ab

Global Strategy

CTAs' Positioning and Flows - Biweekly Update

!

"#$#!

• Despite the S&P making new all-time highs, CTAs have quietly been reducing their

equity exposure (by $15/20bln, ie. ~20%). They notably sold the UK FTSE and European

indices, which have been trading in ranges since May, and now appear close to their

breaking points. Declining realized volatilities will be helpful near-term, masking the

anticipated decline in signalling.

• CTAs are back being net short duration. Their overall level of conviction is at 30%, and

we will need higher yields for CTAs to increase their shorts from here. US and Australia

continue to be the most-at-risk bond markets.

• In Credit, CTAs keep harvesting carry. They are max long the asset class.

• In FX, since October 1st, CTAs have bought $275/300bln of USD, switching from very

short to very long (now at 82%le). The frenzy dollar buying might come to an end, as we

forecast limited flows for the remaining of November. While the EUR, CHF, SEK and GBP

may still face some (mild) CTAs selling pressure in the coming two weeks, commodities

currencies may benefit from some profit taking.

• Limited activity from CTAs in the commodity space since our last update. This is about

to change, as our model anticipates strong selling in Metals, especially in Precious, and

active buying in Energy and Agriculturals.

%&'( )$

a) Equities: bullish most markets, especially US. Bearish Latam indices, Kospi2 & CAC

b) Bonds: bullish Korea & Japan, neutral Canada & EU, bearish US, Australia & UK

c) Credit: bullish across the board

d) Currencies: bullish USD & EMEA FX, neutral GBP, bearish Commo & Latam FX

e) Commodities: bullish Precious, neutral Industrials, bearish Energy & Agriculturals

Potential trades in couple of charts

Levels to watch on S&P 500

Levels to watch on UST 10y

What our CTA model says about FX?

What our CTA model says about Equities?

What our CTA model says about Rates?

What our CTA model says about Credit?

What our CTA model says about Commodities?

