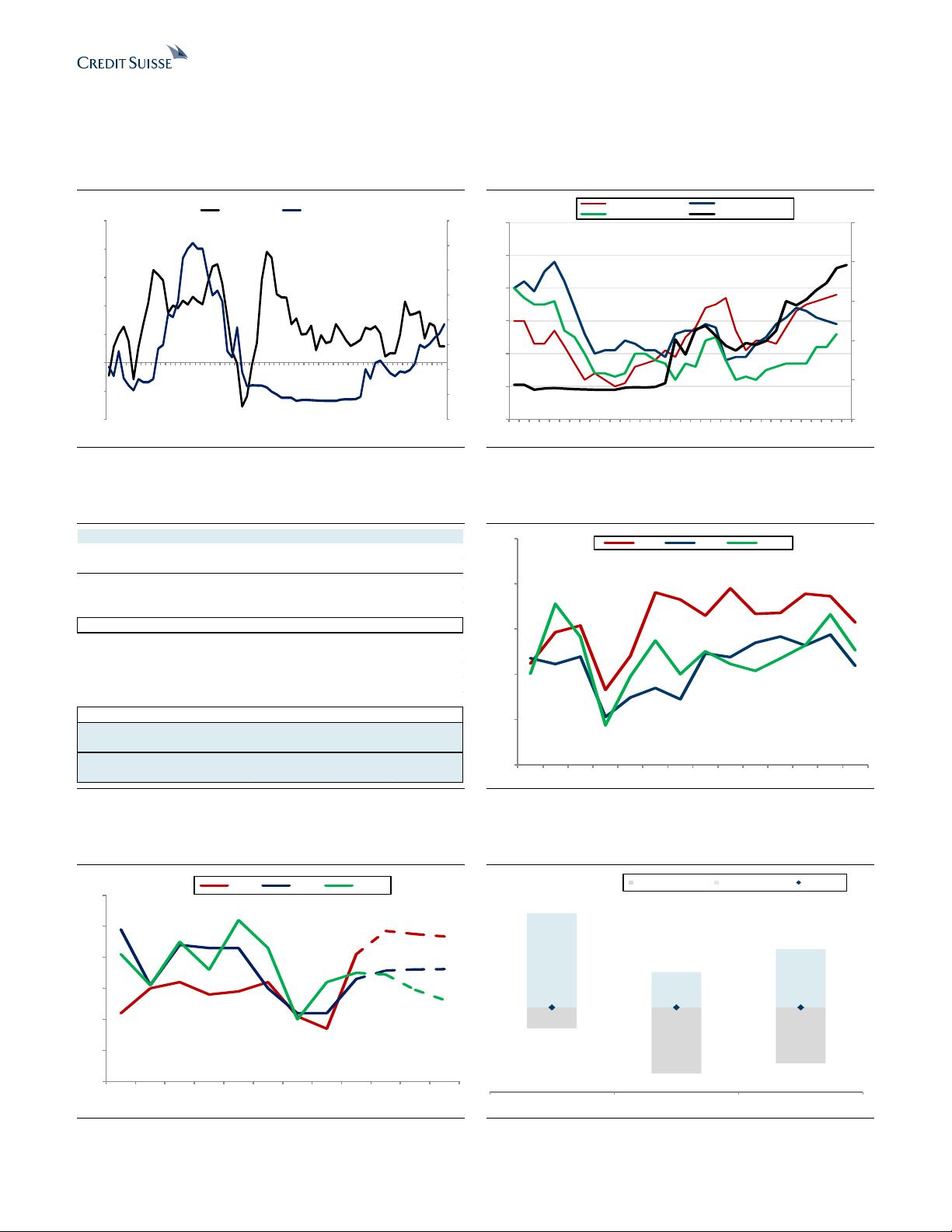

■ UOB should have the least volatile NOII. Capital-market-related non-

interest income (NOII) is the lowest for UOB (16% vs 18-21% for

DBS/OCBC in 2018)—hence UOB should be less susceptible to swings in

market sentiment. Trading income is the most volatile component of NOII.

While trading income is the largest contributor to DBS' earnings, it exhibits

most volatility for OCBC.

■ Switch to UOB. We assume coverage of Singapore banks. UOB

(OUTPERFORM, TP S$29.70) is our top pick, as it has the most stable

earnings base and least volatile NOII, and offers the best risk-reward in

different scenarios. We see DBS (OUTPERFORM, TP S$28.40) providing

the most certainty on dividends (4.8% yield), with its long-term digital

strategy intact. We expect OCBC's (NEUTRAL, TP S$11.85) ROE to see a

declining trend moving forward on its build-up of excess capital to address

volatility in the macro environment and potential acquisition opportunities.

剩余38页未读,继续阅读

资源评论