Equity Research

22 April 2021

U.S. Equity Strategy

Continued EPS surprise vs pervasive

overvaluations: Who wins?

The streak of strong positive EPS surprises is likely to continue,

but elevated valuations have now become pervasive; sentiment

is too optimistic; and a potential change in corporate taxation is

an overhang. We raise our SPX FY21E EPS to $190 and our 2021

price target to $4,400 but caution that further upside is unlikely.

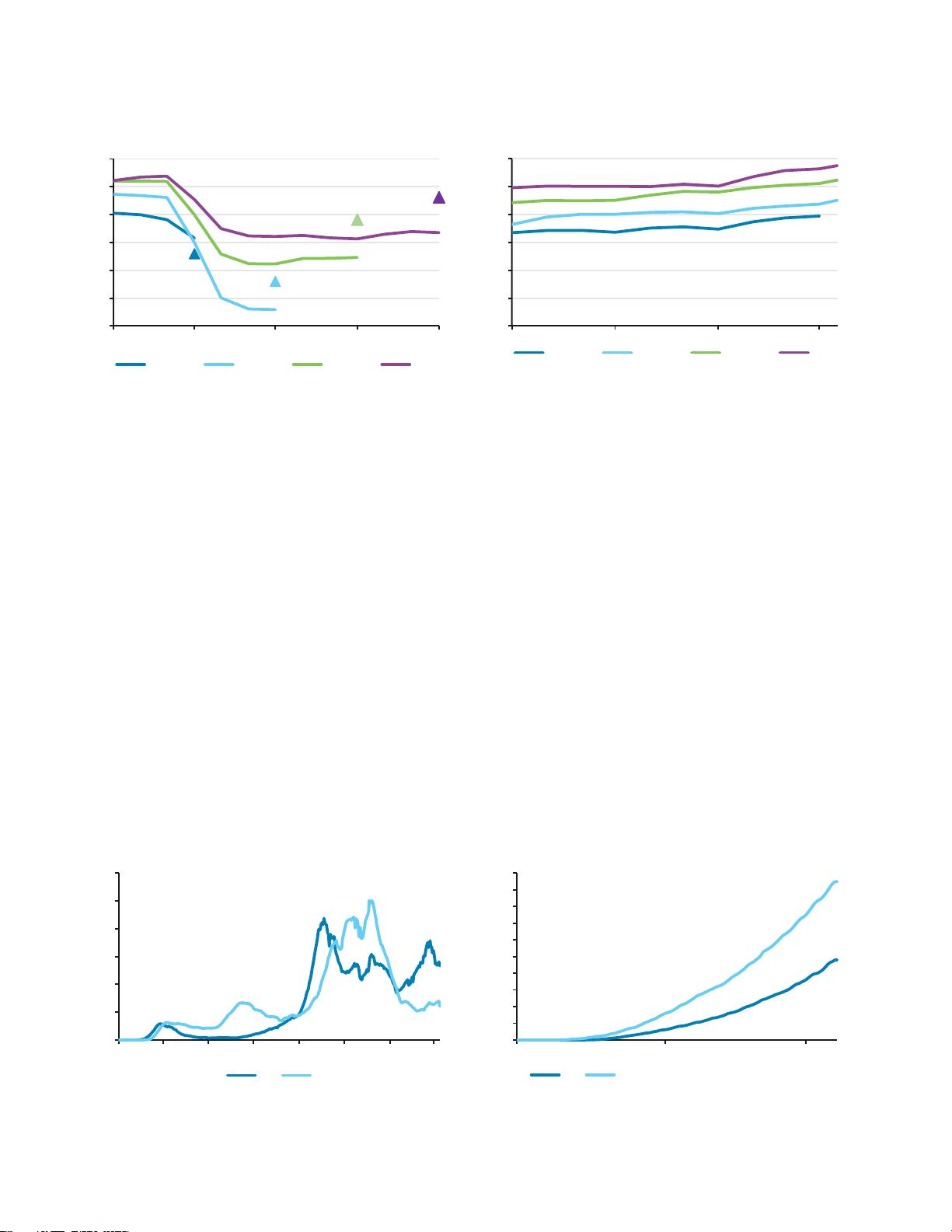

Consensus is not incorporating recent EPS surprises. Although S&P 500 earnings have

