汇丰银行-全球-能源设备与服务行业-全球油服——海上钻探:深水的深层价值-225-44页.pdf

需积分: 0 113 浏览量

2023-07-26

11:54:39

上传

评论

收藏 870KB PDF 举报

Disclosures & Disclaimer

This report must be read with the disclosures and the analyst certifications in

the Disclosure appendix, and with the Disclaimer, which forms part of it.

Issuer of report: HSBC Securities and Capital

Markets (India) Private Limited

View HSBC Global Research at:

https://www.research.hsbc.com

THIS CONTENT MAY NOT BE DISTRIBUTED TO THE PEOPLE'S REPUBLIC OF CHINA (THE "PRC")

(EXCLUDING SPECIAL ADMINISTRATIVE REGIONS OF HONG KONG AND MACAO)

We see value in the sector despite a slow recovery in

offshore markets; stocks trading at undemanding valuations

Our proprietary ‘Rig Market Value’ shows ca. 50% upside

across the sector; read across for SPM and MAERSKB

We adjust target prices and estimates to reflect our utilisation

outlook; maintain Buy on RIG, NE and DO

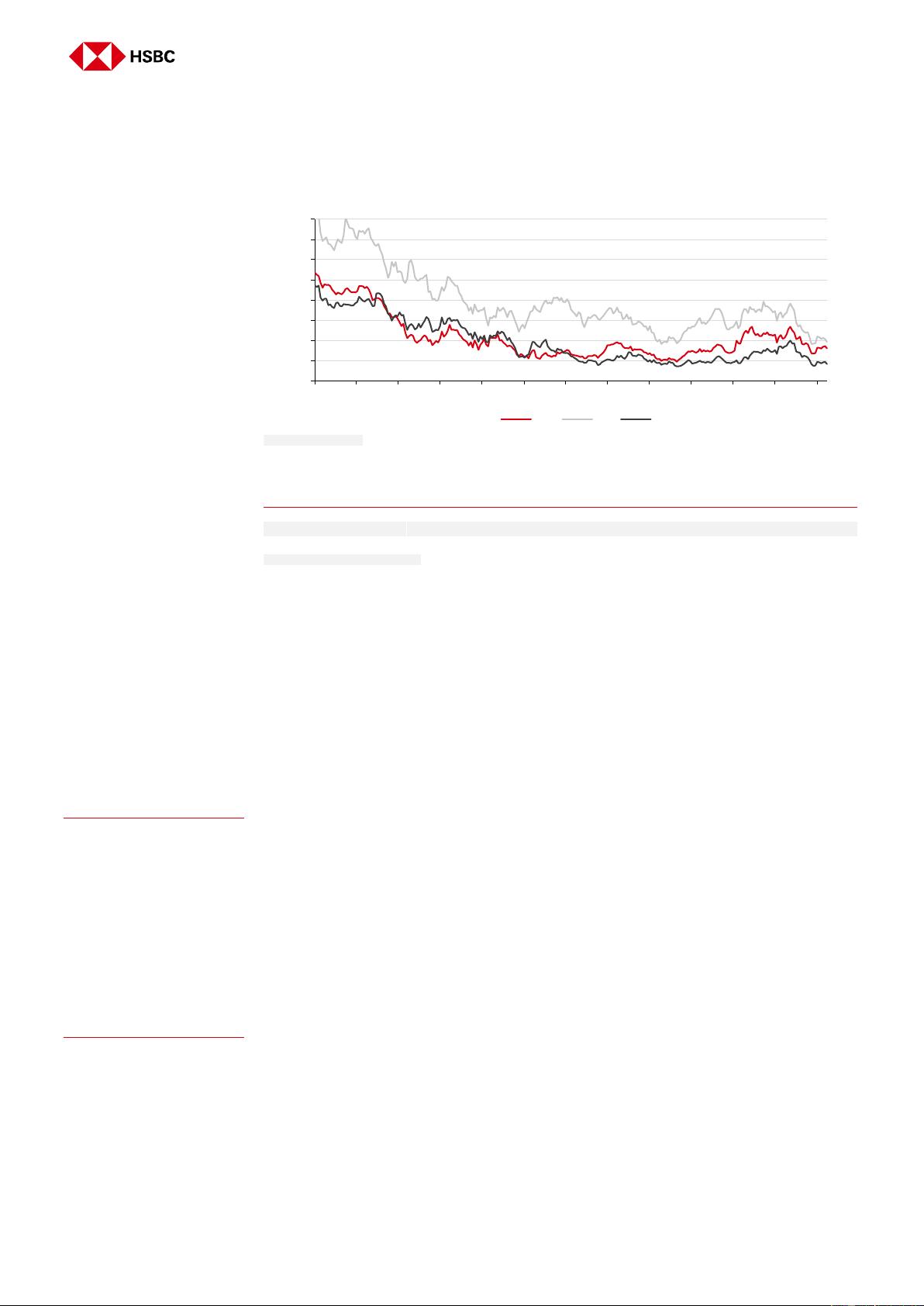

In this report, we discuss why we think current share prices offer deep value opportunities

in this subsector, and are not a value trap. Our analysis suggests that market concerns

over liquidity with the offshore drillers are overdone, with cash needs largely under control

into the early 2020s; we estimate around USD3bn is needed over 2019e-2021e against

total available liquidity of almost USD7bn. We also see sector consolidation as a

continuing theme, and one that supports our rig market value (RMV) calculations.

Context: Despite a drawn-out offshore recovery, we think the fall in the drillers’ share

prices over recent months presents an attractive opportunity. The drillers are at multi-year

lows on price/book metrics, and although the sector is likely to be loss-making until the

early 2020s, we see good value in the stocks (backed by our proprietary rig market value

calculations). Our target prices are on average 50% higher than current market prices.

What’s changed in this report: We adjust our forecasts to reflect Q4 2018 results, new

guidance, recent contract announcements, and our own lower utilization assumptions for

2020e/2021e. On average for our coverage, we lower our forecast EBITDA by 24% for

