1

1 INTRODUCTION

PROC ARIMA can be used with both univariate and multivariate time series and

transfer function models. This user’s guide focuses solely on its use within univariate

time series.

1.1 Nature of the problem

PROC ARIMA uses the Box-Jenkins

1

method for the identification, estimation and

forecasting of time series which are either stationary or which require differentiating

to become stationary. PROC ARIMA cannot be used to evaluate whether the

prerequisite of variance homogeneity has been fulfilled - this is done graphically by

means of the macro %RM. The forecasting ability can be evaluated via the macro

%MAPE. Any preliminary transformations/manipulations must be carried out before

calling PROC ARIMA.

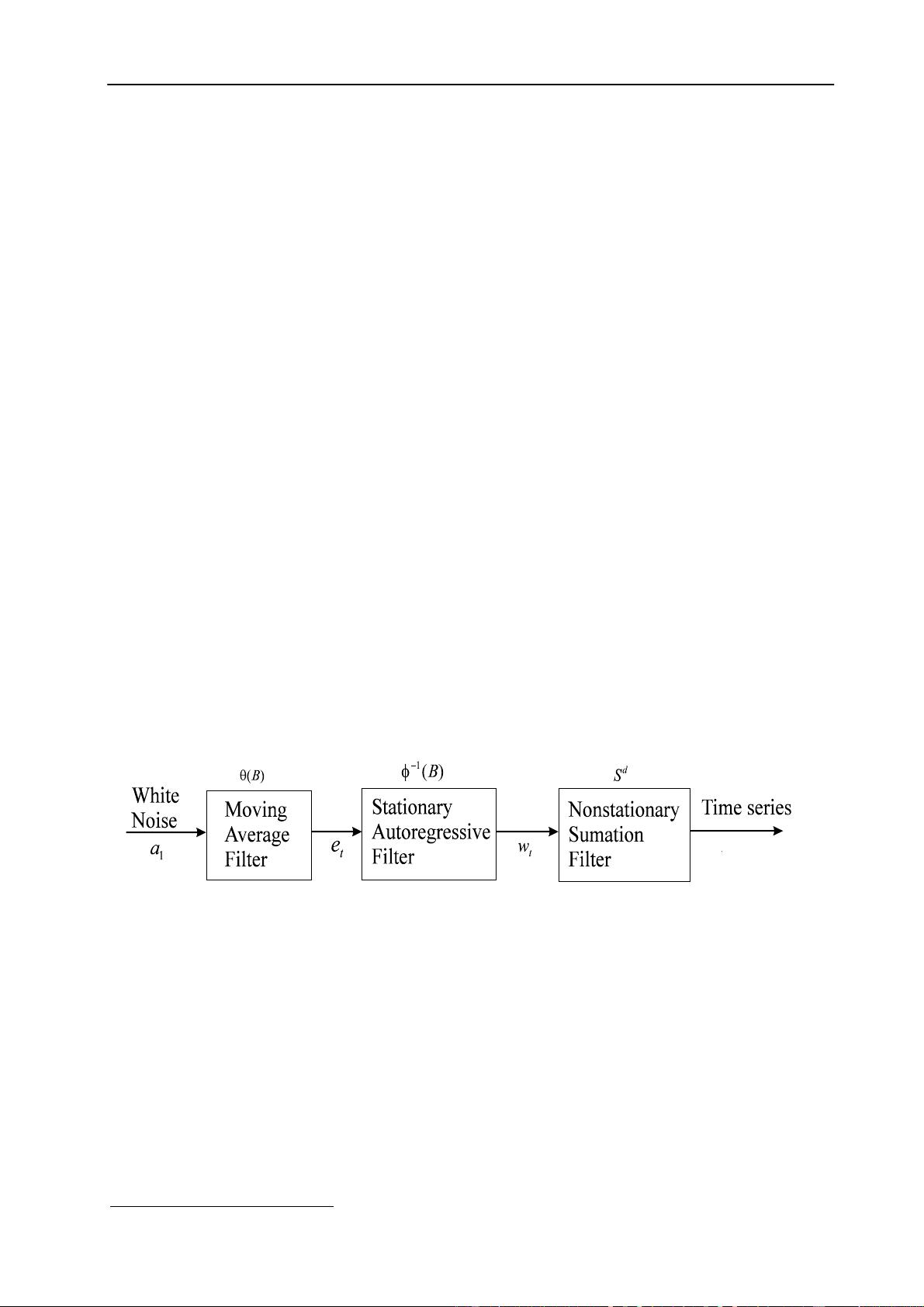

With PROC ARIMA, it is assumed that the process is generated from a sequence of

white noise, together with one or more of the linear filters outlined in fig. 1.

Figure 1 Flow chart for ARIMA models

t

x

Together, the model can be described as ARIMA (p, d, q), or

)( =

w

)(

q

t

p

ΒΦ

where

x

)

-(1=

x

=

w

t

d

t

d

t

Β

∇

plus

Β

ΒΒΦ

p

p1

p

-...--1=)(

φφ

1

and

Β

ΒΘ

q

q1

q

-...--1=(B)

θθ

1

1 Time Series Techniques for Economists.