巴克莱-美股-航空航天与国防行业-美国航空航天与国防:未来收益思考-117-35页.pdf

需积分: 0 7 浏览量

2023-07-24

16:38:36

上传

评论

收藏 657KB PDF 举报

Equity Research

17 January 2019

CORE

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only a single factor in making their investment decision.

PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 29.

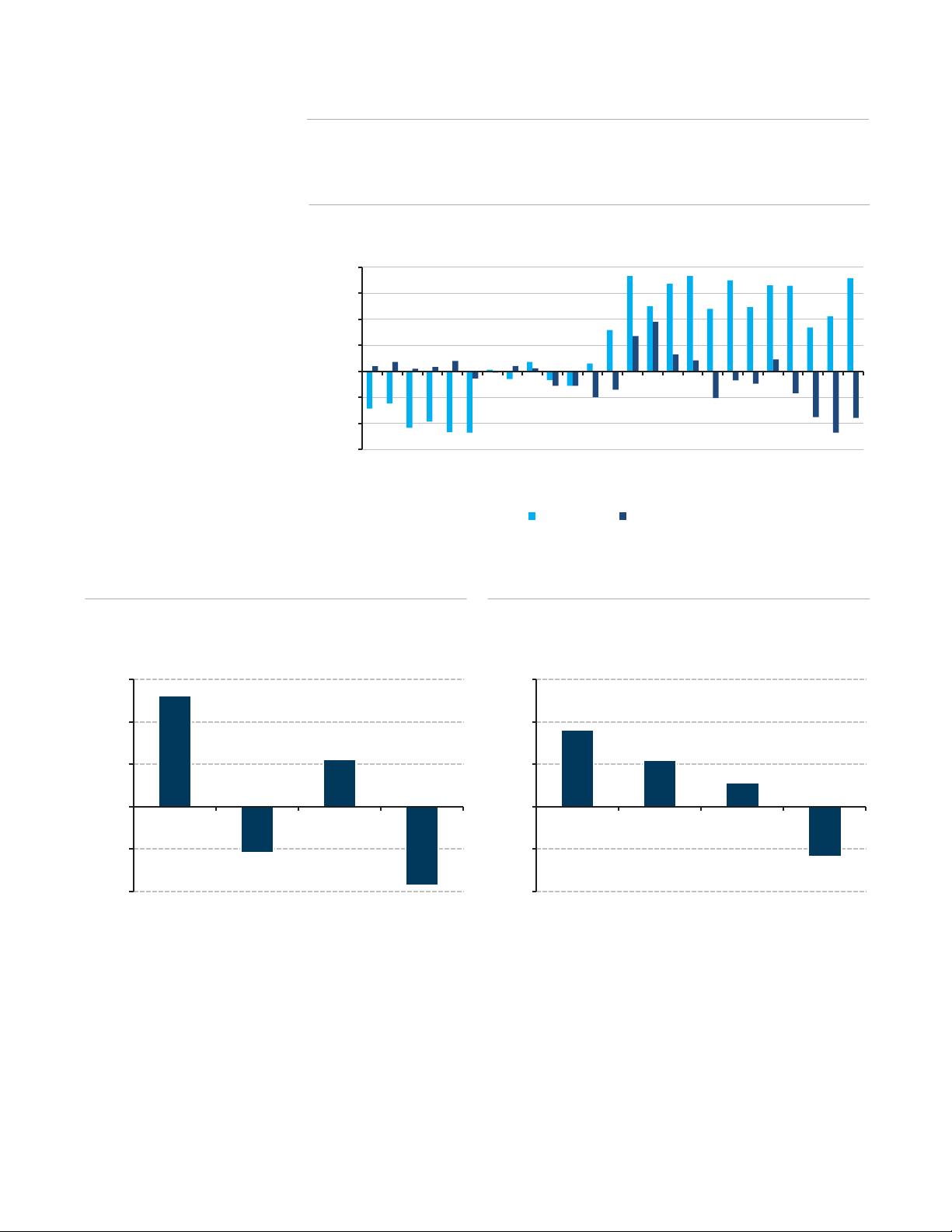

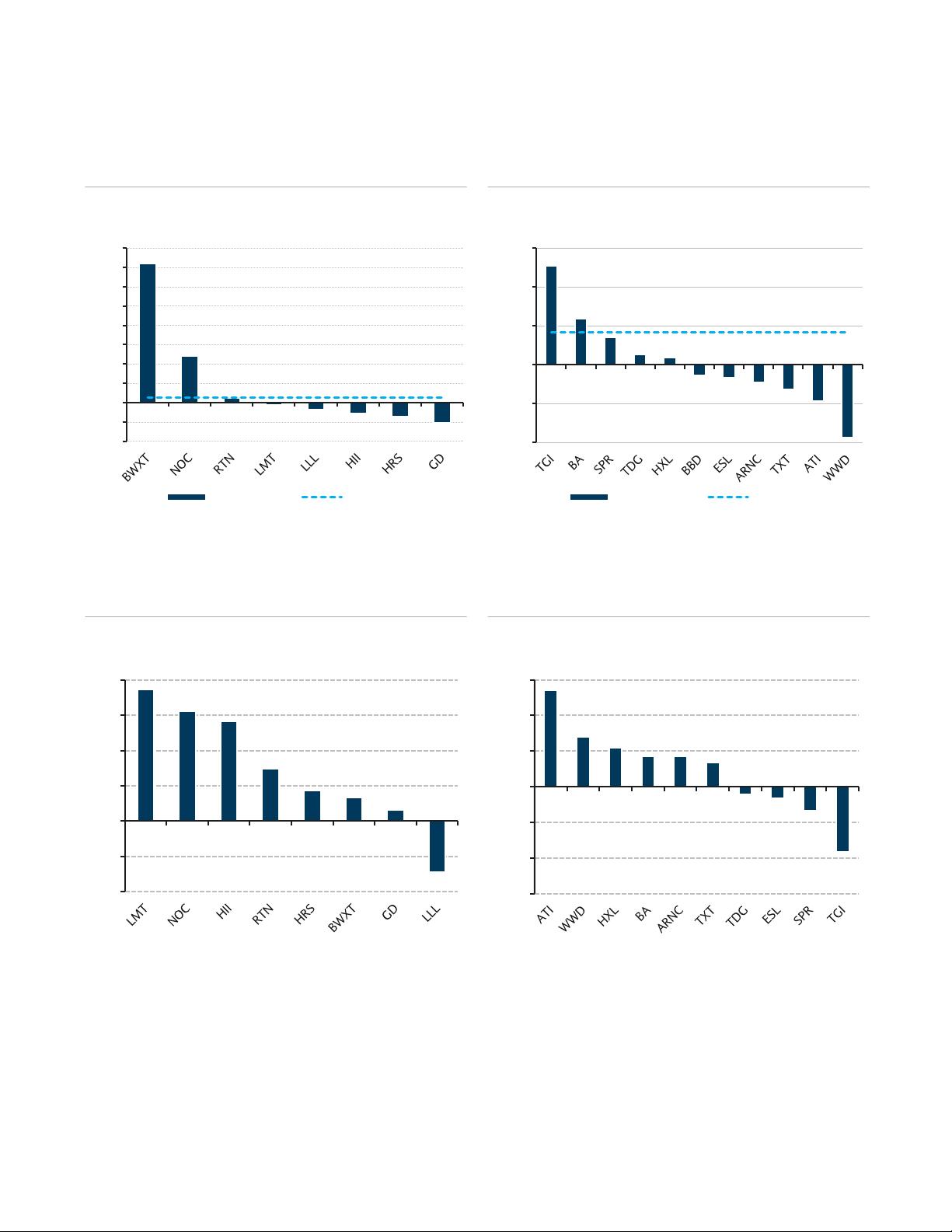

U.S. Aerospace & Defense

Our Take on Upcoming Earnings

A&D earnings begin with ATI on January 22. For defense, highlight will be initial 2019

guidance out of GD/NOC as compared to prior LMT/RTN guidance that reflects 6-8%

revenue growth, flat to down margins, but not much in the way of pre pension FCF

growth. For aerospace, BA delivery guidance in light of lingering narrowbody

production issues and expected 2H 2019 ramp is key while we expect continued strong

aftermarket results across the group despite difficult comp. Favorable raw material

moves should benefit ARNC/HXL in 2019 whereas ATI will be negatively impacted by

lower metal surcharges.

For companies still to give 2019 EPS guidance, we are ahead on GD (see below)

