The incremental information content of investor fear gauge for volatility

forecasting in the crude oil futures market

Xu Gong, Boqiang Lin

⁎

School of Management, China Institute for Studies in Energy Policy, Collaborative Innovation Center for Energy Economics and Energy Policy, Xiamen University, Xiamen 361005, China

abstractarticle info

Article history:

Received 15 March 2018

Received in revised form 8 May 2018

Accepted 11 June 2018

Available online 4 July 2018

JEL Classification:

Q41

Q47

G13

G17

C53

C58

This paper aims to investigate whether investor fear gauge (IFG) contains incremental information content for

forecasting the volatility of crude oil futures. For this purpose, we use oil volatility index (OVX) to measure the

IFG. Adding the IFG to existing heter ogeneous autoregressive (HAR) models, we develop many HAR models

with IFG. Subsequently, we employ these HAR models to predict the volatility of crude oil futures. The results

from the parameter estimation and out-of-sample forecasting show that the in-sample and out-of-sample per-

formances of HAR models with IFG are significantly better than their corresponding HAR models without IFG.

The results are robust in different ways. Thus, the HAR models with IFG are more bene ficial to the decision

making of all participants (including financial traders, manufacturers and policymakers) in the crude oil futures

market. More importantly, the results suggest that the investor fear gauge has a significant positive effect on

volatility forecasting, and can help improve the performances of almost all the existing HAR models.

© 2018 Elsevier B.V. All rights reserved.

Keywords:

Volatility forecasting

Investor fear gauge

Crude oil futures

HAR models

Realized volatility

1. Introduction

The volatility of financial assets is closely related to portfolio optimi-

zation, risk management, and option pricing (see, e.g., Andersen et al.

2017; Billio et al., 2017; Dai and Wen 2018; Moreira and Muir 2017).

In the crude oil futures market, volatility plays a vital role in the decision

of all part icipants in the crude oil futures mar ket, including traders,

manufacturers, as well as policymakers. Additionally, the volatility of

crude oil futures has an important impact on the global economy and

financial stability (see, e.g., Charles and Darné 2017; Cheong 2009;

Gong and Lin, 2018a; Lin et al., 20 14; Wang et al. 2016a; Wen et al.

2018). Thus , understanding the volatility of crude oil futures is vital

for oil-related researchers and participants. Among the many issues re-

lated to the volatility of crude oil futures, forecasting volatility is one of

the major issues that have attracted the attentions of oil market-related

researchers and participants.

The existing literature shows that there are ample models based on

low-frequency data modeling used for predicting the volatility of crude

oil futures. These include historical volatility models (Xu and Ouenniche

2012), AR-type models (Xu and Ouenniche 2012), ARFIMA model (Choi

and Hammoudeh 2009), GARCH-type models (Arouri et al. 2012;

Manera et al. 2016), SV-type models (Baum and Zerilli 2016), power

autoregressive models (Sadorsky and McKenzie 2008), among others.

However, it is difficult for the models based on low-frequency data to ac-

curately measure the whole-day volatility information of crude oil futures.

Andersen and Bollerslev (1998) propose a new proxy of volatility

using high-frequency data. The proxy variable is named the realized vol-

atility (RV). Corsi (2009) develop a heterogeneous autoregressive model

of realized volatility (HAR-RV model) on the basis of the heterogeneous

market hypothesis of Müller et al. (1993), and is later extended. On the

basis of the HAR-RV model, some researchers propose many new HAR

models, such as the HAR-RV-J, HAR-CJ (Andersen et al. 2007), LHAR-RV

(Asai et al. 2012), LHAR-RV (Corsi and Renò, 2012), HAR-S-RV-J (Chen

and Ghysels 2011) models. The HAR models are some of the most popular

models for forecasting volatility in the financial markets. Thus, this paper

employs the HAR models to predict the volatility of crude oil futures.