2019e and 11% for 2020e. We lower our RMV estimates by c13% on average.

Investment view: We see attractive asset-based value across the sector. Our preferred

play is Transocean (RIG) – the market leader with significant exposure to resurgent harsh

environment drilling. Our other Buy-rated names are Diamond (DO) and Noble (NE).

Read-across: Among other Buy-rated companies with offshore drilling exposure, we like

MAERSKB, which announced in August 2018 that it is planning to separately list its drilling

business in 1H 2019 (our RMV sees this fleet worth USD5.2bn), and also SPM, supported

by restructuring and the potential for portfolio change (we estimate SPM’s offshore rig fleet

is worth USD1.5bn).

Key investment ratings and valuations

Company

Ticker

Curr.

Current

Price

Market

Cap (USDm)

New Rating

New TP

Upside/

Downside

___ EV/EBITDA (x) ____

______ PB (x) _______

Old Rating

Old TP

2019e

2020e

2019e

2020e

Transocean

RIG US

USD

8.73

3,975

Buy

Buy

14.60

13.30

52.4%

11.9

11.1

0.4

0.4

Diamond

DO US

USD

10.29

1,414

Buy

Buy

17.20

13.70

33.1%

16.2

18.3

0.4

0.5

Noble

NE US

USD

3.15

777

Buy

Buy

6.10

5.30

68.3%

16.4

11.0

0.2

0.2

Note: Current prices as of close 19 February 2019. Source: Bloomberg, HSBC estimates

25 February 2019

Abhishek Kumar*

Analyst

HSBC Securities and Capital Markets (India) Private

Limited

abhishek.kumar@hsbc.co.in

+91 80 4555 2753

Tarek Soliman*, CFA

Analyst

HSBC Bank plc

tarek.soliman@hsbc.com

+44 20 3268 5528

David Phillips*

Head of Equity Research, Developed Europe

HSBC Bank plc

david.1.phillips@hsbc.com

+44 20 7991 7558

Edward Stanford*

Analyst, Transportation

HSBC Bank plc

edward.stanford@hsbc.com

+44 20 7992 4207

Thomas C. Hilboldt*, CFA

Head of Resources & Energy Research, Asia Pacific

The Hongkong and Shanghai Banking Corporation Limited

thomaschilboldt@hsbc.com.hk

+852 2822 2922

Anshak Singhal*

Associate

Bangalore

* Employed by a non-US affiliate of HSBC Securities (USA) Inc, and is

not registered/ qualified pursuant to FINRA regulations

Global Oilfield Services

Equities

ENERGY EQUIPMENT &

SERVICES

GLOBAL

Offshore Drilling: Deep value in deepwater

剩余43页未读,继续阅读

资源评论