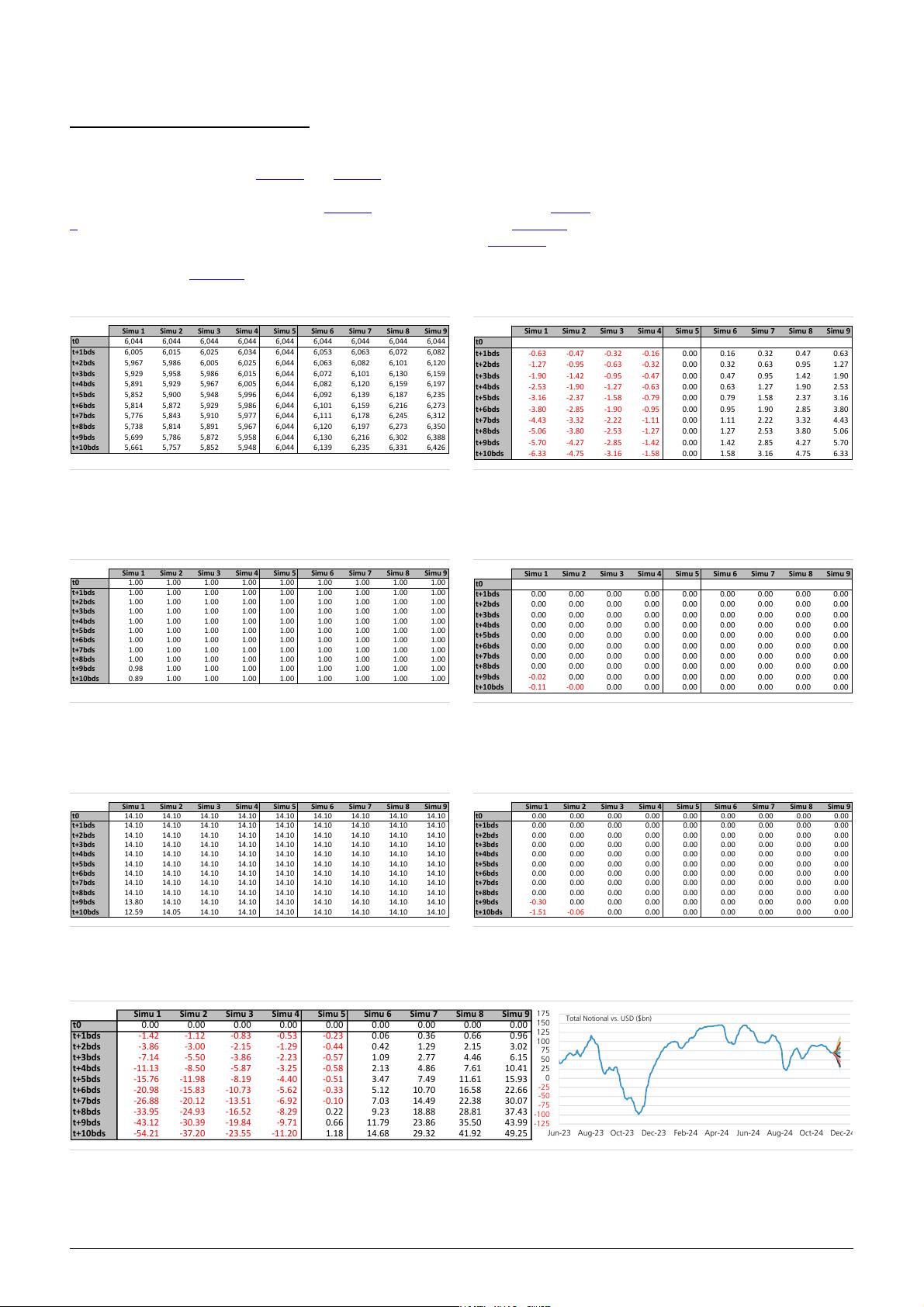

*& %"+! , '&

-1.00

-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

US10Y EU10Y SPX SX5E MESA

(EM Eq)