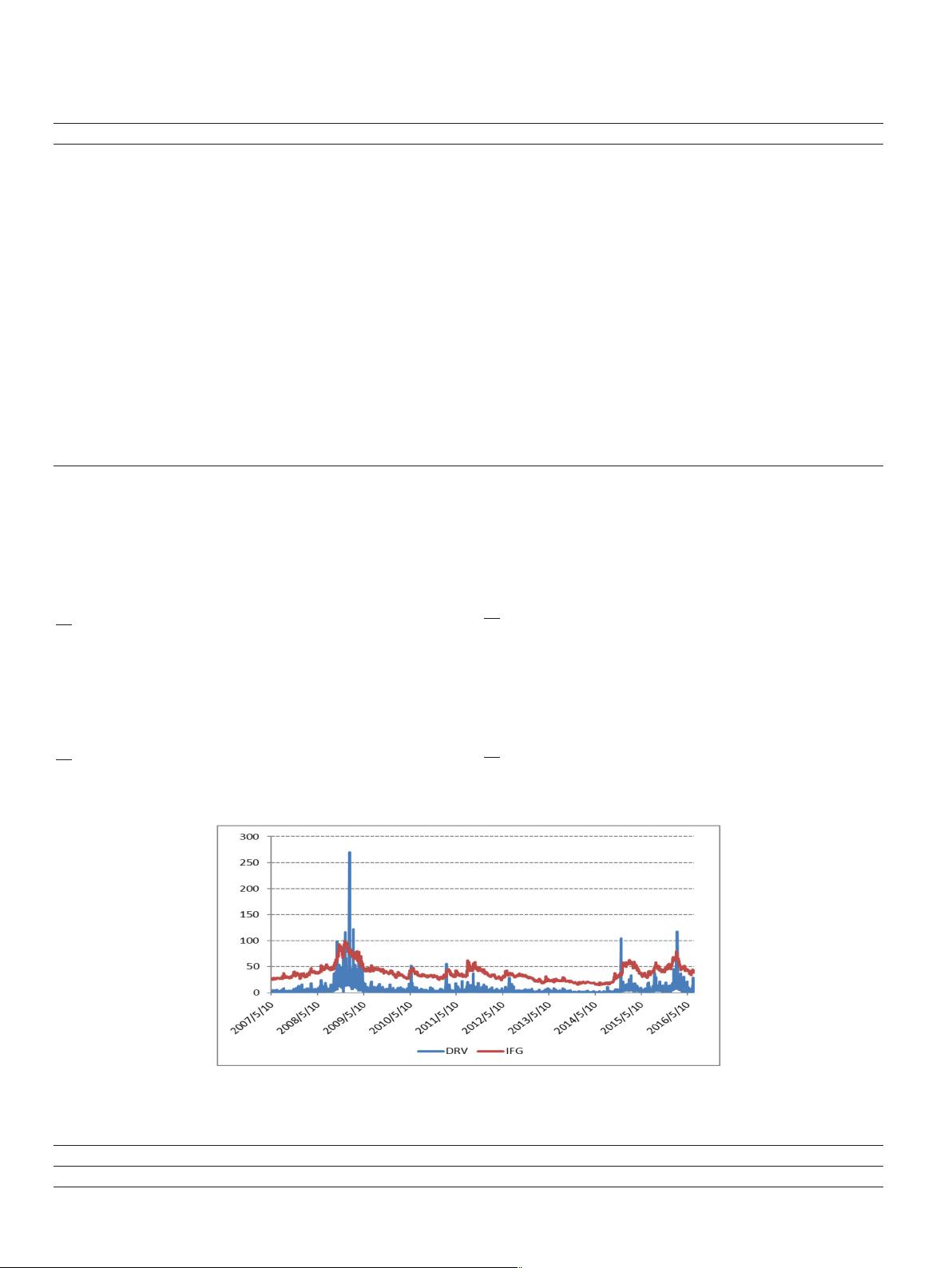

Notably, Chicago Board of Trade (CBOT) proposed the oil volatility

index (OVX) in 2007. The OVX can be used to mea sure the investor

fear gauge (IFG) in the crude oil market (see Ji and Fan 2016; Liu et al.

2017). The IFG (or OVX) is closely related to the crude oil futures mar-

ket. Some studies find that the IFG (or OVX) has an important effect

Energy Economics 74 (2018) 370–386

⁎ Corresponding author.

E-mail address: bqlin@xmu.edu.cn (B. Lin).

https://doi.org/10.1016/j.eneco.2018.06.005

0140-9883/© 2018 Elsevier B.V. All rights reserved.

Contents lists available at ScienceDirect

Energy Economics

journal homepage: www.elsevier.com/locate/eneeco

- 1

- 2

- 3

- 4

- 5

- 6

前往页