surprised three times in a row, consensus has not incorporated these into future earnings. Each

successive beat has been viewed as a one-o event and has had only a modest eect on

earnings projections, eectively lowering QoQ growth forecasts. We construct a simple “surprise

catch-up” model that applies pre-earnings announcement QoQ growth forecasts to actual EPS

and show that it would have done a remarkably good job in forecasting 20Q3 and 20Q4 earnings

and would have been equally eective during the 2009 recovery from the credit crisis. Our

model currently forecasts CY21 earnings of $195 versus the current consensus expectation of

$176. This is not that far from our top-down model forecast of $190, which relies solely on

economic forecasts, but much below our bottom-up model, which starts with consensus.

Hence, we raise our SPX FY21 EPS forecast to $190 from $173.

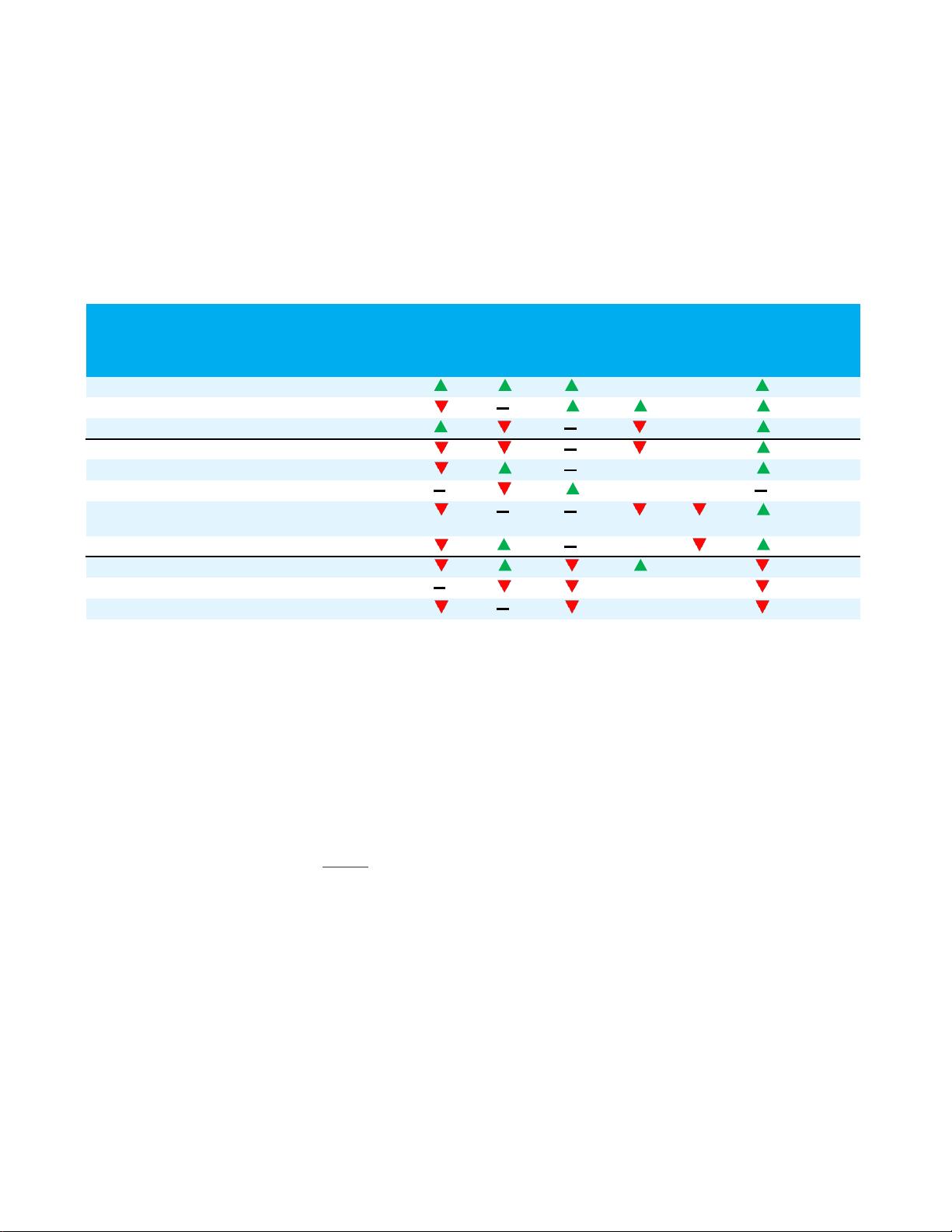

We expected SPX valuation to contract, but not enough to oset higher EPS growth.

Current SPX valuations look highly elevated and are facing several notable headwinds that

should cause a contraction to more reasonable levels by EOY 2021. These include: 1) the rise in

valuations for many cyclical sectors, beyond just the names with medium-term positive

exposure to Covid-19, 2) overly optimistic retail sentiment, as seen in strong fund flows, strong

readings in the AII Bull-Bear indicators, high levels of call buying by retail investors, and

increasing hedge fund beta, 3) an overhang from a potential corporate tax hike, which could

impact SPX EPS by as much as ~8% in FY2022, and 4) strong indications that we are well into the

early/middle expansion phase of the business cycle, which is usually a period of valuation

contraction. Given these significant headwinds, we expect the SPX P/E to decline from

28.8x currently to 23.1x by the end of 2021. Our target FY21 P/E of 23.1x combined with a

