巴黎银行-全球-宏观策略-从资产价格推断经济周期(更新)-0705-25页.pdf

需积分: 0 82 浏览量

2023-07-26

11:48:48

上传

评论

收藏 1.36MB PDF 举报

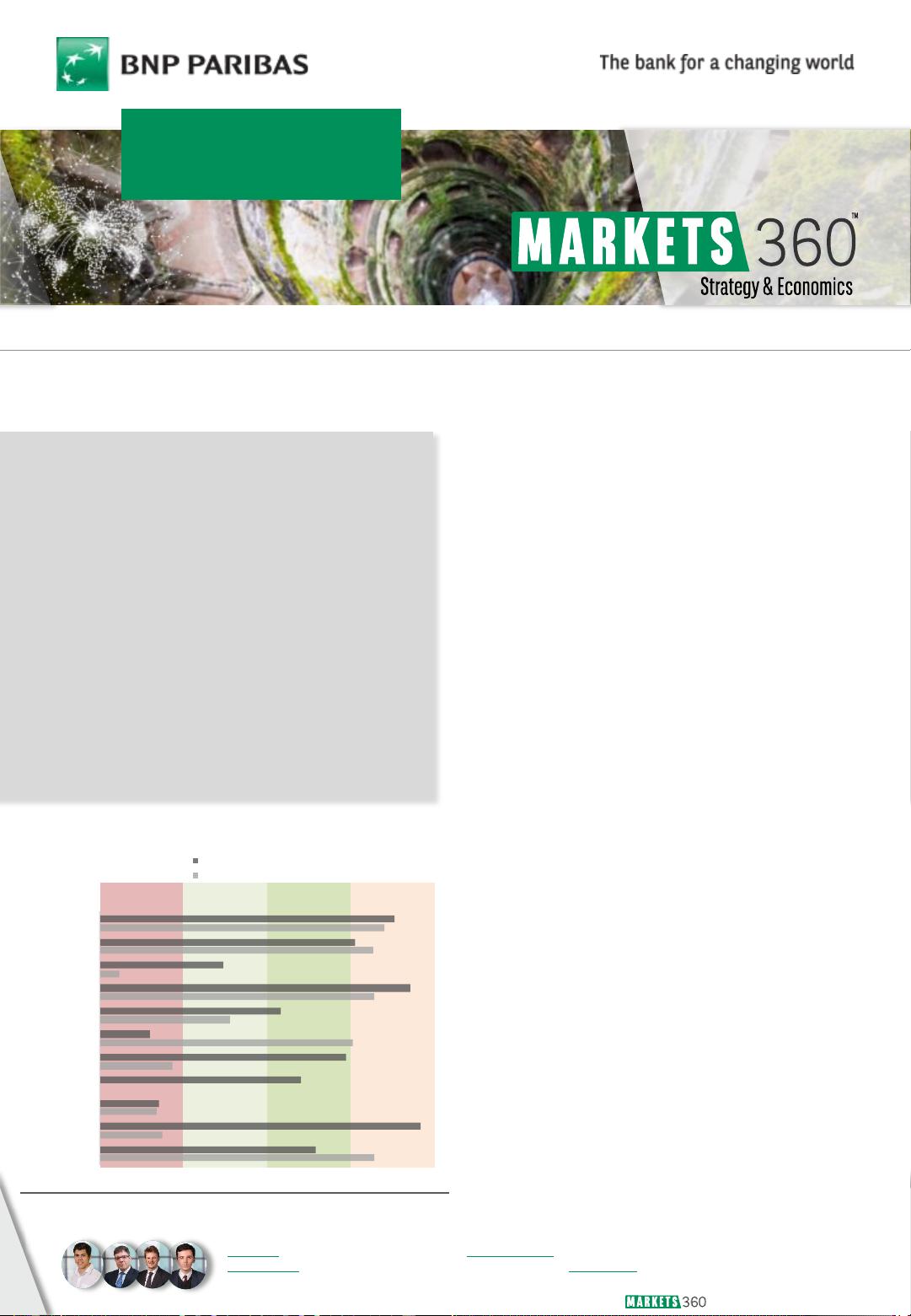

P

oland

Turkey

South Korea

Indonesia

South Africa

Mexico

Brazil

Japan

China

Eurozone

US

Market prices based index

Economic data based index

B- E

arly stage

C- Mid stage

D- Late stage

A- Grow th

< potential

Sources: Bloomberg LLP, BNP Paribas

|

DEEP DIVE 05/07/2019 1

L

uca

M

aia

,

EM/FX&IR Latin America Strategy |

G

abriel

Ge

rsztein

, G

lobal Head of EM Strategy | Banco BNP Paribas Brasil |

Michael

S

neyd, Head of Macro Quantitative and Derivatives Strategy | Stefan

Ub

ovic, Senior Macro Quantitative Strategist |

B

NP Paribas London Branch

D

EEP DIVE | GLOBAL

5 J

uly 2019

I

nferring economic cycles from asset prices; Update

KEY MESSAGES

Bo

th our market-based indicator and an equivalent index

based on published macroeconomic data point to the US,

Eurozone and Japan having entered the late stage of the

economic cycle.