while below on HII (pension) and TXT (weak Industrial/Systems). Consensus

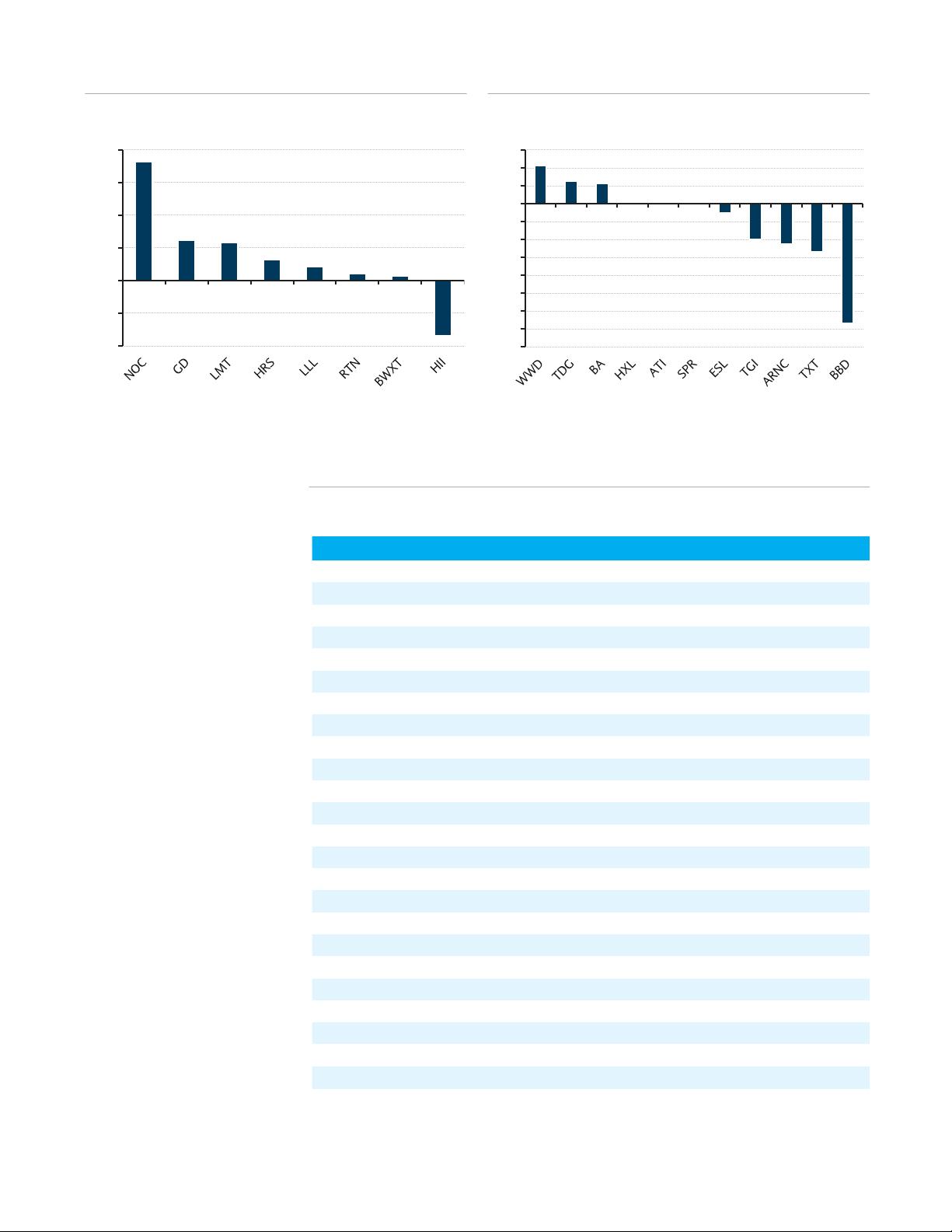

expectations have fallen for GD and TXT over the last month.

Major Q4 corporate events that we would highlight include: HXL acquisition of ARC

(accretive), NOC $1B ASR and move to mark-to-market pension accounting, SPR MOA

with BA that postpones advance repayments (positive for FCF) and TXT Industrial

restructuring.

We see pension as a risk item for 2019 guidance as we estimate that negative asset

returns that were ~13% below assumed returns hurt more than slightly higher discount

rates (50bps) help. We see the biggest risk to companies with large pension deficits

relative to their size, including HII in defense and then ARNC and ATI in aerospace. We

also see pension hit for LMT and RTN, although it is mitigated by initial guidance that

already reflects relatively flat asset returns.

For BA, we see FCF growing in 2019 on higher 737/787 production and some KC-46

tailwind, overcoming likely 777X and prepayments drags, although we forecast slower

incremental FCF growth than recent years. Aero aftermarket up against tougher 13%

comp from Q4 last year, although we still see high single digit growth driven by a

favorable fleet mix of increasing older out-of-warranty aircraft.

Consensus expectations for GD now only reflect 5% EPS growth after adjusting for

~$0.25 of one time CSRA costs in 2018. GD typically guides conservatively without

share repurchase, but even so 5% growth looks light to us given easy comp on CSRA

intangible amortization along with some modest EBIT growth at Gulfstream as we think

low margin G500 deliveries are behind by Q2. In addition, based on its recent

reauthorization, GD appears to have stepped up its buyback in Q4, pivoting away from

paying down CSRA related CP as it had previously planned.

We expect NOC to guide organic growth (ex OA) to mid single digits (lower end of

LMT/RTN) as AS growth moderates on B-21 transition to late stage development along

with continued drag from TS. We also only see slightly higher YOY FCF in 2019 on

negative OA FCF comp as 2018 didn’t include seasonally weak 1H FCF (deal closed in

June 2018) along with higher CAPX and neutral pension cash.

INDUSTRY UPDATE

U.S. Aerospace & Defense

POSITIVE

Unchanged

For a full list of our ratings, price target and

earnings changes in this report, please see

table on page 2.

U.S. Aerospace & Defense

David Strauss

+1 212 526 5580

david.strauss@barclays.com

BCI, US

Matt Akers, CFA

+1 212 526 9019

matt.akers@barclays.com

BCI, US

Kate Copouls, CPA

+1 212 526 3283

kate.copouls@barclays.com

BCI, US

剩余34页未读,继续阅读

资源评论