target EPS of $190 results in an SPX 2021 price target of $4,400.

We upgrade Financials to OW and downgrade Hardware & Semis ex FANMAG to MW. Our

multi-pronged approach to sector allocation marries our valuation framework with our

“surprise catch-up” model, the allocations for our optimal business cycle stage basket, impact

from potential enactment of President Biden’s fiscal plan, and industry-specific factors for each

sector. We upgrade Financials to OW as our “surprise catch-up” model indicates higher FY21 EPS

Barclays Capital Inc. and/or one of its ailiates does and seeks to do business with companies

covered in its research reports. As a result, investors should be aware that the firm may have a

conflict of interest that could aect the objectivity of this report. Investors should consider this

report as only a single factor in making their investment decision.

Please see analyst certifications and important disclosures beginning on page 23 .

FOCUS

Macro Strategy

U.S. Equity Strategy

Maneesh S. Deshpande

+1 212 526 2953

maneesh.deshpande@barclays.com

BCI, US

Elias Krauklis

+1 212 526 9376

elias.krauklis@barclays.com

BCI, US

Japinder Chawla, CFA

+1 212 526 2771

japinder.chawla@barclays.com

BCI, US

Completed: 22-Apr-21, 01:05 GMT Released: 22-Apr-21, 04:10 GMT Restricted - External

剩余29页未读,继续阅读

资源评论

mylife512

- 粉丝: 1464

- 资源: 1万+

最新资源

- Kotlin 扩展函数,Kotlin 使程序员能够向现有类添加更多功能,而无需继承它们

- 海洋生物检测31-YOLO(v5至v9)、COCO、CreateML、Darknet、Paligemma、TFRecord、VOC数据集合集.rar

- 昆仑通态pro触摸屏软件构件详细教程

- ESP32实战-WiFi遥控小车

- 为什么 Java 中 char 的大小是 2 个字节? 与使用 ASCII 字符集的语言(如 C 或 C++)不同 ,Java 使用 Unicode 字符集来支持国际化

- 海洋生物检测27-YOLO(v5至v9)、COCO、CreateML、Darknet、Paligemma、TFRecord、VOC数据集合集.rar

- 海洋生物检测26-YOLO(v5至v9)、COCO、CreateML、Darknet、Paligemma、TFRecord、VOC数据集合集.rar

- C#算术运算符,关系运算符案例代码,运算符是任何编程语言的基础

- bugTest(1).cpp

- tomcat 10 版本的

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