XIN9I EUR MXN CNH CdxHY Crude Gold

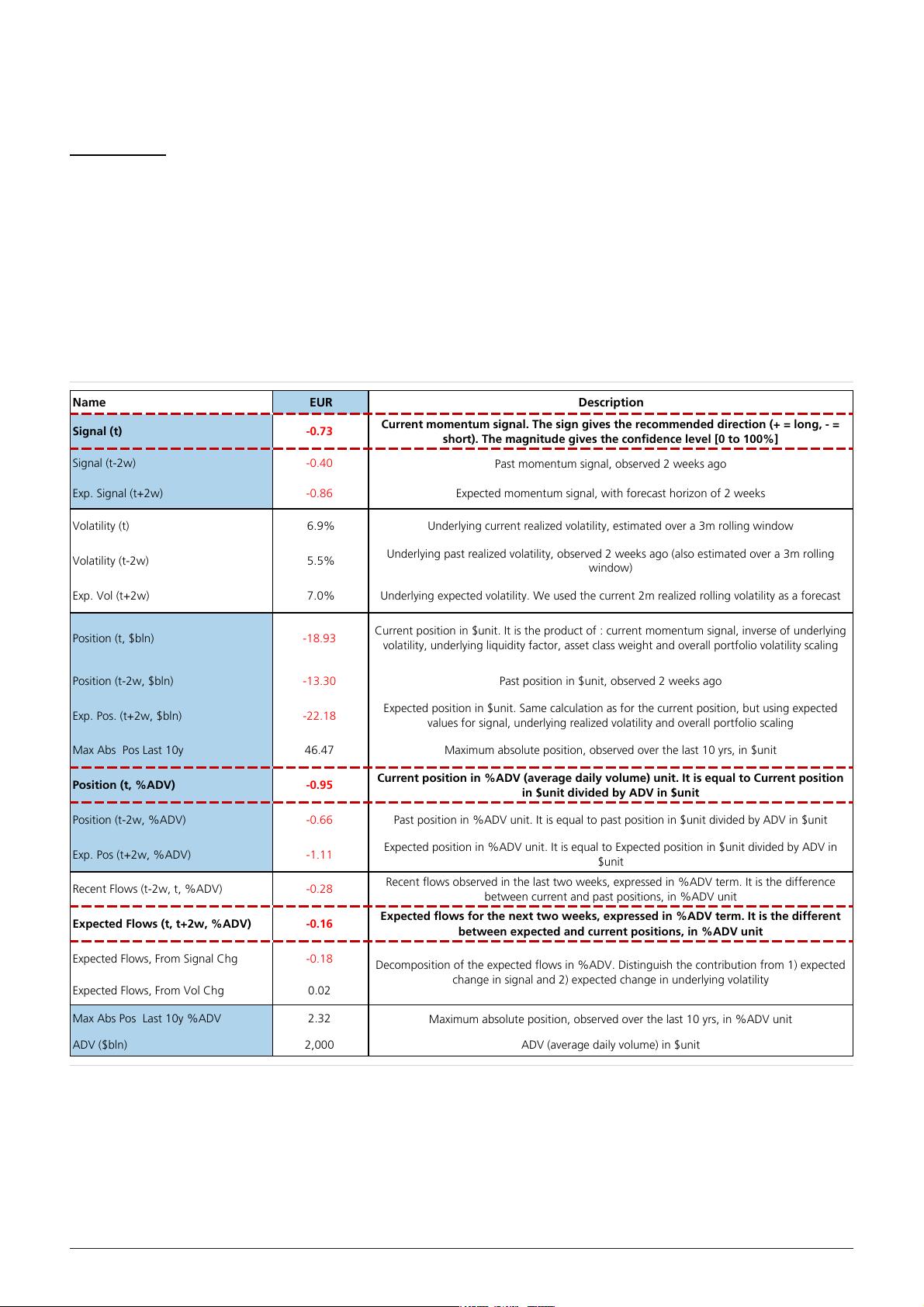

Signal (t)

Exp. Signal (t+2w)

Signal value [-1,+1]

