巴克莱-美股-资产管理-美国经纪人、资产管理人与交易员:Q4丑陋的资产管理背景-19-22页.pdf

需积分: 0 147 浏览量

2023-07-26

11:50:02

上传

评论

收藏 490KB PDF 举报

Equity Research

9 January 2019

CORE

Barclays Capital Inc. and/or one of its affiliates does and seeks to do business with

companies covered in its research reports. As a result, investors should be aware that the

firm may have a conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only a single factor in making their investment decision.

PLEASE SEE ANALYST CERTIFICATION(S) AND IMPORTANT DISCLOSURES BEGINNING ON PAGE 17.

U.S. Brokers, Asset Managers & Exchanges

Ugly Asset Mgr. Setup into 4Q Print

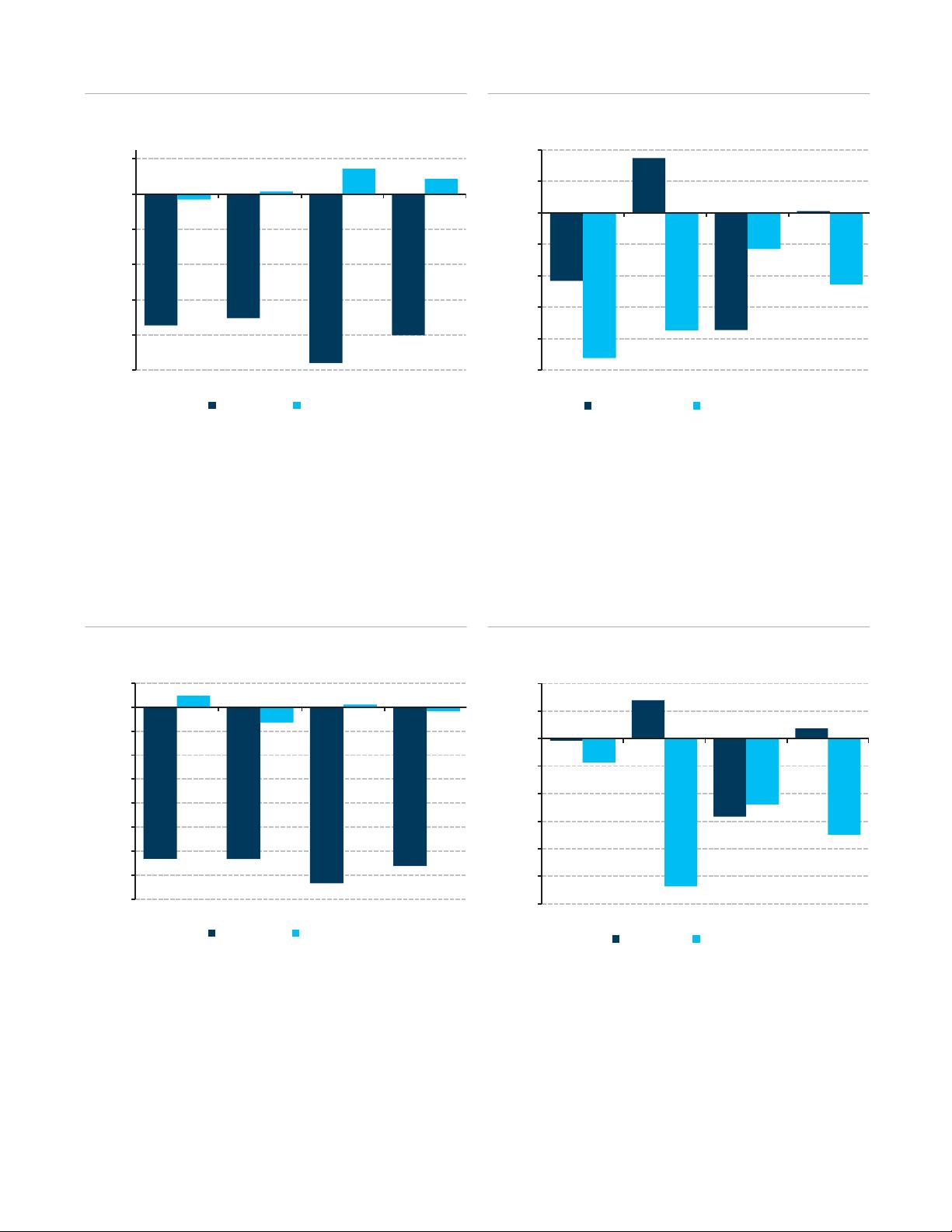

Lower asset manager December Quarter EPS 6-20% from prior forecast. We trace

active management underperformance almost across the board as equity and fixed

income returns were mostly in-line to worse than broad indices (Figure 7). This

underperformance, combined with (likely) outflows drag on AUM & have a negative

fundamental read through to earnings (yielding 1%-10% downward EPS revisions)

while 2

nd

order impacts like weak incentive revenue & fair value marks add additional

weakness (driving additional 3%-18% downward EPS revisions).

AUM/EPS Weakness—qualitatively understood but potential for downside surprise:

In a perfectly efficient market, the impact of a market pullback on AUM/EPS would be

fully reflected in the stock, but we see potential downside risk. The magnitude of the

December AUM decreases (2%-6% below November, Figure 3) could surprise those

that haven’t sharpened pencils as the big market drawdown & sizeable outflows

happened in the latter half of the month when many were already on holiday break.

Additionally, most Street models take a simple average of period-end AUMs to drive

revenue, which would overstate 4Q Avg. AUM & revenues as the sell-off began almost

immediately in October & stayed low thereafter. On balance, fundamentals (weak

flows/performance, etc) drove 1%-10% downward EPS revisions (vs. 6-20% in total).

2

nd

order EPS impacts—hard to model, non-obvious, & possibly large drag on EPS:

Negative marks on Asset Manger seed books and weak incentive fee revenue (in a

typically seasonally strong 4Q) are not top-of-mind modeling adjustments for the sell-

or buy-side, but could have a material impact on the EPS print. Though terribly difficult

to model, our best effort translated to 3%-18% downward earnings revisions for the

quarter vs. our prior forecast (which in addition to the 1%-10% negative fundamental

revision, yielded the total 6%-20% total decrease in December quarter forecasts). Our

line item forecasts are likely off but directionally correct as actual marks/incentive

comp should come in well below prior levels (& seemingly most Street models). We

estimate each $20mm change in performance/incentive revenue (at a ~50% pass

through to incentive comp) and every $10mm change in fair value marks (no opex

offset) translates to a 1%-11% change in EPS for the quarter (see Figure 2 for details).

AM stocks sold off, but don’t fully contemplate fundamental & 2

nd

order weakness:

Although most asset manager stocks drastically sold since November (down 7-15%, vs.

S&P down ~7%), we believe reported December-end AUM levels may be lower than

most anticipate, yielding possible weakness on the monthly AUM prints over the next

week and into earnings (as some may mis-calculate average AUM). Additionally, while

some may view fair value marks on the seed book & weak performance/incentive

revenue as noise, headline misses would certainly not help improve sentiment on a

pretty disliked subsector and could yield additional downside absent a robust rally in

the broad market ahead of Jan/Feb earnings calls.

INDUSTRY UPDATE

U.S. Brokers, Asset Managers & Exchanges

NEUTRAL

Unchanged

For a full list of our ratings, price target and

earnings changes in this report, please see

table on page 2.

U.S. Brokers, Asset Managers & Exchanges

Jeremy Campbell, CFA

+1 212 526 9750

jeremy.campbell@barclays.com

BCI, US

Francesca Kruk

+1 212 526 3856

francesca.kruk@barclays.com

BCI, US

Jason Weber

+ 1 212 526 9406

jason.weber@barclays.com

BCI, US

Ben Jackson

+1 212 526-3006

Ben.Jackson@barclays.com

BCI, US

剩余21页未读,继续阅读

资源评论