China already seems to have undergone a deceleration and is

in the early stage of a cycle. Markets are ahead of data for

China, suggesting that investors see recent stabilization

as a turning point.

In EMs, Brazil, South Africa and Indonesia are in the

middle stage of the cycle, with prices indicating expansion

in those countries.

Markets look to be ahead of the data in Brazil and Mexico,

but behind the data in South Africa, Turkey and Poland.

See appendix for a technical description of the approach.

P

lease refer to important information at

the end of this report

EM

STRATEGY | MACRO QUANT & DERIVATIVES

Our approach: Economic cycles – also known as

business or trade cycles – refer to the economy-wide

fluctuations in production, trade and general activity.

From a conceptual point of view, a cycle is often

defined by the upward or downward long-term trend

of real GDP and other macro indicators, such as

industrial production, income, employment or sales.

The conventional approach is to gather and sort out

economic variables to determine the phase of the

cycle. But what if data could be modelled to infer the

phase of the cycles from market prices?

We have designed a quantitative tool that uses the

performance of selected financial assets to extract

the implied stage of the economic cycle.

Unlike the standard approach to economic cycles, we

have used only asset prices to measure the stage,

pace and duration (actual and projected) of the

current cycle for each country.

Since our goal was to extract market perception on

where selected markets are in terms of economic

cycles, we used only mathematical methods to define

the current cycle instead of using regressing

variables or making assumptions.

We also compared our market-based index with an

index we built using a similar method based on

published macroeconomic data.

