THE EUROPEAN UNION IN THE COVID-19

STORM: ECONOMIC, POLITICAL AND

STABILITY CHALLENGES

Stability in the time

of COVID-19

I FEBRUARY 2021

The COVID-19 pandemic struck the European Union in

early 2020, entering the regional bloc through its Southern

Periphery. Italy, together with China and South Korea,

was one of the countries most aected by the initial virus

spread. Besides the huge human toll,

1

the adoption of

strict lockdown measures and the subsequent major dis-

ruptions in both supply and demand have resulted in

the most severe recession in recent history, with regional

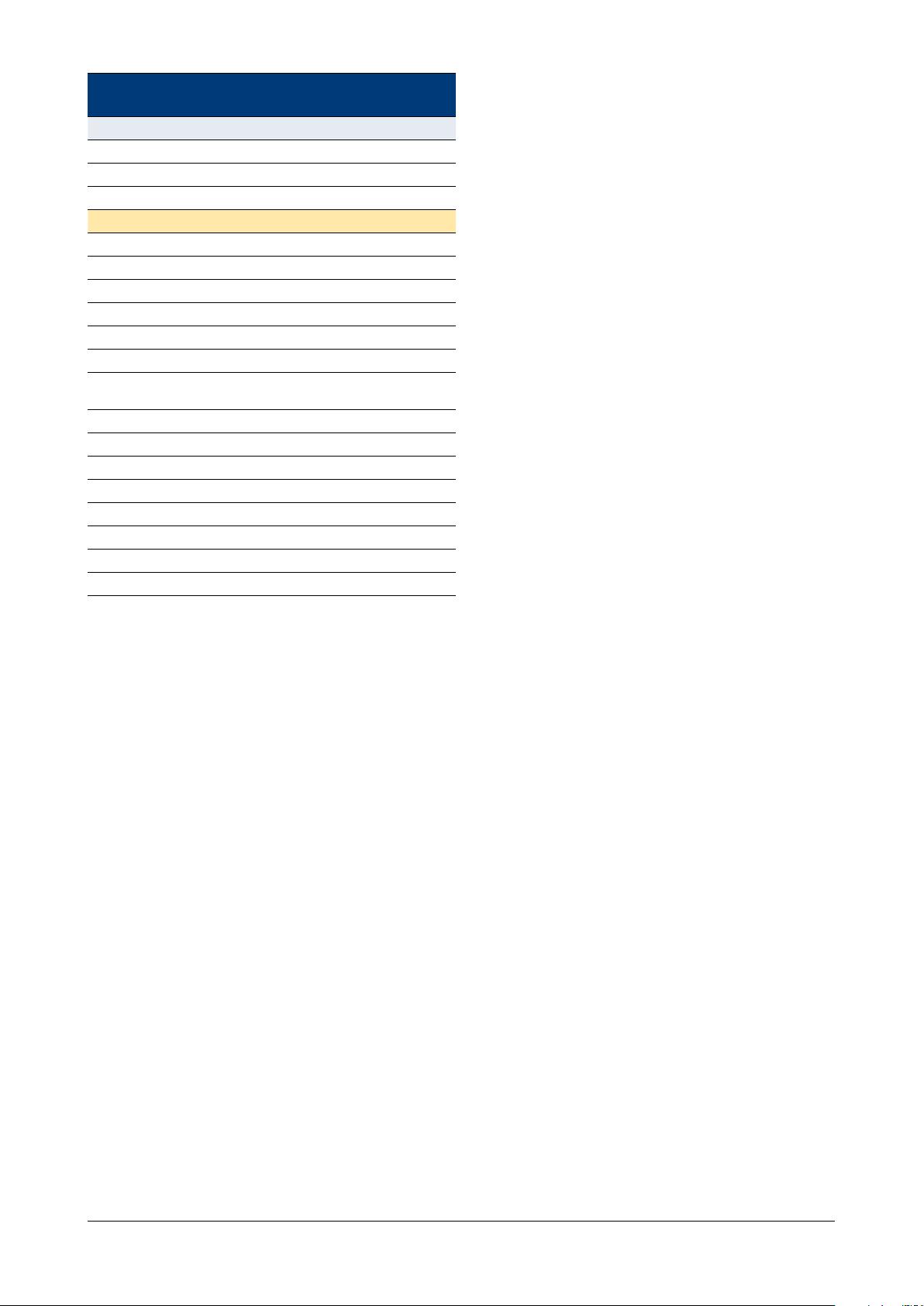

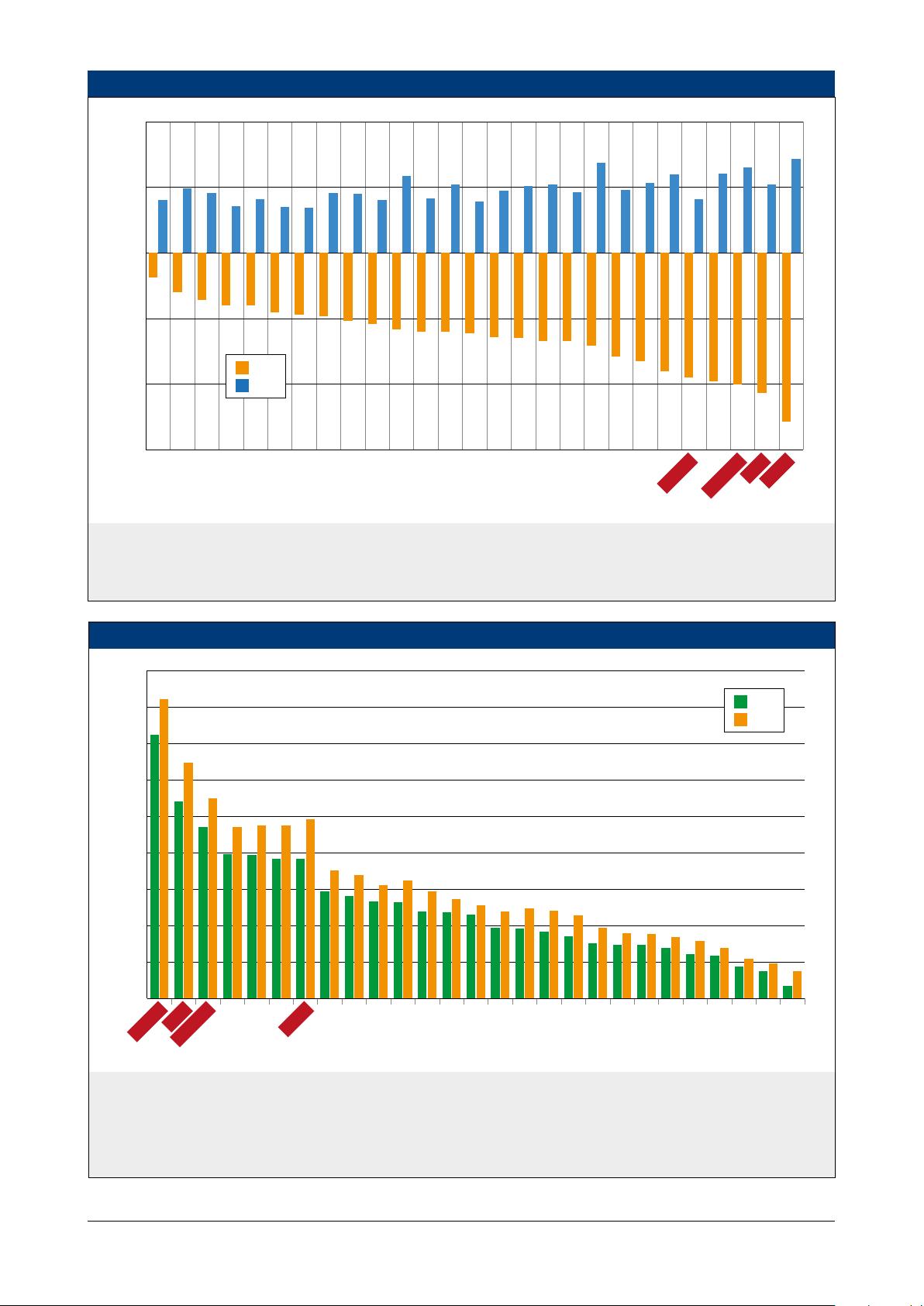

GDP estimated to have contracted by a record 7.6% in

2020, the largest drop since the Second World War (see

This is the fth in a series of papers aimed at understanding and analysing the multiple ways

the ongoing COVID-19 pandemic is aecting stability in dierent parts of the world.

The papers concentrate on the pandemic’s impact on security, governance, trade and

geo-economics.

KEY MESSAGES

The International Institute for Strategic Studies

The COVID-19 pandemic has plunged the European Union into the most severe recession in its recent history,

exacerbating existing imbalances and divergences between members. The health emergency has hit the Southern

Periphery region (comprising Greece, Italy, Portugal and Spain) particularly hard, compounding its existing struggles with

stagnant growth, high debt levels and competitiveness aws. Although some recovery is forecast for 2021, the social,

political and economic consequences of the pandemic will be long lasting.

The quality of governance in dierent EU countries aected their resilience to the initial COVID-19 shock and will be key for

the success of the EU-directed policy responses. Structural reforms to improve economic eciency and boost institutional