Source: UBS, Bloomberg

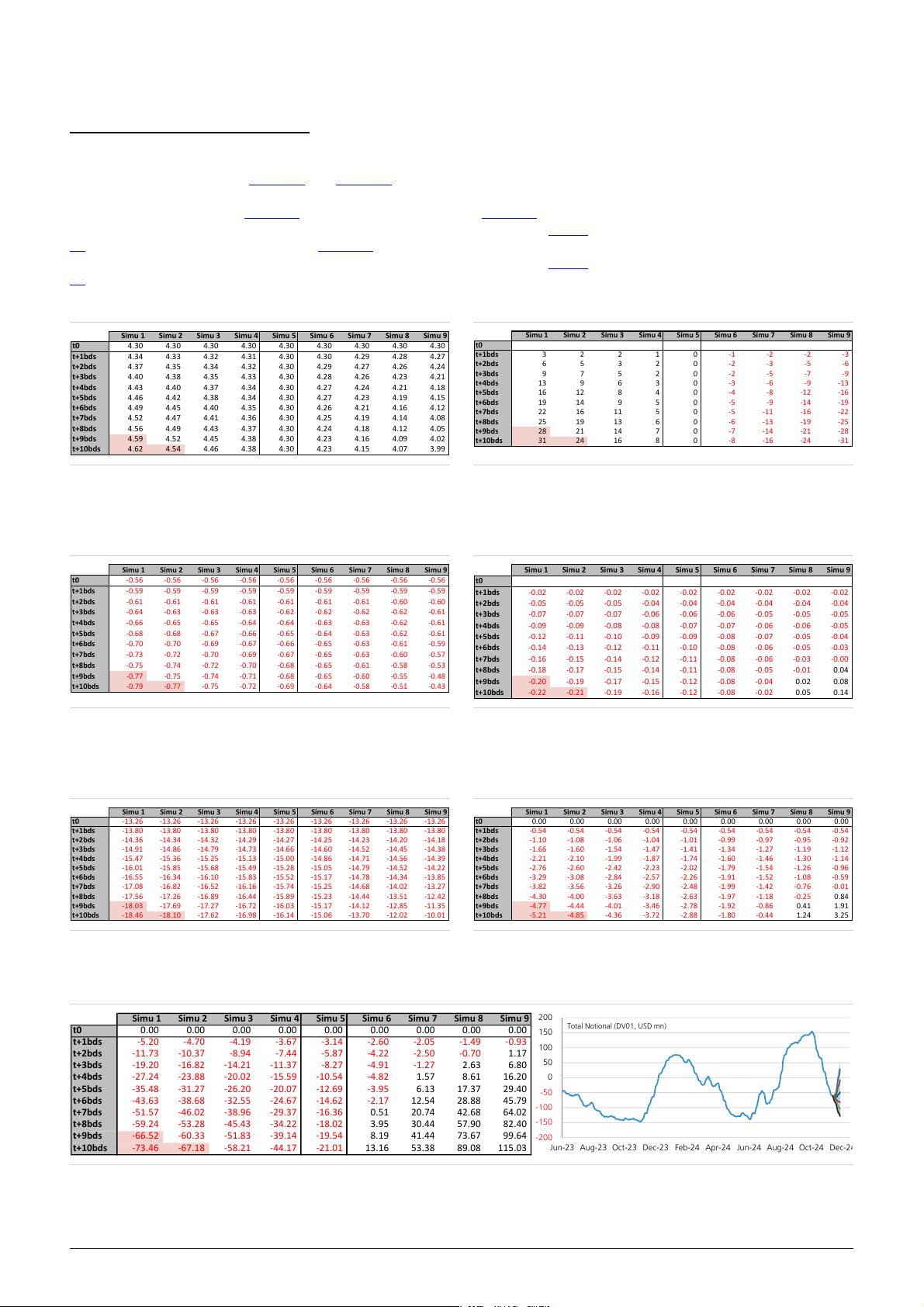

*& % ! -! # . /

+01,'

-10

-5

0

5

10

15

US10Y EU10Y SPX SX5E MESA

(EM Eq)

XIN9I EUR MXN CNH CdxHY Crude Gold

Position (t, %ADV) Expected Flows (t, t+2w, %ADV)

(%ADV)

CDX HY: +31% ADV

Source: UBS, Bloomberg

This report has been prepared by UBS Europe SE. ++23 " %4"5*5%+"56 + 4(54 5 %26 (4 $ 789:;<78=

78>?@ABC7?8?8CDE;B8C7CBC7FEEGEB@9DEF7EHI;J:7GDE<JK(L $JE=78?8IB=EMN

O

Global

2-

Strategist

nicolas.le-roux@ubs.com

+33-14-888 5000

LL#,

Strategist

bhanu.baweja@ubs.com

+44-20-7568 6833

PQ

Analyst

paul-j.winter@ubs.com

+61-2-9324 2080

RO

Strategist

james.malcolm@ubs.com

+44-20-7568 8924

O'

Strategist

manik.narain@ubs.com

+44-20-7568 3635

O%

Strategist

mike.cloherty@ubs.com

+1-203-719 4281

O#O$%*+

Strategist

matthew.mish@ubs.com

+1-203-719 1242

*#

Strategist

gerry.fowler@ubs.com

+44-20-7567 5490

R%S

Strategist

julien.conzano@ubs.com

+44-20-7567 2067

O-#$%*+

Strategist

maxwell.grinacoff@ubs.com

+1-212-713 3892

剩余32页未读,继续阅读

资源评论

soso1968

- 粉丝: 3321

- 资源: 1万+

最新资源

- 基于UDS协议的Bootloader 采用autosar架构的标准,DCM集成uds协议,nxpS32K,tc275,tc233,tc234,nxp148,tc1782,NXP5746,NXP5748

- 开绕组电机的控制策略,SVPWM仿真的双闭环控制,控制效果优良,具有快速响应性能,对开绕组电机的控制策略,故障容错,共模电压电流抑制都有所了解 同步电机开绕组与异步电机开绕组都有

- 宝马股票价格数据,BMW股票价格数据 (1996 - 2024)

- genad-hGridSample-test.hbm.png

- VSG模型仿真,和单台同步机的联合仿真模型 在负荷扰动下进行了验证 有详细的技术报告,包括所有参数的设置原理 可将vsg接入3机9节点

- comsol一维管道流模型,集非等温管道流模块、浓物质传递模块和化学反应模块为一体,三物理场耦合,本模拟以甲烷气体为例进行模拟仿真,涉及了GRI-3.0最为核心的Z40反应和其余的附加反应,反应结果真

- 蛋白质数据集,生物信息学蛋白质数据集,物理性质和功能分类的合成蛋白质数据集

- sgdgcxkdshloxdjsalcxhksdgcxdsyjt

- HC32L196串口中断发送数据

- AI时代下的汽车-分析报告

- Turbo编译码实现 通信专业 信道编码译码识别 接turbo码译码算法仿真 译码算法logmap sova

- 加载富文本框鼠标右键菜单翻译文件

- django南京某高校校园外卖点餐系统-j2k3o(源码+数据库+论文+PPT+包调试+一对一指导)

- msys2-x86-64-20230318.exe

- HP DL380 Gen9 BIOS/BMC 固件及bmc中文语言包/升级教程

- 单相九电平级联NPC逆变器模块,输入250V直流,输出交流幅值1000V,电阻负载 PLECS平台搭建,MATLAB simulink也可实现

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