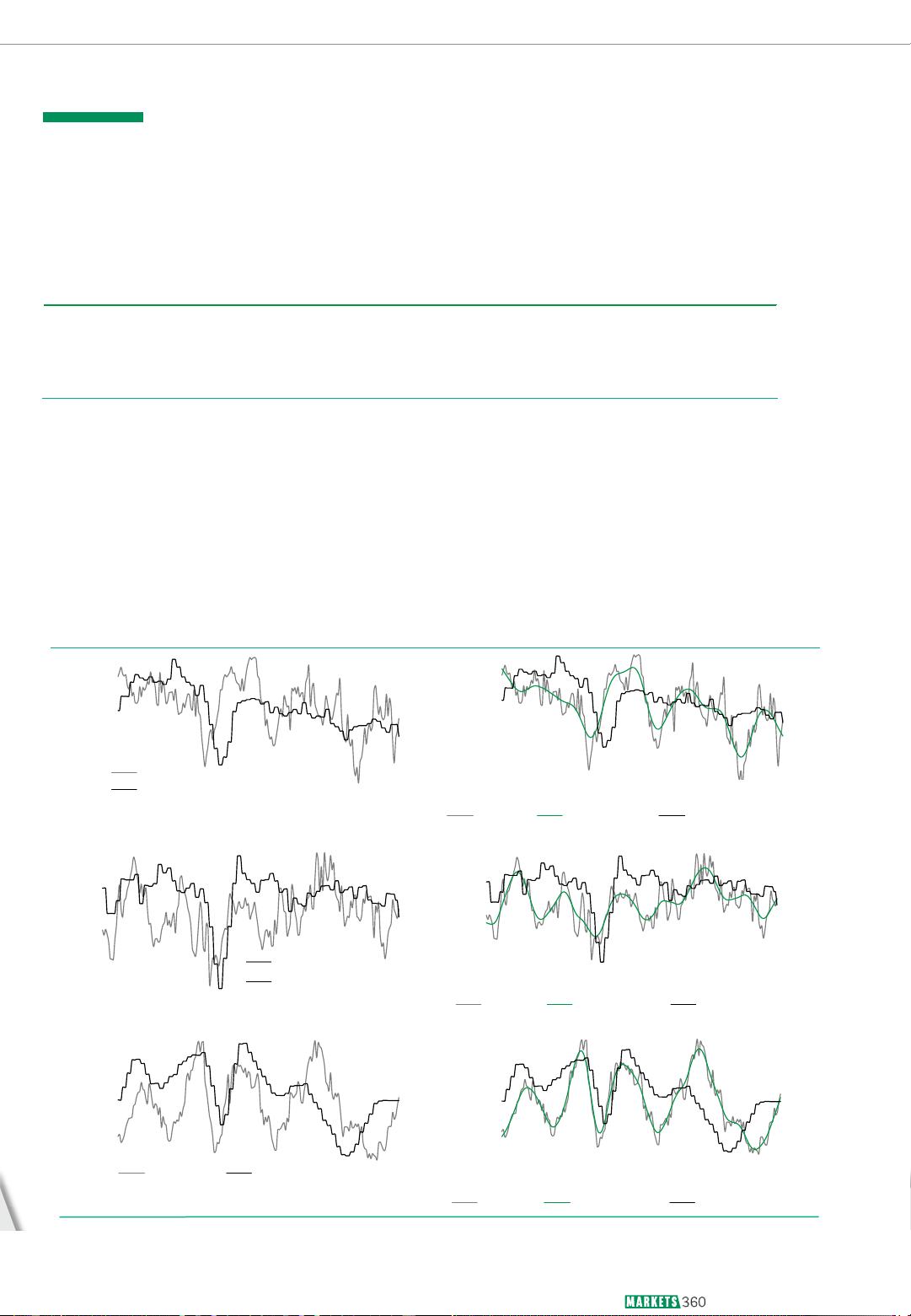

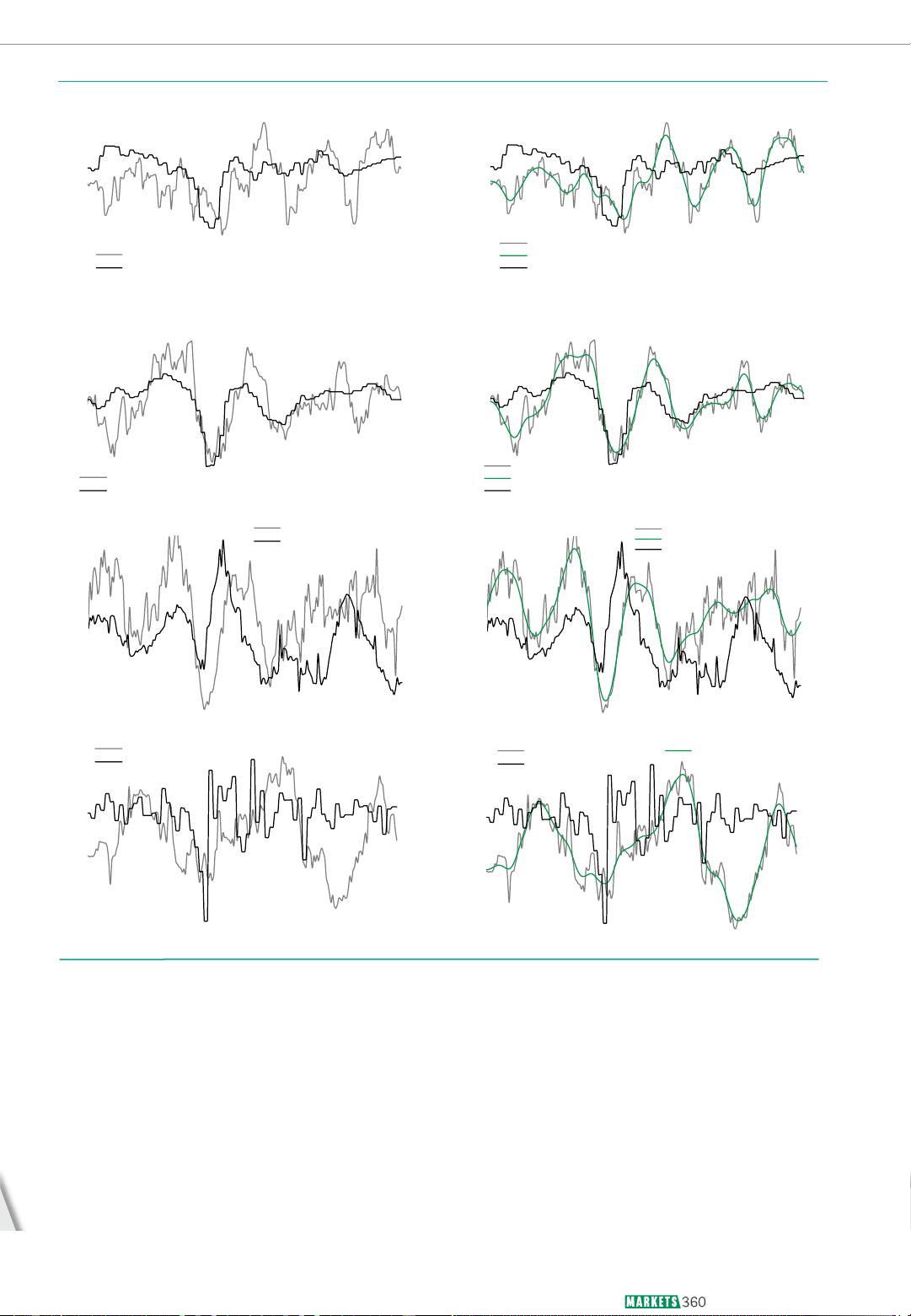

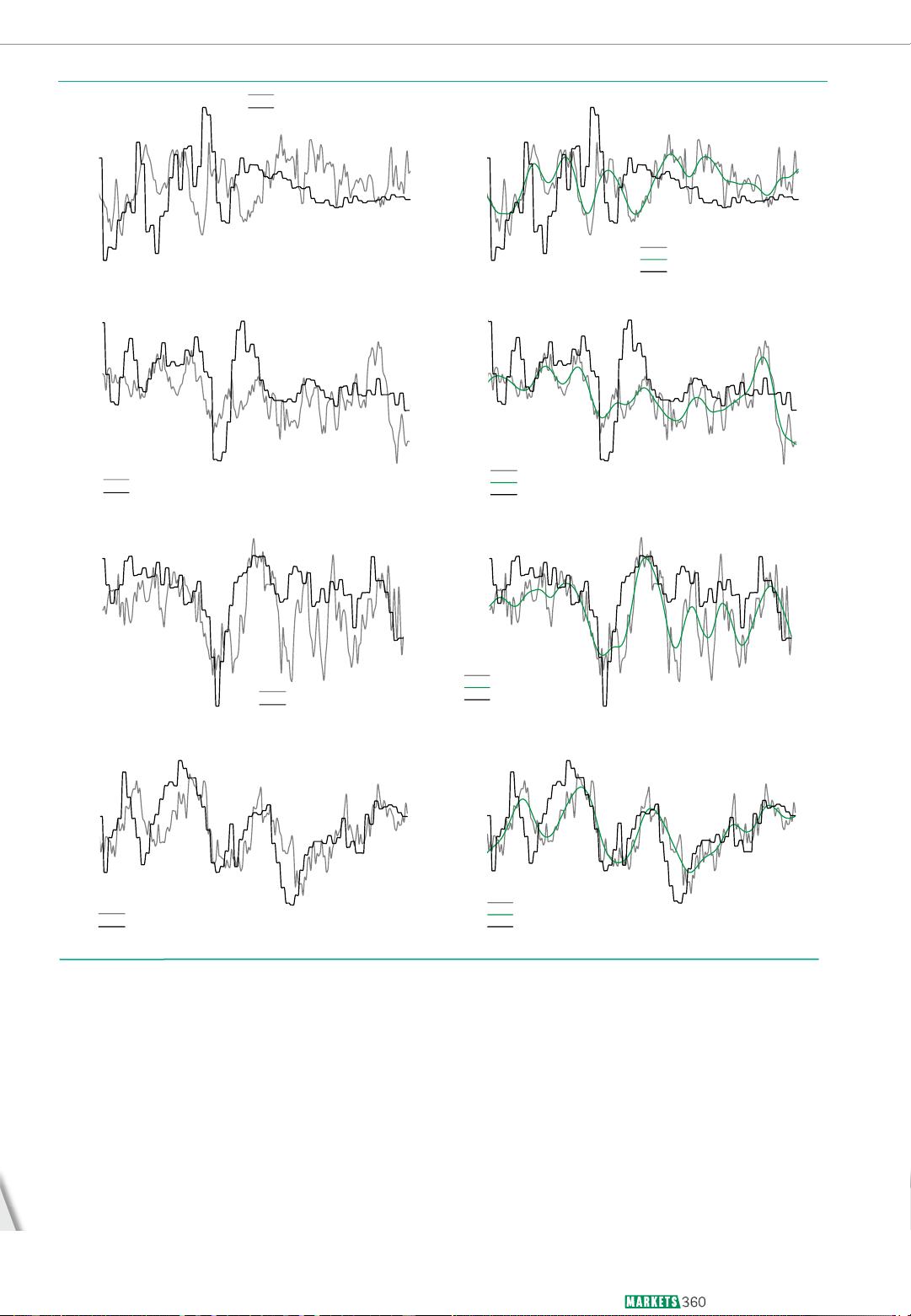

Our results: The results of our analysis are

illustrated in Figure 1. A full review of the results is

set out by country on pages 6–16 below.

Fig. 1:

Market and economic-based current stage of the cycle

剩余24页未读,继续阅读

资源评论