eectiveness will be essential to ensure durable growth (and access to EU funds). But they remain unpopular domestically.

Shortages of medical and pharmaceutical products have provided a perfect business opportunity for organised-crime

groups in the EU, with a surge in the production and commercialisation of counterfeit and substandard high-demand

medical goods, including vaccines. Better enforcement and awareness campaigns will be needed to address this issue.

After some initial hesitancy, the EU adopted a comprehensive and multifaceted strategy to tackle the pandemic,

supported by an unparalleled mobilisation of regional resources. The strategy is aimed at boosting the immediate

recovery while driving a longer-term transformation towards more resilient, sustainable and inclusive economic models.

The EU response featured several novel elements, such as the ‘mutualisation’ of debt – a victory for the Southern

Periphery states against the ‘frugal four’ (Austria, Denmark, Netherlands and Sweden) – and the conditionality of the

disbursement of EU funds on respect for the rule of law.

The pandemic threatens to accentuate existing trends of political fragmentation and popular dissatisfaction with the

status quo, increasing the risk of political instability.

The eectiveness of the EU-supported recovery and structural transformation of regional economies will be an inection

point for the durability and resilience of the EU project.

剩余12页未读,继续阅读

资源评论

qw_6918966011

- 粉丝: 26

- 资源: 6166

最新资源

- C语言-leetcode题解之28-implement-strstr.c

- C语言-leetcode题解之27-remove-element.c

- C语言-leetcode题解之26-remove-duplicates-from-sorted-array.c

- C语言-leetcode题解之24-swap-nodes-in-pairs.c

- C语言-leetcode题解之22-generate-parentheses.c

- C语言-leetcode题解之21-merge-two-sorted-lists.c

- java-leetcode题解之Online Stock Span.java

- java-leetcode题解之Online Majority Element In Subarray.java

- java-leetcode题解之Odd Even Jump.java

- 计算机毕业设计:python+爬虫+cnki网站爬

资源上传下载、课程学习等过程中有任何疑问或建议,欢迎提出宝贵意见哦~我们会及时处理!

点击此处反馈