Sampling methods for uncertainty analysis

Simple random sampling

Simple random sampling involves repeatedly forming random vectors of parameters from

prescribed probability distributions. A normally-distributed random variable x with mean

µ

and standard deviation

σ

can be generated by:

x* =

σ

r

n

+

µ

where r

n

are normally distributed random numbers with mean 0 and variance 1.

A multivariate normal distribution with variance-covariance matrix V can be

sampled utilising the lower and upper triangular matrix (LU) decomposition method

(Davis, 1987). The variance-covariance matrix V is first decomposed by Cholesky

factorization:

V = L L

T

where L is the lower triangular matrix. To generate the random variables vector x,

matrix L is multiplied by vector, r

n

, of independent normal random numbers with mean 0

and variance 1:

x = L r

n

+ µ .

The procedure is repeated for sample size ns, resulting in a set of variables with

expected mean vector µ and expected variance-covariance matrix: L cov(r

n

) L

T

. Since

the random numbers are independent, the covariance matrix cov(r

n

) should equal I (the

identity matrix),

L cov(r

n

) L

T

= L I L

T

= L L

T

= V .

Latin hypercube sampling

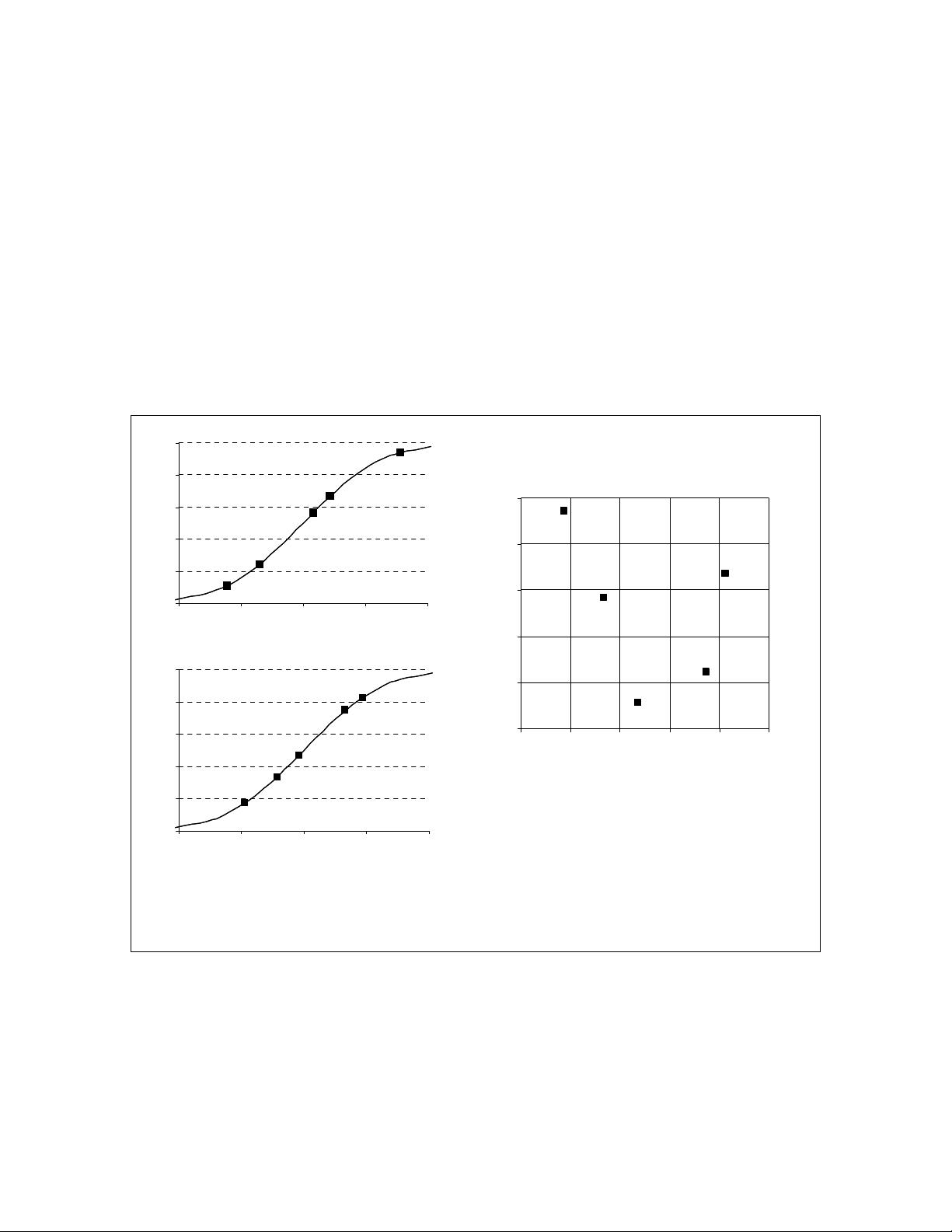

Latin hypercube sampling (LHS), a stratified-random procedure, provides an efficient

way of sampling variables from their distributions (Iman and Conover, 1980). The LHS

involves sampling ns values from the prescribed distribution of each of k variables

X

1

, X

2

,

…

X

k

. The cumulative distribution for each variable is divided into N equiprobable

intervals. A value is selected randomly from each interval (Figure 1). The N values

obtained for each

variable are paired randomly with the other variables. Unlike simple

random sampling, this method ensures a full coverage of the range of each variable by

maximally stratifying each marginal distribution.

The LHS can be summarized as:

• divide the cumulative distribution of each variable into N equiprobable invervals;

• from each interval select a value randomly, for the ith interval, the sampled

cumulative probability can be written as (Wyss and Jorgensen, 1998):

Prob

i

= (1/N) r

u

+ (i – 1)/N

where r

u

is uniformly distributed random number ranging from 0 to 1;